I think you ALL are on your high horse pretending to think you have any idea what these people are doing behind the curtain. As a result, everybody should simply express his/her opinion and be done with it. I was told some time ago intimately familiar with the situation that some of the principals actually enjoy the entertainment of some of the crack-pot theories advanced by a few of the more vocal and obviously jaded denizens - which is why I no longer bother. So, best thing to do is yes express an opinion, but do feel privileged to hear the opinion of others, especially those who do not have an obvious axe to grind.

Do you think this is realistic? Give me one sound reason AMC would put $18M (or any money) into MDMN’s hands to be deployed unproductively?

AMC can simply walk away from the option today if they choose to. (I am not saying they are going to.) But let’s suppose they did. Where does that leave them and where does that leave MDMN? Given what I know about both companies, their capabilities, their cash positions, and what they have access to over the next 6 - 12 months, I’ll take AMC’s position all day long if that’s the case.

Regardless, it’s not going to happen. JJ was the real reason why no sane deal occurred over the last 15 years. That problem has been removed. It’s left us on life support to be sure (1.3B shares and NO money and a smaller portion of the claims than we had when we started.) Nevertheless, the patient is still breathing and the mountain is big enough to revive us. MDMN and AMC will reach a deal. We’ll go into production, get some cash dividends, prove the porphyry, and cash out. We can stick around as this happens or not. But it will happen regardless.

2 Likes

Never said it is realistic, I just said I would be happy with this. I also stated in my previous revised post that I do not care where the positive cash flow comes from, whether it is first production or exercise of the the purchase option. The key is that MDMN becomes positive cash flow sooner than later in order to first eliminate debt and the need to issue more stock for operating expenses and then to eventually pay a cash dividend. Of course it will all probably happen in steps which will be hopefully laid out soon! JMO

4 Likes

I believe HR said it best and it is worth reading again.

As suggested by several other posters, read the Auryn contract and use that as the lowest common denominator of what’s what. Do not fill in the blanks by rounding up or rounding down. Assume that there is nothing else but the contract governing the future of this investment. However, supplement that with Auryn’s updates. Do no supplement it with Les’ updates. Do not supplement it with message board opinions or rumors (positive or negative).

Casually follow the price of gold and macro-industry developments (i.e. check Kitco.com every morning). I would also read Wizard’s Auryn blog, but understand when he is stating something factual versus opinion. He’s usually pretty good about stating what is specifically his own opinion.

That’s it. That’s all you have to do. Investing in a mining company is not a day-to-day activity. It is a month-to-month or quarter-to-quarter activity. The share price will work itself out once production begins - once production begins according to Auryn’s guidance, not any poster’s or Les’ guidance.

Anything else that you are reading, with the exception of the helpful geological explanations by CHG, mdmnholder, MikeGold & BrecciaBoy, is just speculative nonsense that if you don’t treat as “for entertainment purposes only” you’ll drive yourself crazy wondering what your investment is all about. Trust me, ignore it. I assure you that you’ll feel a lot more comfortable about this investment when you don’t let the noise of this board alter the lowest common denominator.

And one final thing…do not let the share price affect your interpretation of the fundamental developments of ADL…unless you’re looking for an early exit. If that is the case, you’re going to be disappointed.

3 Likes

L&G, what I would like to see and what is IMO feasible are two different things. And here is where I agree with Wiz.

Let’s step in time, pre-AMC, what did we have? Bifurcated ownership of MDMN Chile and a bunch of other claims. Our boys did not anything about mining and there was zero progress made towards monetizing the claims. Every couple of years MDMN would go through this elaborate process of vetting major mining companies, money firms etc., all under strict confidentiality. The results were picking the wrong partners and having fail to deliver one penny. How many years were wasted with Partner A and Ulander? How many shares were issued?

More importantly, how much work was actually done toward monetizing the claims? Zero

What was the future for MDMN? Nothing

Enter AMC, no-upfront money, but real mining people, spending millions on exploring the claims and bringing validity and credibility to the “mountain”. Do we know all the terms on the Nuoco and CDCH deals, nope, but I don’t think AMC is holding back that info, rather our BOD/Trustee. AMC is doing just what they said they would be doing.

The vacuum is on our side in regards to info and the incompetence of our BOD to convert JJ in common shares without a leak-out/limited amount of shares that could be sold in the market.

Bottom line, IMO, there appears to be a future with AMC where there was none with MDMN. Upfront cash or not.

There are really only two options

- Ride the future with AMC and whatever renegotiated deal they strike with our incompetents

- Stick to the contract and play a game of chicken, which IMO, MDMN will lose and on to Partner 4,5,6…

Question, if the share price were at $.07-$.10 would there be this anger? Now ask, who is responsibile for the share price trading where it is today. Not AMC.

10 Likes

BTW I also know the cash situation for all companies involved. The point is Auryn has been lending MDMN cash to avoid issuing stock. It would benefit Auryn to make sure MDMN has sufficient cash on hand to met all operating expenses thus avoiding the need to issue future shares. Does Auryn have 18M readily available? Probably not and if it did it would probably use it elsewhere. I do believe Auryn will have to issued some cash equivalent whether its $2 million or $18 M or somewhere in between, because there is a big benefit for them not to have MDMN issue shares for operating expenses, especially at such depressed prices. JMO

2 Likes

If the share price were hovering in the 7 -10 cent range I would be ecstatic. But that’s just me.

http://theminingplay.com/t/mdmn-2016-03-14-weekly-discussion/1051/171?u=wizard

From 4 days ago

Lets advance this a bit. I’m in a favor of a handoff to AMC as soon as possible too. I have offered my opinion on some acceptable terms that must have a cash component or a short-term royalty or a brecciaboy like strategy implemented.

Are you saying you are ok with nothing to ENSURE immediate pps appreciation? If you are, i strongly disagree. Pressuring them for the $100M would be a wayyyy better idea than any deal absent of IMMEDIATE PPS appreciation.

I’m not defensive, I’m tired of responding to you. You have stated multiple times that AMC is strong arming MDMN or that MDMN BOD are terrible for not leveraging what they have or insisting on this and that. I simply disagree and have stated reasons why including your lack of comps within the sector and lack of understanding of the contract. MDMN is not in a position of strength here. The people with the money are – that’s always the case when the sector is weak. If gold was screaming, the economy was booming, and large porphyry systems requiring Billions in capital were in favor, perhaps things would be different.

6 Likes

First you said:

“You already know my opinion. I think whatever needs to happen for the MDMN claims to be fully consolidated under Masglas / AMC for immediate exploration and to give MDMN access to early cash flow from the Caren / Fortuna is the right deal.”

Then you said:

“Do you think this is realistic? Give me one sound reason AMC would put $18M (or any money) into MDMN’s hands to be deployed unproductively?”

These are very conflicting statements. Weather its for the option or cash flow from early production, why would Auryn give MDMN any cash?

I think very one assumes just because production is starting MDMN will get cash flow. Why would Auryn do that?

A big problem that has been discussed very little on this board is the fact we will own a minority interest in Auryn, not a free carried interest, or a smelter royalty. As a result we will be at the mercy of Auryn in terms of any cash flow being distributed to MDMN. So I ask again, why would Auryn distribute any cash from early production? They are going to want to use that cash for exploration, which I don’t think is a bad thing, but I do not think we should get our hopes up to much for early cash flow. IMHO this is a long term play, MDMN will receive cash when a major wants in and will purchase our interest in Auryn, sit back and relax it’s going to be years not months, IMHO.

1 Like

How is that a conflict? He responded to someones wishes for 18 mil and said why would they do that ( give me one sound reason) just like you said.

I personally think at least some cash should be part of it because we (mdmn) need it to operate and they do need to pay to play at some point!

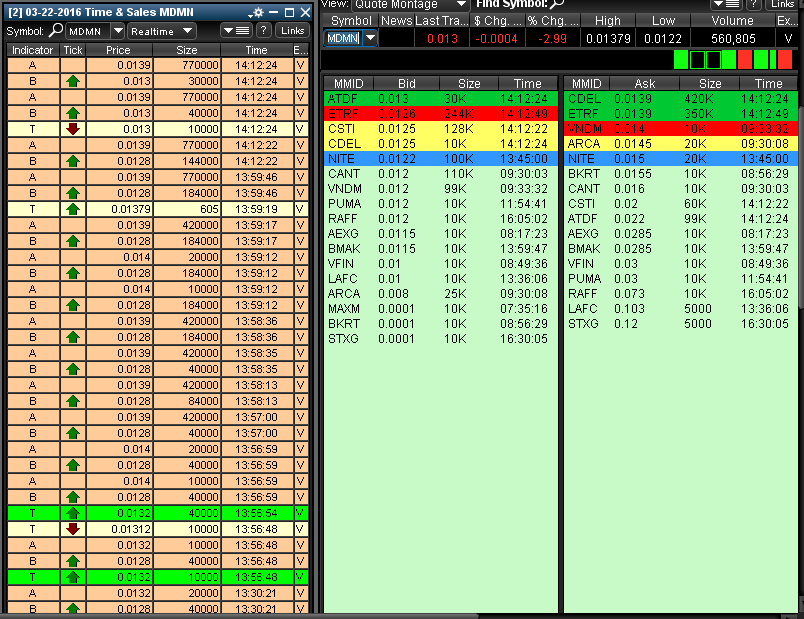

770000 for sale at .0139 April is 2 weeks away from the rumored meetings( not factual) Who wants them??

Same 2 heads CDEL and ETURD on the ASK

I just revisited the latest Medinah shareholder update of Feb 25,2016 as prepared by Mr. Karra. This very recent and positive update concluded in saying that the $100 million and 15% terms of the original contract remains intact. What has changed since then whereby many posters are referring to new payment and ownership contract conditions? I may have missed something more recently as we are currently travelling a bit and not paying as much attention to MP. Again, I am just wondering what has really changed ?

Could Mike, Kevin, CHG or any of our more knowledgeable posters please provide an explanation?

2 Likes

Hi Funnyman,

My gut would be that some obvious “win-wins” have surfaced and both parties wanted to better their overall position at the expense of potential “losers”. If Medinah had its druthers it wouldn’t take a check for $100 million and turn around and hand perhaps $20 million of it to the tax man. AMC with the leverage at hand to put a dollar into exploration and increase the NPV of the deposit by 10 times that amount would just as soon preserve capital while riding that wave of LEVERAGE. AMC doesn’t want to raise money by paying an investment banker a bunch of money to raise the purchase price via an IPO in this current mining environment.

I would think that Medinah would prefer a slug of cash up front or as they need it for working capital and hopefully share repurchases followed by dividends. Those “extra” AMC percentage points are going to grow a whole lot quicker in value than “extra” cash making perhaps 3%. Recall that AMC paid about $15 million or so (a guess) for 210 million Medinah shares. They’ve got an incentive to design “win-wins”. Who are the “losers” in these “win-wins”? The tax man, the investment bankers and perhaps the commercial bankers. AMC’s incentive would be to crank up the NPV of the deposit as high as they can before eventually calling in the heavy artillery when the CAPEX requirements get really steep. This way they can sell less percentage points of the action in order to fund the CAPEX.

1 Like

Little confusing but this is my understanding as of now.

Similar to how it worked for Cerro…the Option agreement would be vacated and replaced at the same time with a new finalized agreement that goes into immediate effect when Les gives his thumb print etc at the Notario in Chile. This will pretty much wrap our investment such that it might be a good time to move on from MP and simply monitor PRs from Auryn going forward since Medinah will start to lose its identify as a distinctly different company with all news/noteworthy events coming out of Auryn.

I see little or no reason for Auryn to put out any news prior to this happening unless they(or Medinah) decide to give a heads-up that they are finalizing a new deal in Chile.

One other thing. There is an obscure rumor that Auryn will be distributing profits from the Caren mine/producton etc each quarter so its partners may receive cash as early as July this year.

5 Likes

Things are progressing very rapidly in terms of how mining projects progress, especially one that is the size encompassing the Alto. Thankfully, we no longer have the historical MDMN BOD steering this project to monetization and success. I’d like to remind those posting here that AURYN will be mining much sooner than later in order to help meet the expense of maintaining the following payroll:

EXPERIENCED TECHNICAL TEAM

•David Bent.- Qualified Person

David has over 40 years of experience exploring for base metals, precious metals and uranium in over a dozen countries. He worked for Noranda Mines for over 27 years and also for Normandy and Newmont prior to becoming a consultant geologist working with Junior exploration companies in Canada and Peru. He has worked on several projects that have been developed into World Class producers such as Real de Angeles (Ag-Zn-Pb) in Mexico and Antamina (porphyry Cu-Zn) in Peru.

•Luciano Matías Bocanegra – Director & Principal Technical Advisor Luciano has over 12 years experience, he is specialized in the porphyry-epithermal environment with additional experience in diamonds, bauxites and alluvial gold exploration. He executed exploration programs in Chile, Argentina, Brazil and Peru, working for Rio Tinto and Hochschild Mining. Last year was working as consultant for private investors and Junior companies.

•Mario Arancibia Nanjarí - Project Geologist

Mario has over 8 years of professional experience in Copper exploration working for major mining companies in Chile and Panama.

•Felipe Andrés Astudillo Rojas - Project Geologist

Felipe has over 6 years of professional experience, mainly working in Porphyry Cu-Mo±Au and IOCG systems in major and medium size companies in northern Chile.

•Enrique Lopez Albujar – Director, Operation & Logistics Manager

He is an electromechanical engineer specialized in HSEC, and over 13 years experience in mining industry working for major mining companies in Peru.

•Italo Volante – Director & Legal Advisor

•Patricia del Carmen Opazo - Mining Claims Advisor

Patricia has over 8 year experience as geomensor engineer in the mining industry and academic teacher. She worked with important mining companies in Chile, in charge of mining claims departments.

•Aquiles Alegría – Consultant Geologist

Aquiles has over 27 years of experience in exploration, evaluation and production of mineral deposits. He has been working for international mining companies in South America, Asia, Europe and Australia. He had managed the local group of exploration in CODELCO North Division in Chile, and Superintendent of Geology for Andina CODELCO Division. As well as Exploration Vice President in Andina minerals and Inversiones Benjamin Holding. Currently advises mining exploration companies in South America and participates as a Board Member of three mining companies.

•Katherine Narea Cavieres - Data Base Geologist

Experience in data base and software’s management. Their main experience is in research Institutes, supporting in applied research, innovation and development projects for Mining and other industries.

The frustration levels don’t need to be reiterated daily on this forum. I’d suggest the “daily posters” take a break until we have the next round of news released. Maybe a little vacation would help! ![]()

Thanks Doc for the very simplistic (babytalk) explanation of these workings about how the contract conditions may be suspected of being changed for various reasons.

On another old topic, do you have any knowledge of Auryn’s recent efforts to obtain more of previous management’s shares or have they just abandoned this exercise? And if so , what will their new strategy be to acquire control of MDMN etc? And if you have already addressed this issue, pls refer me to what day and I will find.

And lastly do you believe Auryn will soon become a public company before the MDMN etc option is exercised? I do not think I want an interest in a private entity.