Hey Jimmy, look at that Gold has made a new high 4360. Them dirt piles are looking good $$$$

4 Likes

My bet is that MC is more excited and motivated to monetize those piles than you can imagine.

One step at a time though - IMHO, MC is gonna make us all wealthy ….. and some of you will have to be dragged kicking and screaming the whole way.

4 Likes

Bid and Ask tightening up. Let’s see if this starts to run a little bit with all the positive events going on the mountain. Maybe a Christmas update to go along.

3 Likes

Maybe this picture right here, courtesy of the Wizard, is making people think ……. something is gonna happen?

Ahhh …… probably nothing.

2 Likes

BB, Is anyone doubting that they will have a plant built? That news is already built into this investment. If, for whatever reason, you didn’t see pictures of a plant nearing completion, the stock would be headed to zero. Again, remember, this is a stock that has debt, of all shapes and sizes. Debt can be a great alternative to avoid dilution but it needs to be serviced. This plant needs to be profitable over a relatively short period of time to service that debt. I appreciate that everyone just assumes that this thing will be cranking out cash. Hell, 100gpt stockpiled to the sky, what can go wrong? If mining were that easy…

AMNP has doubled again over the past two days. That’s my exit. Thx for playing.

Traded 72k shares Hi of 20c low of 6.5c. Couldn’t have been much of a position!!

2 Likes

Couldn’t have been much of a position!!

Do you know how many folks on this board remain involved here with positions of less then 25 million shares of MDMN? And, despite unbridled optimism, its pretty clear that nobody owns or has added much AUMC based on the historial volume. I would argue the majority have less than this amount (25M) which would be the equivalent of 70k shares at 20 cents.

To be fair, I didn’t buy nor sell my entire position in a day but I’m also not working with a normal size position. Just a flyer, for fun, and another possible candidate for getting into super small scale production in 2026.CRAZY price action on Friday on, decent, relative volume. AUMC didn’t trade much neither BUT the level 2 (market makers) looked a bit more “active” vs. passive with a very tight bid/ask spread. Haven’t seen that in awhile but it sure looks like someone is accumulating. Just wish it was a bit cheaper from a val standpoint to take another flyer. As most alredy know, bullish price action on large volume (still lacking in this categry) has a tendancy to attract more “eye balls.” Investors are scavengering the PM sector in hopes to find companies that aren’t already up 500%.

I plan to speak to Maurizio next week on an ulrelated matter but will strongly encourge a preliminary mine plan for 2026. Estimates on volume, grade and ounces of production. IMHO, based on today’s market cap, AUMC is discounting ~7-10k ounces in 2026. This would be a stretch and I would think its closer to 5k ounces. If the stockpile made of gold is truly at 60gpt and truly at 60k tonnes, there’s some good upside to the share price. I’ve been pretty clear in questioning the grade and quantum as something more analagous to “old school MDMN” predictions but hope I’m wrong.

An updated mine plan would really help new investors in any attempts of due diligence. Of equal importance, there needs to be better visibility on the terms of the debt financing. Any mine plan will be heavily discounted due to a lack of resources/feasability studies, etc. BUT Maurizio can be clear in presenting guidance in the proper context. If he can improve (massively) the transparency with some basic steps of disclosure on key items, AUMC become investable, and those scavenger hunting investors just might pause to take a closer look.

Based on the last set of pics and assuming the company receives all of its pending permits, production could happen as early as Feb vs. March. Good stuff.

1 Like

If medianh was trading today its shares would be trading higher than AMNP even with more shares outstanding.

1 Like

Your evolution has been remarkable - you went from:

No rag-tag outfit is ever going to produce AND It’s not fair, they cannot produce without drilling 1,000 holes

to

Based on the last set of pics and assuming the company receives all of its pending permits, production could happen as early as Feb vs. March. Good stuff.

And yet, you recently stated they will NEVER pay a dividend.

I’m not worried, you’ll evolve on that too.

Have a nice day.

4 Likes

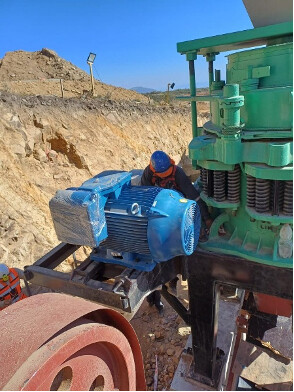

NEW PICTURES

December 13, 2025 pictures, captioned as follows (pictures below captions):

Dec 13, 2025 - Floatation Serrano cell structures completed (welding), Chute support fixings completed above fine ore bin, Cone crusher legs completed, Conveyor belt supports 1 & 2 completed.

Dec 16, 2025 - Began support foundations for electrical cable and services, confirm level/grade of the water tank reservoir area, 4 scrapers and 4 winch systems were delivered for mine activites.

Dec 15, 2025 - Prepare the stock area close to the course ore bin, entry chute cone crusher, foundations bins tailings/concentrate, concrete area electrical generators.

Dec 16, 2025 - Construction of the cone crusher chute to belt #1, belt support assemblies, rotation of the Serrano cell into position.

Dec 16, 2025 - Denver inspection, bracing of the vibrating screen chute.

Dec 17, 2025 - Install motors cone crusher, grizzly, grizzly chute.

Dec 17, 2025 - Begin electrical stands installed (foundations & structures), chutes, orientation of floatation cells, place 20,000 liter water tanks.

Dec 17, 18 2025 - Foundation modifications to ball mill (Comesa alignment issues). To be repoured with Epoxy grout (highly durable, non-porous grout made from epoxy resins and fillers.)

Dec 18, 2025 - Continue chute assembly and welding.

3 Likes

Evolution? Bubbles, it doesn’t suprise me that you are having a difficult time followng along but, to be clear, I never claimed they could never get into production. What I claimed was that they would never be able to finance the construction of the plant by pursuing the “normal” sources of financing, like offtake financing (where I was correct), nor even equity. Yes, if the CEO is willing to sink $10M of his own money and then enter a draconian debt financing, it is indeed possible to build a plant, or a bridge or whatever else money can buy.

My main point has not changed or evolved. Without a resource the road is a very difficult one. Because they didn’t drill “1000 holes” you are sitting in one investment that no longer trades and another that has gone down to sideways (after being diluted 95%) over the past 8 years, under Maurizio, and 20+ years under previous management. The consequences of not drilling are not debatable but rather empirically historical with disastrous results. No evolution needed.

More recently I also told you that the plant would be a year late. Also turned out to be true. However, feel free to do some cartwheels on a Feb vs. March start, just in the wrong year.

Yes, I will also be correct on the dividend front. Where I hope to evolve, is to a point where shares in AUMC become investable. Given the amount of time spent following this “story” I wouldn’t mind actually trying to make money and, unfortunately, it was not possible to short the stock over the past decade so the only option is being long. The history is clear and undeniable but the path forward is all that really matters at this point. I geniuenly hope that the plant is built and the commissioning process goes smoothely so that I and others can analyze actual data and make an educated decision on investability. My main concerns are 1) transparency 2) the rich valuation and 3) the debt obligations where, with any mistep, the equity would get wiped out. If I can get comfortable with all 3 I’d love to make an investment but I’ll never be so naive to expect a dividend.

Hulk. MDMN was trading at $0.0008 before it was “delisted.” Given that shares in AUMC, the only asset (besides AMNP) has gone sideway over this period why do you think shares in MDMN would be trading at 10-20 cents, let alone a penny or half of penny?

The challenge here is that, despite some crazy price targets thrown out around here based on ridiculous metrics (P/E of 30x), shares in AUMC are richly priced based on any sensible “comp” analysis. There is clearly a bias in making those predictions with the hopes of coming up with a price target that gets folks back to breakeven. The difficulty: if you make an assumption that AUMC could trade to $5 per share (just picking an arbitrary price target) the company would be trading at a $350M market cap. Now, if you look at other companies trading at around that valuation, you will find mines producting 50k-100k ounces (vs AUMC trying to get to 5-10k ounces when running at nameplate capacity. These mines will have large, multi-million ounce resources (vs. AUMC with none). They will have feasability studies with analysis on “life of mine” which allows them to trade on a forward multiple (vs. none). Admittedly, I do believe these “comps” are significantly undervalued for now but such is the state of the sector,

Is $5 a share possible? Anything is possible but A LOT of things have to go very right over a lot of years. That would be a signifiant departure from most everything that has happened since new management “took” the assets

Is it Monday yet?

1 Like

Look at the gold, silver and copper miners their SP has increased 5x and more. Why did AMNP go up from .005 to .12? They are not mining, pure speculation and if medinah were trading today like I said it be trading around the same as AMNP on speculation and on AUMC about to go on production.

2 Likes

I see AUMC trading at 5.00 once they start producing that’s my price target. Metal prices are on the move big time.. lets see where the stock is trading in April.

3 Likes

I love the enthusiasm. I guess you need to ask yourself how MDMN would have traded up by 100x when shares in AUMC, its only asset have been flat. But, just for fun, MDMN at 10 cents would be a market cap of $200M (if we use 2B shares outstanding, who knows the actual number). This would mean that AUMC, of which MDMN owns ~20%, would need to be trading at a $1 billion dollar valuation or $14 per share. Funny enough that’s a lot less than BB is calling for so you may be spot on need to up your measly $5 estimate.

The Brecciaboy halo effect is no joke!! You’ve got Mr Bubs taking a “I told you so, a decade ago” victory lap while the primary investment, MDMN, is trips (triple zero), no longer trading and Hulk is predicting the next unicorn company as early as April.

Gold running to new highs this morning 4420. With the year coming to an end 4500 should be reached any day.

1 Like

You know what’s really funny. Some of these shills still defend all this crap!! It’s not that hard to transfer shares WE GOT OUR CDCH/AUMC SHARES IN A FEW MONTHS!!!

stop defending it’s simple give us our shares now before we get screwed again

4 Likes

EasyMoney gave me a link to these TA guys talking about the potential of gold/silver over the next few years - I’ve listened a few times, very good.

1 Like

As a follow up to valuation, I’ve been using AI queries for investment related questions more and more, especially now with hallucinations coming down. Grok is pretty solid, specially for investing/macro. The most value from Ai, beyond a quick and easy deluge of information, is the lack of bias. Anyone who’s invested or traded appreciates the inherent negative or positive emotional bias that is toxic when it comes to making a decision to buy or sell a stock. Grok removes it completely although you have to be careful NOT to ask a biased leaning question as the answer often tilts in that direction. Do I have a negative bias towards AUMC based on my historical experiences? Absolutely!! I don’t think it’s anywhere near as slanted as the positive biases in the other direction but they exist nonetheless.

I asked Grok to provide a valuation framework (Comps) for AUMC using the most basic variables: type of resource, grade, geography, scale. If I had used 50gpt average grade I can only assume the response would be slightly different but I also didn’t highlight the downsides, no resource or feasibility study, etc. FWIW, I received the following;

For a small-scale gold mining company in Chile with a very high-grade (~10 g/t++) narrow-vein resource, initial production targeting ~10,000 oz/year (ramping up over time), and a non-mechanized operation in the short term, valuations in late 2025 remain conservative despite the gold bull market (prices ~US$4,000–4,500+/oz).

These operations are micro-cap, high-risk assets—often single-mine, with challenges around vein continuity, dilution control, labor intensity, permitting in Chile, and limited scalability without future mechanization.

Typical Market Cap Range

US$20–80 million (most cluster US$30–60M).

• Lower end (~US$20–40M) → Pre-production or early ramp-up, higher risks (e.g., grade continuity in nuggety veins, regulatory delays).

• Higher end (~US$50–80M) → Profitable cash-flowing operations, demonstrated reserves (5+ years life), exploration upside, or strong margins from high grades.

Key Valuation Metrics (Late 2025 Trends)

Small producers like this trade at discounts to larger peers due to risks, but high grades (10 g/t is exceptional—far above global averages ~1–3 g/t) can support premiums if execution is strong.

Comparables and Insights

Few exact matches (most small Chilean gold ops are part of larger portfolios like Pan American Silver’s Minera Florida or historical artisanal sites), but global analogs for high-grade narrow-vein small producers (~10–20k oz/year, often underground/selective mining) include:

• TSXV/ASX-listed juniors in similar styles (e.g., high-grade veins in Canada/Mexico/Peru) trading US$30–70M.

• Examples from 2025 data: Micro-producers or near-producers in Latin America often US$40–60M once cash-flowing, with premiums for grades >8–10 g/t.

• In Chile: Juniors like San Lorenzo Gold (exploration-stage, ~C$55M/~US$40M) or historical small ops suggest pre-production vals ~US$20–40M, rising post-startup.

Upside drivers: High grades enable low AISC and fat margins (~US$2,500+/oz profit), plus ramp-up potential could re-rate to higher multiples.

Risks/downside: Narrow veins = grade variability/dilution; non-mechanized = slower ramp-up, safety/labor issues; Chile jurisdiction = stable but bureaucratic (permitting delays common).

I subsequently asked how much would the valuation change if AUMC had a fully built and permitted 100Tpd plant and received the following:

Updated Valuation Range (Late 2025 Context)

With the plant under construction (foundations/warehouse complete, commissioning targeted Q1–Q2 2026 per updates), the fair value range shifts higher: US$50–100 million (from prior US$20–80M estimate, with most peers clustering US$40–70M pre-mill).

• Lower end (US$50–70M): If delays occur (common in Chile permitting/small ops) or grade dilution proves challenging.

• Higher end (US$70–100M+): On successful early 2026 startup, proven recoveries, and initial cash flow—could trigger quick re-rating (seen in Latin American micro-producers).

2 Likes