Now if we can only get those AUMC shares!!

2 Likes

Just as a security backup, I’ve been hanging on to my wedding ring from my first Ex. We paid $40 for it in 1971.

Anyone have the 1999 Howe/Cintis report handy?

5 Likes

Refer to Geological Report on the Fortuna Gold - Cerro Dorado, Inc.

Page Viiii and Page 23.

1 Like

Not a geologist but picture 2 and 3 looks like melted rock going down that face.

Finally’" we have a “tape measure” in the pictures. Something to give us perspective to what we are looking at. And Please turn away your head lamp and get a decent light, or camera to take better pictures with.

Presentation, presentation, presentation.

** Please start crushing and separating, and driving that ore off that mountain before snows come…

6 Likes

On Figure 3 at the below link you can see small veins colored in yellow just east of the Fortuna Centro Vein (Don Luis 1 Vein). At surface, these were about 8 or so meters east of the Fortuna Centro. The yellow coloring signifies that they were less than 0.1 meter wide (4 inches) at surface. In fact, they measured in between 5 and 8 cm at surface or about 2.5 inches in width. In geology, these are called “subparallel veins” which means “almost parallel” (to the DL1 Vein). The “sub-“ prefix doesn’t have anything to do with being “under” anything in a geological context.

Being “mesothermal veins” these veins are expected to increase in grade and width with depth. If these 3 new pictures on twitter are indeed one or two of those veins, then it looks like they have expanded to about 8-times their width at surface (to about 20 inches) at the current level of about 100 meters below surface. But we don’t know with 100% certainty if the various veins intersected at depth in the Antonino Adit, correspond to the veins intersected at surface during the Auryn trenching program. A lot can happen to the orientation of a vein during a 100-meter or so drop in elevation. The density of veins under the surface will exceed that seen at surface.

At surface, the DL1/Fortuna Centro Vein averaged about 15 cm (0.15 meters) in width or about 6 inches. There’s no guarantee that the DL1 Vein will match that 8-fold widening over the course of 100 vertical meters if indeed the recently intersected vein corresponds to one of the narrow veins intersected at surface during the trenching program. However, the 20-inch width of the vein pictured in those 3 new photos is very encouraging. But, of course, we need to wait for the assay results.

This newly pictured vein does not appear to be another one of these “splays/ramifications” coming off of the DL1 Vein. The “splays” have been coming off at oblique angles and are often almost horizontal in orientation across the working face of the adit. This new vein is nice and upright and has a well-defined sericitic “selvage” where it merges with the host granodiorite. The scalding hot hydrothermal fluids ascending into a fault/fissure within a body of granodiorite will “alter” the plagioclase feldspar within the granodiorite into “sericite” which is a type of “mica”. This looks like a stand-alone vein.

These mesothermal veins form way down deep where both the temperatures (about 500-degrees C) and pressures are extremely high. These ultra-hot and highly-pressurized hydrothermal liquids and gases have plenty of “oomph” to widen out pre-existing faults or fissures within a rock structure. Faults start out being wider width depth. By the time these fluids and gases make it up near surface, the temperatures are approaching room temperature and the pressures are approaching 1 atmosphere. There’s no “oomph” left to dilate out the size of a fissure in the rock structure near surface. So, you might be left with a less than impressive 2.5-inch-wide vein at surface. But don’t count out a vein like this as not having any significance down at depth.

A similar phenomenon occurs with the gold grades, most of the gold gets dumped down deeper where these fluids were able to “boil”. By the time these fluids approach the surface, the gold grade is de minimis and all you want with trenching results is just the presence of some gold to indicate that these fluids were “gold-bearing”. Any gold that did make it to surface is usually extremely fine and these tiny particles were light enough to float to the surface. What amazes me is that the artisanal miners at the ADL (“SMFL”) were able to average 64 gpt gold production near surface over the course of 30 years with no visible gold present. That’s an awful lot of tiny little gold specks that made it up close to the surface.

Time will tell if the angle of divergence of these smaller veins as they descend through the earth’s crust matches that of the DL1 Vein. The superior economics of mesothermal vein deposits has to do with a combination of wider widths and higher grades with depth not to mention how deep they tend to descend into the earth’s crust.

In the middle photo of these 3 new photos, you can see how the working face of the adit has been cleaned to show a little more of the character of the rock. This rock has a different appearance than that contained in the various “splays” we’ve been witnessing. The new rock is taking on more of a reddish hue reminiscent of either hematite, an iron oxide, and/or cuprite which is a copper oxide which is 88% pure copper. Both of these are often associated with gold in hydrothermal veins.

The veins at the ADL have a tendency to “pinch and swell”. Maurizio made the analogy at the informational meeting in Las Vegas that they behave like a Rosary with a thin chain and dilated beads. When we study these photos in the Auryn website “gallery” we never know if we’re looking at an example of the chain or the dilated bead. The main form of worthless “gangue” in these veins is quartz and I don’t see a whole lot of quartz in these new photos. The quartz that is present is that of “milk quartz” or “chalcedony”. This is the stuff that gold loves to hang out with.

The presentation of these “veins” (or this singular vein) is different than that of the “splays” we’ve been seeing recently. The vein in photo #2 of these 3 new photos is a nice-looking structure with a very distinct sericitic(?) selvage (border with the host wall rock). The reddish material is likely to be either cuprite, which is a copper oxide that is 88% pure copper, or hematite which is an oxide of iron native to gold veins. Potassium feldspar is another possibility.

I get the distinct impression that Auryn’s management and their professional geoscientists are focused 100% on intersecting the DL1 Vein and, for now anyways, are not interested in these other veins even if they have wonderful grades. The DL1 Vein is more of a known commodity. The grades witnessed at the depth of the old “Fortuna Mine” workings were nothing less than stellar. This is the spot where the artisanal miners ended their exploitation efforts. If, once intersected, the grades and widths of the DL1 Vein are what management anticipates them to be, then they can simply exploit this vein at multiple levels and not even address all of these other veins and splays for a long period of time. I think this is what Kevin is referring to when he cites that management and the miners are “keeping their eye on the prize”. Figure 3 at the below link shows these yellow-colored veins that surround the red Fortuna Centro/DL1 Vein:

8 Likes

The ops games are still being played. The significant event for Mdmn may just be the announcement of the AUMC shares populating into Mdmn accounts for whatever final ratio is determined.

If these mms are truly short the stock, I can’t wait to watch them burn thru a short squeeze.

Mdmn won’t be taken seriously until this happens IMO.

If it doesn’t happen, we’re all screwed

5 Likes

I would agree that the distribution is a more significant event for MDMN shareholders vs. “another” binary event of hitting the DL vein. The stock didn’t move the last time they hit the DL Vein so its hard to argue this time being any different. Its fair to say that they’ve made a bit of progress tunneling since the last binary event and there are lots of pictures documenting the same. However, I don’t understand why the company isn’t moving some of this mined ore to Enami. The associated assays would be helpful as would some incremental revenues to offset the ongoing expenses. Claiming that they are stockpiling the mined ore because they are only focused on the DL vein doesn’t make any credible sense to this layman. Gotta put that brand new truck to work.

5 Likes

BB,

You allude to a map of this area existing sometime in the distant past. Is the map publicly available? If so, has Auryn already past the expected intersection of the location that never got mined, or is the expected trajectory just a little beyond our present progress? If not yet located, how much further before it’s location is definitively deliniated? This would be the very richest area for the quickest return, not just for cash flow, but a block buster PR shareholders have been waiting for. The Q1 should have details on what has been accomplished and future goals. Quarterly reports have been timely filed on time for a few years. I know the “Looking forward to what we uncover next week” was recently teased a little more than a week ago. I would think that if what was expected to be uncovered was truly remarkable it would be routinely highlighted in the March 31 Q1 rather than a fluff PR. The next PR would then follow with very detailed information and assay results. MDMN distribution of AUMC shares will occur after AUMC has attained several quarters of positive cash flow.

EZ

3 Likes

Assays aren’t as readily available as you think. I know AURYN is still waiting on assays from more than 5 months ago. Some have not been delivered at all. Going into production on the high grade will be the “ultimate” assay. The previous example being the 15 g/t over material they’ve passed through.

Once the DL is hit, they will get results on a significant tonnage much faster than assays come back.

7 Likes

Someone mentioned having the joy of watching the shorts getting burned with MDMN.

Proposed Rule 13f-2 and Form SHO would require that institutional money managers file

on the Commission’s EDGAR system, on a monthly basis, certain SHORT SALE related data,

some of which would be aggregated and made public. Certain data, including the identities

of such managers and individual short positions, would remain confidential.

2 Likes

Baldy,

My take on the situation is much different from yours. Your lack of support for the success of this company is more than apparent in your repeated advise of what management needs to do. It is not just “hitting” the DL vein, but putting it into production. Until that happens there is no way for the market to put value on this company. The truth of the situation is that the only thing that will raise trading interest and price is not shares on the open market, but putting the highest grade ore into rapid production as soon as possible. This is the immediate goal of management, and every effort is being made to accomplish this. As WIZ says, going into production on the high grade ore will be the trigger to launch the interest and PPS of AUMC stock in the market. Since the supply is so limited, MDMN will act as a precursor of predictive value for AUMC. Trading interest will increase on MDMN stock not just from present shareholders, but also from speculative traders (and day traders) rapidly launching the active trading of MDMN quickly to a much higher price. Present shareholders should hold on as this occurs for the long awaited conversion to occur. This dynamic will be a direct result of shipments of high-grade ore to Enami and production figures, accompanied by cash flow from the DL vein. Once that is evident, it will make sense to perform the conversion of MDMN shares for free trading AUMC shares in a company that has gone into production.

10 Likes

new doc 2022-02-26 10.23.09 (2).pdf (1.0 MB)

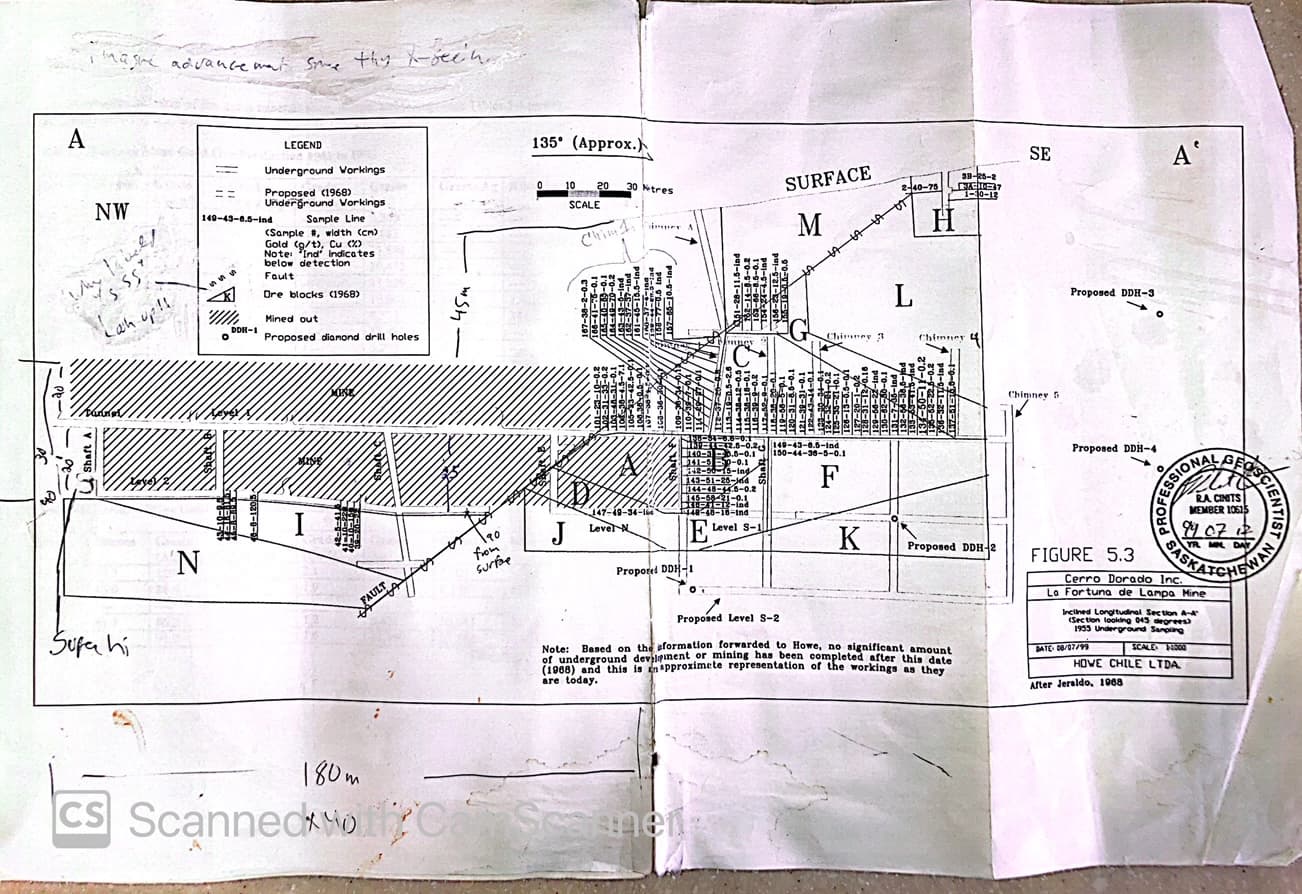

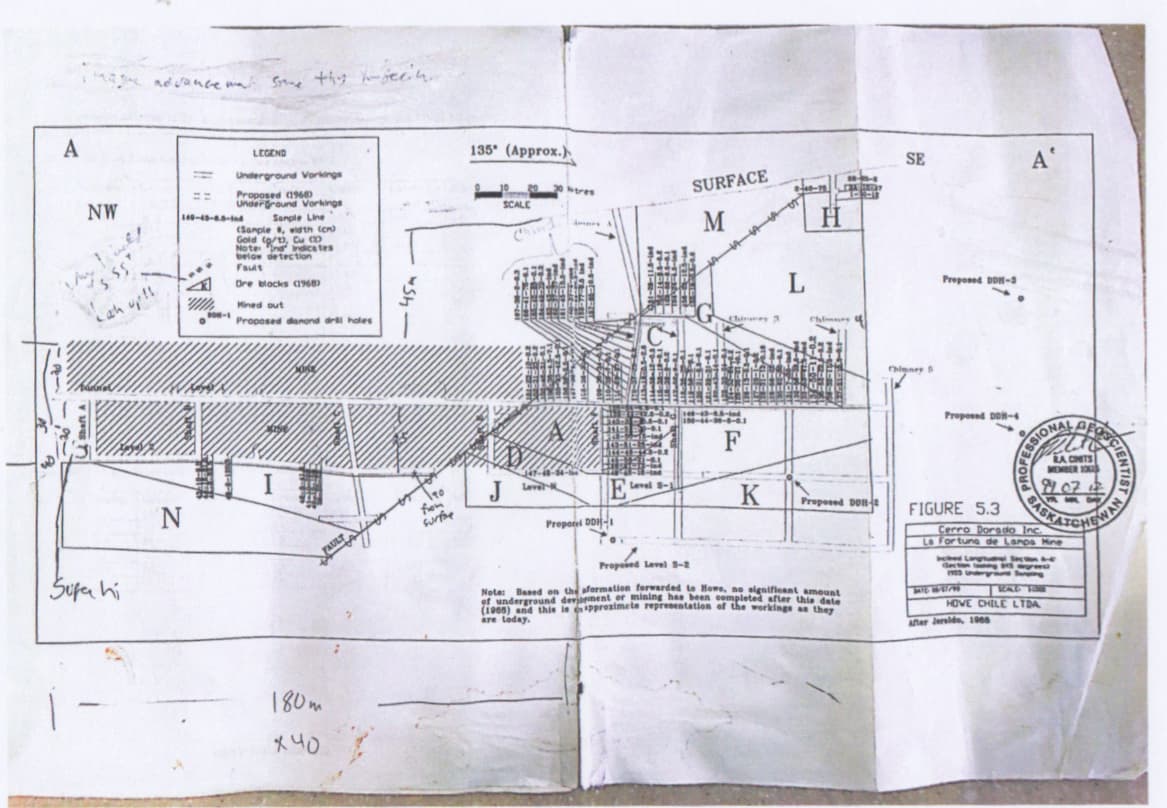

Hi EZ, this is the figure I referenced. It is figure 5.3 on the 1999 Howe Fortuna research paper. I bought the hard copy of this report about 20 years ago. Apparently the internet version did not carry this figure because it was a multi-page “fold out” within the text. For all of these years, I could never figure out why nobody was discussing this information.

I copied Kevin with this figure in case the link I posted didn’t work. I asked him to post it for all.

1 Like

Thanks BB,

It downloaded OK!

I didn’t have a converter program to change pdf to an acceptable format, though.

I re-scanned it and saved as a PNG and this is the result:

Can you go over the details again as explained in the Howe research paper?

TIA

EZ

2 Likes

You are correct. There are massive delays at many assay labs. I’ve heard of up to 3 month delays in some cases. The “assays” from the uber high grade DL material coming from actual payable material will certainly be helpful (for visibility on grade and actual cash flow) but it still doesn’t explain why AUMC isn’t monetizing all the rock we are seeing in the shiny pictures. Why keep a truck idle? Yes, $40k over a six month period won’t move the needle but it doesn’t make sense to not send already mined ore to Enami. Something doesn’t add up.

Assuming, they are truly ignoring 15pgt material b/c they have their sites set on hitting the DL Vein, its important to keep in mind that “vein” mining is extremely difficult. It’s hard to be able to predict where the vein is headed directionally (even for well capitalized mining operations). This is why most mining co’s actually initiate a drilling program, with block models, feasibility studies. and measured resources/reserves. Its also why the market generally awards co’s who take this approach as they are able to model “life of mine”, production estimates based on TPD in different blocks of the model and grades, etc.

There are clearly benefits of trying to establish a mine plan while mining (less dilution, more expeditious) but its equally important to understand 1) the risks and 2) what the market will ascribe value to. As an example: if AUMC hits the DL vein and has stratospheric grade and cash flow for a month or two, this would be a welcome result. However, if they lose the vein (similar to the last 12 months) the market will be unforgiving as unpredictable success is often worse than consistent mediocrity (in the public market’s eye).

This commentary does not come from a negative bias. Even though its convenient to dismiss with that label.

2 Likes

More analysis required, but we may have cut one of the parallel structures of the main vein as referenced in the July 12, 1999 report by Robert Cintis, Howe Chile LImitada.

New tweet from Auryn

1 Like

4 Days ago WIZ asked “Anyone have the 1999 Howe/Clintis report handy?” and showed the Twitter images that this was referring to. Perhaps BB may be able to untangle just how far this parallel vein structure is from the DL for us. The map BB provided from the July 12, 1999 Clintis/Howe report has structures labelled from A → N, but the detail on the rescanned image is unclear. WOW! Just how far is this parallel vein structure from the DL? Apparently Howe and Clintis had it pretty well mapped out and explained in the text of their report. March 31 Q1 should have some answers. Recall from the January 22 shareholder update:

- The mining team has extended the Antonino tunnel approximately 255 meters SSW and is encountering larger extents of mineralized rock and more frequent branches indicating closer proximity to the Don Luis vein.

- Along with the structures mentioned in previous updates, during Q4 2021, the team has encountered the following structures which warrant analysis and consideration for exploitation.

- Nov 9 – a branch of the Don Luis – 1m in width

- Nov 10 – 12 – 2 additional branches of the Don Luis – 15cm and 20cm width

- Nov 17 – 18 – a mineralized fault – 2.5m width

- Nov 22 – 23 – 1 additional branch of the Don Luis – 25cm width

- Nov 27 – 28 – 8 different branches of the Don Luis – each 5-10cm width

- Dec 30 – 31 – 2 additional branches of the Don Luis

- In total, AURYN has tunneled 255 meters into the mountain, beginning at an elevation of 1880 meters above sea level and is currently at an elevation of 1845 meters above sea level. The team has discovered more than 15 ramifications over the 255 meters.

(January 2022 - Shareholder Update | AURYN Mining Corporation)

We are moving closer to the prize and production.

6 Likes

Hi EZ,

EXPLAINING FIGURE 5.3 OF THE ACA HOWE REPORT ON THE FORTUNA MINE DATED 7/12/99

This view is an “inclined longitudinal section” of the Fortuna Mine/DL1 Vein. At surface, the DL1 Vein traces at about 340-degrees. This means that it is oriented from the NNW to the SSE. On a clock with 12:00 representing north, it would trace from about 11:00 to 5:00.

Near surface, the Fortuna/DL1 Vein “dipped” to the NE at about 45-degrees. This figure is “inclined” to account for that. On this figure, it looks like Level 1 is directly above Level 2. In reality it is not. Level 2 is actually below Level 1 but off to the NE a certain amount because of the “45-degree dip”. Distances can be tricky on an “inclined longitudinal section”.

The surface is clearly marked on this figure. The surface elevation is somewhere around 1,950 meters above sea level or “masl”. You can see where “Chimney A” exits at surface. It not only brings in fresh air but also represents an emergency exit for the miners. There is a picture of it on the Auryn website “gallery”. You can see the steel ladder projecting out of the chimney on that photo.

About 45 meters below the surface, you have “Level 0”. It contains 5 other “chimneys/ventilation raises” numbered 1-5. About 20 meters below “Level 0”, you have “Level 1”. The 5 numbered “chimneys/ventilation raises” connect “Level 1” to “Level 0”.

About 20 meters (on an incline) below “Level 1”, you have “Level 2”. Shafts A, B, C, E, F, and G connect “Levels 1 and 2”. I assume that there was once a Shaft D that is no longer operational (cave-in?). Towards the SE you can see notations of “Levels N, S-1 and proposed Level S-2”. You can see several “ore blocks” labeled with large capital letters A thru M. Many are triangular or other forms of polygons. These were highly-recommended targets made by the geoscientists from the bank underwriting the mining efforts of “SMFL” i.e. “CCM” or “Caja Credito Minero” which later became “Enami”. These never got mined and this figure is still pretty much accurate to this day.

The cross-hatching, “///////”, represents areas that have been mined out in between 1940 and 1970. SMFL was working from left to right (NW to SE) starting at the (unlabeled) adit portal to the far left of the page near “Shaft A”. They had to choose some place to commence the adit drifting and they chose this site. In hindsight, they probably would have wished that they commenced the drifting of the adit a little further to the NW and lower in elevation but they chose what they did. Why do I say that? It’s because, Auryn chose to sample the very northwestern end of Level 2 where it met Shaft A and the results were nothing less than stellar and were above the 64 gpt gold grade average achieved by SMFL.

For a sense of reference, the average underground gold mine in operation worldwide mines about 7 gpt gold ore. Basically, you could get rid of the cross-hatching and fill in “64 gpt gold” on this figure in the areas of cross-hatching. I’m going to assume that SMFL might have done some “sorting” at surface but according to ACA Howe the ore had pretty much no “visible gold” present and there were no reports about “concentrating” the ore until SMFL installed 4 crude “flotation circuits” which did bring the head grade up to 92 gpt gold. So, the ore is amenable to “beneficiation” measures like flotation.

The copper contribution near surface (0.2% Cu) was de minimis and was not incorporated into the 64 gpt gold grade. This appears to have changed markedly in areas of “supergene enrichment” as one of the Auryn samples from the Antonino Adit had a copper contribution of 5.3% Cu. One of the key revelations from Auryn’s various metallurgical tests revealed that the ore is indeed “free-milling” and amenable to simple and inexpensive gravity separation techniques incorporating Sepro’s “Falconer system”. This system resulted in recovery rates in the high 90 percentiles. Recall that SMFL’s artisanal techniques were so ineffective that the tailings piles and dumps (the post-processing discards) present to this day are still running over 5.25 gpt gold.

Auryn management has made it clear that they intend to set up their own mill and processing facilities. From an ECONOMICS point of view, what an existing or prospective shareholder wants to get a grasp of is what grade of a “concentrate” above the 64 gpt “head-grade” might Auryn be able to achieve and how much money will it cost to achieve that goal. Don’t forget to include the “by product credits” attributable to the copper contained especially in the areas of supergene enrichment containing bornite, covellite and chalcocite. The formula to calculate the final grade of the concentrate being shipped might be: the 64 gpt head-grade, plus the beneficiation associated with gravity separation techniques, plus the beneficiation associated with flotation (the target here being the sulfides), plus the copper by-product grades plus any head grade enhancement associated with this being a mesothermal vein famous for increasing grades and widths with depth and vertical extensions commonly to 1,000 to 1,500 meters of depth.

The Antonino Adit, which appears to be currently slightly below the level of these older “workings” will (hopefully) be intersecting this DL1 Vein and the old workings coming in at an acute angle. Once the intersection occurs with the DL1 Vein under these “old workings”, management will have to go up probably either 1 or 2 new “Levels” in order to hit the fresh air within “Level 2”. It’s a little bit hit and miss because GPS does not work under the ground and out of the view of the satellite. Even barometric altimeters are “iffy” until there is a direct communication upwards to fresh air.

The math might get confusing because of the 45-degree initial “dip” to the NE of the Fortuna Centro/DL1 Vein, but these “old workings” extend down from the plateau about 70-meters vertically but in a lineal “inclined” fashion they extend for about 100-meters. The lineal extent of SMFL’s prior mining is about 180 meters in a NW to SE direction horizontally at surface. As it turns out, this initial 45-degree “dip” apparently became more vertical and ended up with the vein becoming closer to vertical. This is why it was not intersected much earlier on by the Antonino Adit oriented in a SSW fashion which anticipated the 45-degree “dip” continuing downwards.

MENTALLY TRY TO ENVISION WHAT THE NEXT VERTICAL 35- to 40- METER SECTION BELOW LEVEL 2 IS GOING TO GRADE OUT AT IN A MESOTHERMAL VEIN SYSTEM AFTER AURYN MINES IT

From Level 0 to Level 2 is about 35- to 40- meters whether you’re counting vertically or “down dip”. So, what’s the next 40 or so meters below Level 2 going to grade out at? How much wider might the vein be at this new level versus what it was at Level 2 or at the surface where it was about 0.15 meters wide. Keep in mind that the vein has been traced at surface for about 10-times the lineal extent that SMFL mined i.e. 1.7 Km versus 180-meters.

FOR NOW, CONFUSION MIGHT REIGN

Because of the many, many hundreds of pages of geological reports and the 30 years of past production, the DL1 Vein is a somewhat known commodity. The grades have been stellar for a very long time although the volumes of ore mined under artisanal mining conditions are not that large. Don’t confuse the trek that Auryn has been undertaking during the drifting of the Antonino Adit with what the evidence suggests they’re going to find when they intersect the DL1 vein i.e. Fig. 5.3 of the Howe report. The various veins that the Antonino Adit has intersected during this journey are photographically very impressive but we don’t have the assay results yet. My impressions are that Covid-19 related delays in providing sampling results might induce a “doubting Thomas” reaction once the truth is revealed.

There appear to have been over 20 intersections of various veins and presumed “splays/ramifications” off of the DL1 Vein to date within the Antonino Adit. The “plumbing system” capable of bringing metal-bearing hydrothermal fluids and gases upwards towards the surface, in my opinion, has been nothing short of phenomenal. We’ve witnessed broad expanses of heavily-mineralized rocks and SHINY YELLOW STUFF all over the place (outside of the DL1 Vein proper) but until confirmation arrives via assays management is right in staying focused on keeping their “eyes on the prize” i.e. the high grades and the fresh air that the DL1 Vein has historically represented.

KEY QUESTIONS THAT ARISE

- We see plenty of evidence of supergene enrichment in the photos taken within the Antonino Adit. The bluish-colored “bornite” (63% pure copper) seems to be everywhere. How vertically wide might this SGE zone be? The average is somewhere around 200 to 300 meters.

- We also see plenty of evidence of “boiling zone” activity wherein gold grades tend to greatly enhanced. The presence of “milky quartz/chalcedony” is nearly ubiquitous. How wide might this “boiling zone” be? The range is from 50 to 800 meters in vertical width with an average of about 300-meters.

- We’ve seen plenty of evidence of “potassic alteration” present especially with the presence of salmon-colored potassium feldspar of “K-Spar”. This is the very high heat form of alteration where high-grade ore tends to concentrate. The presence of high heat “arsenopyrite” related gold corroborates this.

- With outcroppings of veins over 1,000 meters below the plateau level clearly visible, just how deep might this “mesothermal vein system” extend?

- Do those insanely high grades that Auryn sampled at the intersection of Level 2 and Shaft A represent an “ore shoot” that Auryn may have clipped?

DO I OWE AN APOLOGY TO MY FELLOW GEO-GEEKS ON THE MINING PLAY?

I’ve been studying Fig. 5.3 of the Howe report for almost 20 years. I bought the hard copy way back then. I assumed that everybody had access to it via the Internet. I apparently assumed WRONG because since it was a “fold out” it apparently couldn’t be incorporated into an Internet copy or nobody bothered doing it.

When you look at that copy from a due diligence point of view, what’s the first thing you wished you could figure out? For me, it was what might the grades and widths be in the lower left- and right-hand corners of Fig 5.3 where SMFL terminated their exploitation efforts in 1970? A while back, Auryn published the results of 16 channel samples taken from the intersection of Level 2 and Shaft A. The grades were off the chart right at the spot where SMFL ended their exploitation efforts.

On the MiningPlay forum, none of my fellow geo-geeks said a word. I’m doing cartwheels (not very good ones) and not one person mentioned what this might suggest. SMFL quit right at the spot where things started getting crazy. Does it not make sense why management is making a bee line towards that area?

Like I mentioned earlier, mentally erase all of that cross-hatching where the ore has been mined out. Instead write in: 64 gpt head grade + beneficiation from gravity techniques + beneficiation from flotation + grade enhancement from the SGE copper grades + any enhanced grades and widths associated with this being a mesothermal vein + this vein is likely to go down for a long, long way towards the valley floor.

WHAT’S NEXT?

Start penciling out potential economics. Start with 6 working faces, an adit height of 4 meters and a width of 3 meters, 3.1 specific gravity ore (3.1 Tonnes per cubic meter), 2 shifts, 1 blast per shift. As far as the average grade, estimate a pre-beneficiation number and a separate post-beneficiation number. Use the industry multiple of 30.21 times EPS. Figure on 70 million shares O/S. Figure on a 200-to-1 ratio between the PPS of Medinah and AUMC. What do you come up with?

4 Likes