Welcome to the OTC YIELD sign, as MDMN has failed to meet their 5 day extension for Q1 reports: https://www.otcmarkets.com/stock/MDMN/disclosure

Nothing from Cerro either

CHG

Welcome to the OTC YIELD sign, as MDMN has failed to meet their 5 day extension for Q1 reports: https://www.otcmarkets.com/stock/MDMN/disclosure

Nothing from Cerro either

CHG

Maurizio is quoted in a new Chile Explore Report article here (at the end):

http://cexr.cl/attract-investment

Interestingly the article is about reforming Chile’s laws regulating mining concessions with a view to modernizing the system.

A comment is made re. the opportunity Chile has in relation to Peru and its ongoing political issues, which I was unaware of. Background for this can be gathered here: https://www.opendemocracy.net/democraciaabierta/ver-nika-mendoza/political-crisis-as-opportunity-for-new-peru (I do not vouch for the article’s point of view)

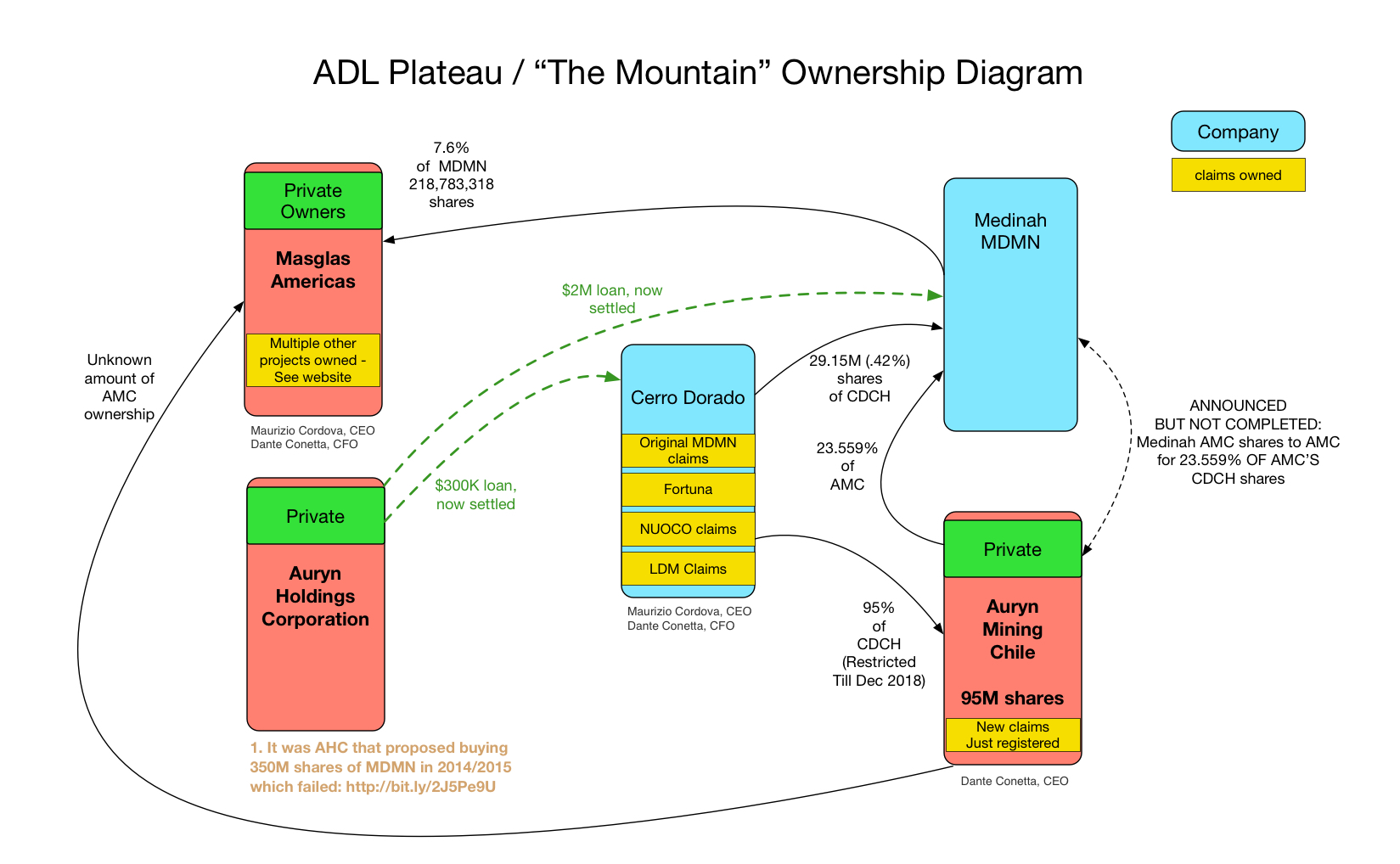

Someone asked about an ownership chart a few days ago. Sitting here watching a baseball game I threw the following together:

Peter I do not believe that Les will ever get the justice he deserves legally or personally. Which is probably what pisses me off the most.

He has to live with himself 24/7. Life will eventually dole out the rest of his punishment. It always does.

Nice! Now if going forward everything was that simple and clear we’d be all set!

NOTE: 12,000 hectares (the area of our claims) = 46.33 square miles

Pretty big when it comes to mining districts?

Is there one that big anywhere else?

Mr. Gold posted a picture sometime back which showed a picture of the Chiquicimanta (the largest copper mine in the world?) superimposed on our little gem - and it put it into perspective.

Now if our guys can … convert? Never mind.

FYI:

The Chuquicamata mine lies on the Chuqui porphyry complex, a north-north east trending, elongated, tabular, intrusive complex that measures 14kmx1.5km.

… The copper ore reserves of the Chuquicamata underground mine are estimated to be 1,700mt grading 0.7% copper and with an average molybdenum content of 502ppm.

Square Kilometers to Square Miles conversion

21km²= 8.108145mi²

Really, not much of a comparison … ![]()

Preliminary Exploration at Pegaso Nero Target Suggests the Discovery of a Copper Molybdenum Porphyry System within the Altos de Lipangue Project.

The previous rock sampling detected highly mineralized Mo-Cu±Au breccia, in this campaign the rock sampling was extended with preliminary results of 1.2% Cu, 860 ppm Mo and 0.12 g/t Au in the hydrothermal breccia.

Preliminary Exploration at Pegaso Nero Target Suggests the Discovery of a Copper Molybdenum Porphyry System within the Altos de Lipangue Project. - AURYN Mining Chile

I used to think like that. But I’ve found people like that have twisted values ergo, goals-- and they live with themselves just fine. In fact they think they’ve actually made accomplishments in obtaining their obtuse goals-. The only hope for justice is: " what goes around comes around"

Bubba,

No, not really. Majors have absolutely huge claim blocks in other parts of Chile especially up North and in the Andes. Their strategy is to simply grab as much perspective ground as possible then look for deposits later with most of the land just barren desert. They like a lot of buffer around their operations as well. However, Cerro’s claim block is quite respectable especially considering almost all of it is likely mineralized(or potentially so) and that it is in the coastal range where widespread private land ownership limits the size of claims. Even better, it is located near good infrastructure.

Bubba;

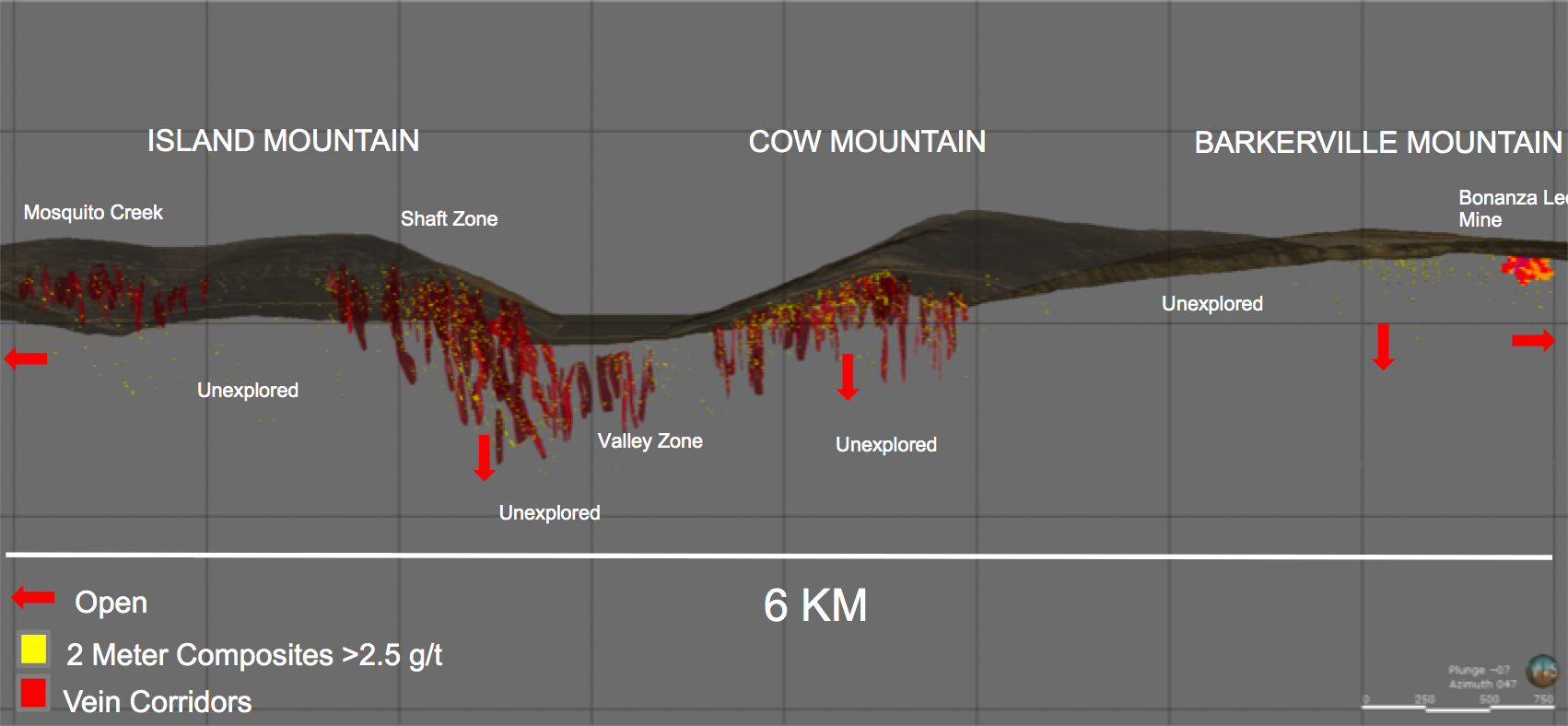

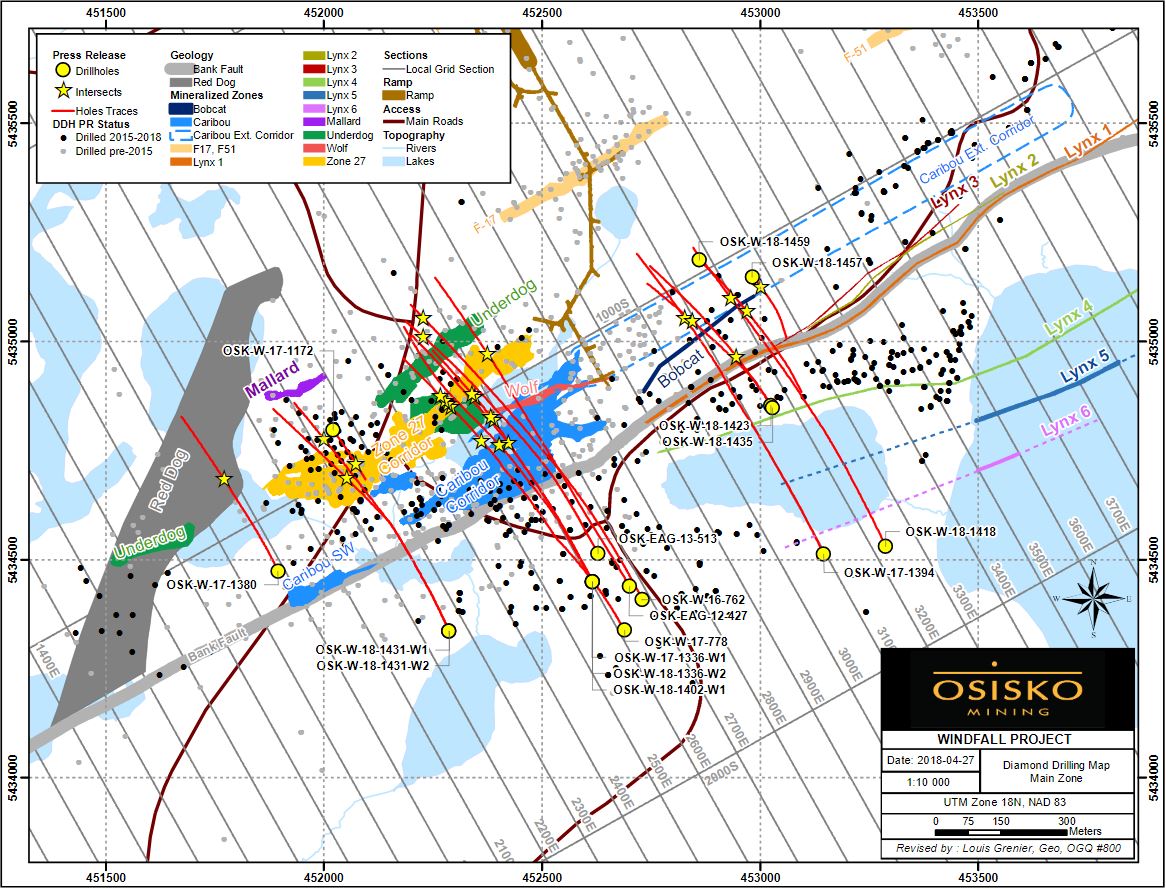

These are two that I know of, both located in Canada. Cariboo in BC & Windfall in Quebec.

Rod

Barkerville Gold Mines BGM.V

Cow and Island Mountain deposits only -

1.60 M oz measured and indicated category (8.1 million tonnes grading 6.1 g/t Au)

2.16 M oz of gold in the inferred category (12.7 million tonnes grading 5.2 g/t Au)

Osisko Mining Inc. OSK.T Osisko has 4 more areas of gold mineralization

So we had some hope the past week and half with a little bit of volume and Mr. Gold digging up those new claims associated to Auryn, excitement was building until Auryn drove another nail in the coffin by not filling financials, wow! We have invested money in this company and all we ask is where are we at presently? ok I said it too many times I’ll tune out…

Death and thereafter may be his ultimate reckoning.

If they knew they were going to miss the 5 day deadline I don’t think they would have filed that extension jmo I say look for them to come out any day. Maybe they are waiting for cerro  the big Bids are still there

the big Bids are still there

1st Quarter Report out for Medinah: https://backend.otcmarkets.com/otcapi/company/financial-report/194207/content

Not much there but noticed that our Auryn Mining investment is suddenly valued at $13.2 million compared to around $1 million last quarter.

also:

Looks like LP finally turned over all his stocks in:

MDMN

CDCH

AMNP

Auryn Mining Chile

As a result (I’m assuming), MDMN’s shares in Auryn went up from 23.559% to 24.848% of AMC

UPDATED: The document still uses the future tense “will own” in regard to the CDCH and AMNP shares and still mentions the Q2 2018 conversion expectation. So perhaps this part of the conversion is still in progress, or it just hasn’t been updated to recently occurring events. At any rate, I assume that’s what the increase in Auryn shares came from so the conversion is proceeding and should be completed by next financials (Aug 15)

[sentence removed by author as misleading … see Wizard below]

My guess is the “will own” is an oversight. Also, it doesn’t increase the percentage significantly because LP’s stock is diluted. He never made the cash call.

Regarding the valuation of AURYN, it now has a real way to determine value, i.e. it owns CDCH.

Can we finally say LP is out of our way and we can finally move forward with the conversion?

So now that MDMN’s ownership % of Auryn is set, it seems like, subject to a couple of caveats, the way is cleared for Medinah’s Auryn shares (24.848% of Auryn) to be converted to the same % of Auryn’s CDCH shares.

There has been speculation as to whether this could occur before the CDCH shares became free trading (Dec 2018), or if it did, whether MDMN could/would distribute them to individual shareholders in exchange for MDMN shares before they become free trading.

And I don’t know.

But I did run across a somewhat similar situation which overcame the restricted shares situation. This is the description:

Artemis Resources (ARV.AX) accepted a JV partner Novo Resources (NVO.VN) in 2017. As part of the deal ARV received 4M shares of NVO subject to a 1 year restriction till Aug 2018.

After that, Kirkland Lake (KL), a much bigger company, took an ownership in NVO and recently decided they wanted to increase their ownership and buy those 4M shares of NVO from Artemis right now (instead of waiting). They came to an agreement on price and the deal is expected to close in May. In regard to the restriction, NVO agreed to release ARV from the trade restriction on the shares and KL agreed to be bound to the original restriction till Aug 2018. [1]

So this implies that the restriction, at least as it involves Canadian and Australian companies, can be a matter of negotiation between companies, rather than simply a legal matter between the government and the buyer. And so in our situation it implies, subject to my lack of knowledge of how U.S. laws may differ, that the restriction may be able to be overcome at least for the first stage via agreements between the companies, just as in this case cited. Whether this could be done for the final distribution to individual MDMN share holders or not is unclear.

Hi CHG,

Great find. The 12 month restriction period comes from Rule 144. Since Cerro was not “fully reporting” with the SEC the usually 6 month restriction period goes to 12 months. To a major miner interested in acquiring a good chunk of the action at the ADL Mining District, I’d have to think that the Medinah 25.3% stake (which includes Medinah’s 10% of Cerro’s original 5 percentage points of AMC) would stick out like a sore thumb. A major wouldn’t care about 6 months left of some restriction period.

If some major does a JV on let’s say the Pegaso Nero, if they’re going to move their troops in and set up shop they’re probably going to want exposure to a stake in the entire ADL Mining District and not just the PN to make it worth their while. Medinah’s fourth of the action in EACH of the 5 subdivisions and deposit types present at the ADL (including the PN) might be the obvious route to take. That large of a chunk of the action should command some type of a control premium. Once any share exchange takes place that control premium is gone.

I’m in this for the long term and I can’t wait to see how this mining district is developed but many shareholders are just plain pooped. In search of a win-win scenario, I would suggest some type of hybrid deal in which those Medinah shareholders who want out now can get out and sell their restricted Cerro shares to an interested major but those who want to go a while longer could take their Cerro shares and hang on for a while. I would love to own shares of a Cerro company which had a major miner as perhaps a 15% shareholder and I think Maurizio might feel the same way. This might serve as a launching point for an eventual tender offer by that major.