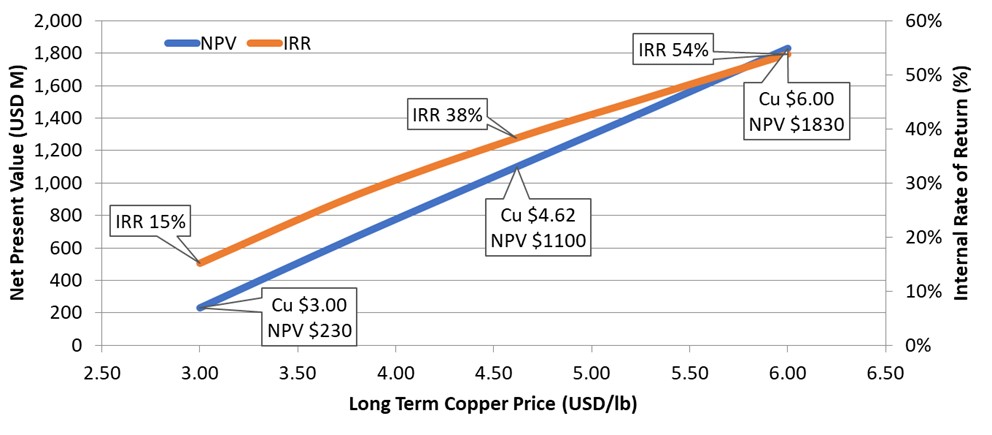

This graphic shows that at about a 33% discount rate, the net present value of their holdings is $1.1billion. At a 38% discount rate the NPV is zero. Not sure what discount rates on mining investments are these days but in an otherwise zero interest rate environment it seems a bit high. As the discount rate drops the NPV increases.

Based on the $14 million they received for 10% of the project, that would place the overall value of the project at $140 million. Thats 12.7% of the NPV that they show in the graphic.

Hard for me to understand how you accept $14 million for a 10% interest in an asset that has at a minimum $1.1billion ( per their graphic ) value.

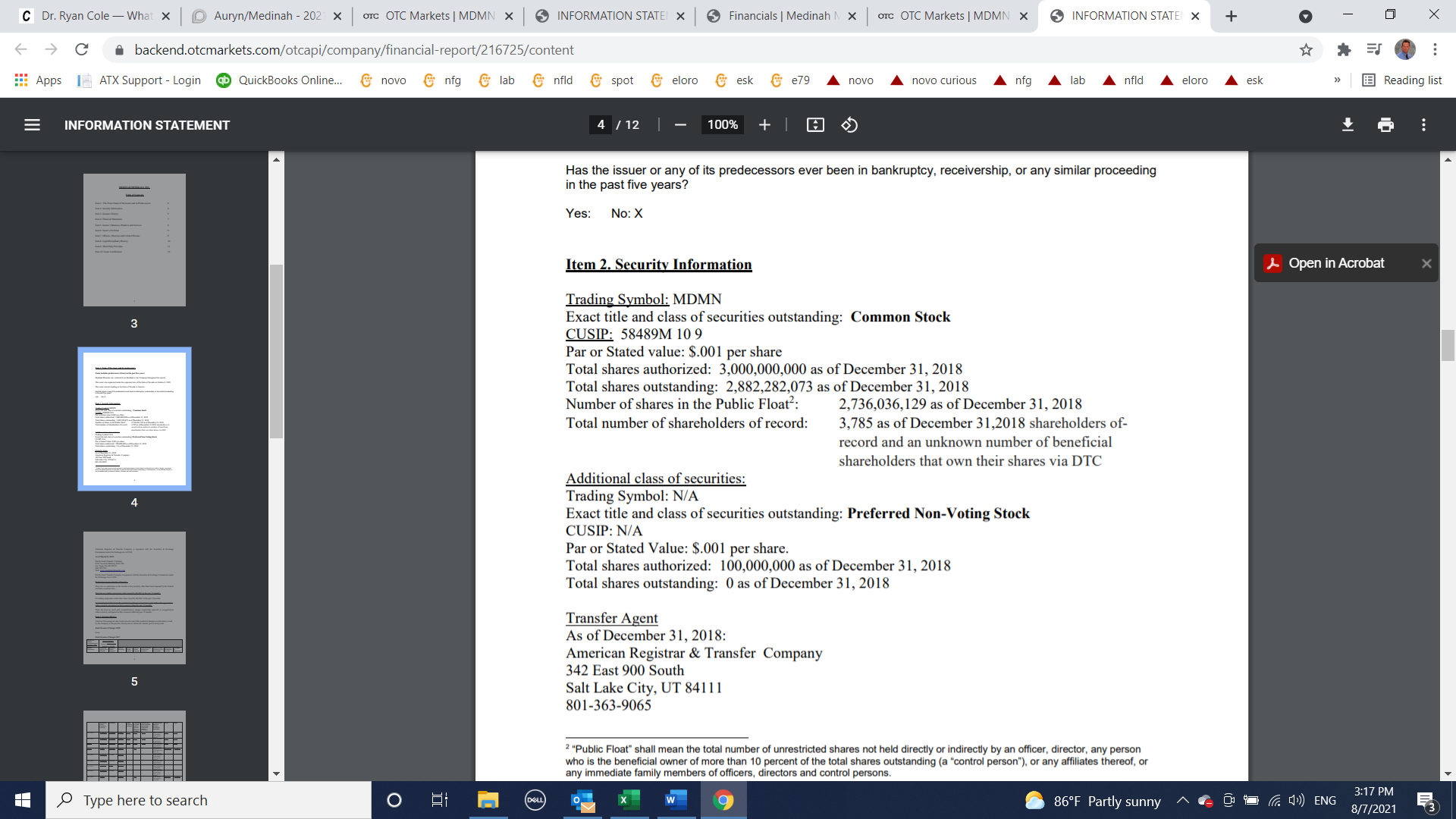

Well, that would be GOOD NEWS if there are only 2.3 Billion shares of MDMN outstanding - sorry, I seem to recall there are about 2.85 Billion shares of MDMN outstanding. I wonder if what you’re reading is “fully diluted”? Look immediately below at the screenshot of the 12/31/2018 OTC Disclosure for MDMN (which is the last such official disclosure I’m seeing for MDMN):

When I get a moment, I’ll look at that company’s porphyry prospects but, in the meantime, I’ll try to get you to change your focus from Medinah/Auryn’s porphyry prospects to their mesothermal vein deposit. Like I’ve been saying, mining is a race to become cash flow positive in as nondilutive of a fashion as possible. The ultimate scenario would be to go straight into high-grade gold production without inducing the dilution associated with having to pay for things like drill programs and feasibility studies. Any major that wants to take you out is going to want to see the results of drill programs and feasibility studies. But if you have a very high-grade mesothermal deposit with wide veins you don’t need to court the attention of majors. You want to get a bunch of cash in the bank before you ever have to sit across the table from a major whose goal is to screw the shareholders of the junior explorer/developer and look after the financial needs of their own shareholders. Medinah and Auryn don’t have to play that game because of the availability of very high-grade early production opportunities.

The Pegaso Nero and the porphyries aspect of the ADL will no doubt be playing the typical mining game with a major or more likely a consortium of majors. That’s fine. We need to concentrate our energy on the cash flow resultant from the exploiting of those veins. When I was young and stupid (now that I’m old and stupid) I used to think that a junior explorer with an active drill program was “in play”. Everybody’s sitting at their computer waiting for drill results to come out. If hole #16 hit 18 meters of 5.2 gpt gold that might get the stock to move. The reality is that this company (not necessarily HotChili but in general) will still probably never see production and if they did get lucky production might be many years out.

Contrast this with Medinah/Auryn. They successfully landed the Fortuna Centro/Don Luis 1 Vein. From 1940 to 1970 it produced from 64 to 92 gpt gold back when gold was at $35 per ounce. The recent sampling of the Don Luis 1 Vein came in at 85 gpt gold. The Caren Vein has similar numbers. They’re both part of a mesothermal vein system famous for the veins getting wider and richer with depth. On June 23rd management successfully intersected the Don Luis 1 Vein at the 150-meter depth level below the plateau. Those production grades just cited were from back up by the surface. Management planned on producing at a clip of 40-tpd starting about 6 months ago but couldn’t hit that pace until finally intersecting the Don Luis 1 Vein at the 150-meter depth level. As of today, Aug. 7, they hit the target about 44 days ago.

On their way to the target, they hit two previously undiscovered veins. We have no grades or widths yet. After hitting the DL 1, the next target became the Merlin 3 Vein which is in close proximity to the DL 1 Vein. It is one of the “2 massive veins” that management is targeting after the DL 1 intersection. The next “massive vein” is the Leopoldo Antonino Vein which either has been intersected by now or hasn’t quite yet. It was about 60-meters west of the DL 1 intersection. About 6 months ago, management had stockpiled 54-tonnes of 85 gpt gold ore from the upper portions of the DL-1 Vein (not from the 150-meter depth level). We do not have a figure yet on how much they stockpiled since then. We can assume that in July, after finally intersecting the DL 1 Vein at depth, they’re probably stockpiling 40 tpd times perhaps 22 working days per month or 880 tonnes for July. We don’t have the previous months production rates but we do know that it was less than 40 tpd.

That 40-tpd “INITIAL PRODUCTION RATE” target refers to 1 blast cycle at 1 working face. Within the next “X” amount of time, there could be as many as perhaps 6 working faces if all is going well. This was the plan back when the attention was on the Caren Mine/Merlin 1 Vein. If the mining industry is all about being a race to positive cash flow in as nondilutive fashion as possible, (Medinah obviously got off to a terrible start but somehow still ended up with 24% of the action at the ADL) then which company is truly “in Play”? Is it a junior explorer drilling hole #17 in a Phase 1 drill program or is it Medinah/Auryn and its shareholders waiting at the edge of their seats to hear the grades and widths of the newly intersected mesothermal veins which will open up 2 new working faces doing 40-tpd INITIALLY? The questions that arise are: how wide and what grades did the DL 1 show at the 150-meter depth? How wide and what kind of grades did those 2 new vein intersections made on the way to the DL 1 back in mid-June? How wide and what were the grades found at the Merlin 3 at the 150-meter depth level if they successfully intersected it? How wide and what grades did they find at the Leopoldo Antonino Vein if they did successfully intersect it? Remember that the Merlin 3 and the LA Veins were over 2-meters wide AT SURFACE.

Management will do a nice deal at the porphyry locations when you least expect it but for now we’ve got enough on our plate with the mesos. Thanks for all of your posts JimmyP!

Now, I’m off to “Dollar Tree” with the grandkids. Do you remember that TV show where the contestants ran around the grocery store throwing stuff into their shopping carts and the winner would be the one who could run up the biggest bill? Yep, that’s us!

Yep, this is the coup de grace of this operation. If our guys can monetize these 5 veins at two faces each and at 40 tpd each even at the lower grades from surface, we will all do VERY well. If the grades have grown at 150 meters of depth, then … Good Heavens. If this comes to fruition, the only way we should even CONSIDER dealing with majors is if they can proceed without interrupting our mesothermal production (no cut on that action) and if they come to the table with money to give US (with NO dillution).

Glencore is not just paying $14M to sit back and own 10% as would be the case in a royalty arrangement, which is strictly a financing arrangement. If that were the case, $14M would be a terrible deal for HCH. It’s a joint venture and clearly HCH needs Glencore to unlock the 90% remaining value that HCH retains. As in our case, minerals stuck in the ground with no way forward to monetization is basically worthless.

The $14M will be going into the ground to Kickstart production. I admittedly can’t tell you if it’s a great deal or not but for a company like HCH, they clearly needed Glencore. If Glencore’s investment and expertise is what it takes for HCH to start cashflowing their remaining 90% stake, then it sounds like the right move for them.

Going by the $1.1B NPV from that chart, their 90% retained interest should put them at over $900M valuation. Their market cap is currently only ~$100M. I’m sure as developments progress, they will grow into a market cap closer to $1B now that Glencore can take them there. And that chart I believe represents just one of their project. It’s one we should keep an eye on.

Thanks for response Jimmyp. Yes, they are getting hammered with dilution. 2019 and 2020 they raised $29million. they had to issue nearly 1.5 billion shares at about 2 cents per share. They are burning thru about $29million in cash per year so if they have to keep that up they will be issuing billions of shares annually.

Very difficult situation to be in. Hopefully they will be able to start generating some cash flow to stem the bleeding.

Sad that their PFS shows so much future potential yet the share price is unable to reflect it.

We are incredibly fortunate to have the potential to generate cash flow without having to dilute us into oblivion. So far!

Taken from my earlier post

** The impact of shifting politics on the mining investment landscape in the Andean region**,

***** the royalty proposal, which originated in the lower house of congress, is of suspect constitutionality, given that the (current) Chilean constitution assigns taxing powers to the executive branch. Moreover, far from hurtling through the legislative branch, the bill is currently the subject of much careful and reasoned scrutiny in a senate committee. The committee has been taking advice on it from international metals and mining industry experts, who have left little doubt about the damaging effects that the bill would have on mining investment. Therefore, many analysts expect that, while taxes on mining are bound to increase, actual increases are likely to fall far short of the nearly expropriatory regime proposed in the lower house.

Companies wishing to proceed with investments will need to give greater attention to their exposure to social and environmental risks, and to their cost structures, and will need to draft financing, joint venture and other agreements in a manner that will enable them to respond flexibly to possible legal changes. Mining investors already present in the country must carefully examine the benefits of any existing tax stabilization agreements that they may have signed, while foreign investors generally can look to the protection available under international investment treaties. Canada’s Free Trade Agreement with Chile provides investors with some protection.

-------This is good reason for Maurizo’s to continue the small mining operation

he is on, till this all shakes out. He gets some sampling in while he mines ore. Which will get some money flowing when that ore is shipped off to processing plant, The mining team gets valuable experience as they work the mine. He stays on good terms with the Chilean students from the mining university he welcomed on the site to explore and learn from.

[This is great P.R. by the way]

He /they can do all of this, while playing the waiting game with the majors.

And stay out of the political arena gun site, at the same time.

**The Political landscapes in the South Americas is, “not to be taken lightly”.

They can change quickly, and in opposite directions, fast.

These are young countries, coming of age in this new world.

They very much want a slice of the pie.

When it comes to new mining sites in Chile.

One might want to go to Hochchilds corporate site and look at its, one, and only, area of operation in Chile. The Volcan Gold Project.

Very far from the eyes of anyone who might be interested in mining.

Not like MDMN within eye sight of the capital Santiago.

I’m ecstatic about the near-term gold production that is commencing! I agree that it’s the quickest way to share price appreciation.

We can look at Hot Chili as confirmation that even a JV with a major has not gotten their market cap anywhere close to the estimated npv of the resources. Supposedly their copper deposit will be one of the largest in the world.

It’s a slow game and we are all tired. Posting some big profit figures is just what the doctor ordered. No pun intended.

For those of you that hold MDMN shares in TD Ameritrade account tomorrow 8/13 will be your last day to purchase shares. You will still be able to sell but TD will not take in anymore buys.

No…it will be 8/13 till when the OTC finally posts Medinah’s updated financials. Hopefully, this will turn out to be a very short period of time. I believe the OTC has already have had them for quite awhile but OTC remains backlogged in processing all the various companies(hundreds?) who are attempting to catch up on their filings so their quotes aren’t relegated to the grey market. OTC has indicated on their website that they will NOT provide any lists of companies or otherwise respond to inquires on a particular company about whether they have made recent submittals or not to become current.