Will have to wait and see. IMO there needs to be some kind of cleanup of MDMN and a new director, two, or three added.

4 Likes

What I would like to know more about Masglas. Who is on their BOD, assets, debt, cash on hand, etc… Is this to much to ask? maybe they will be thorough on their “Abut Us” like Auryn has done.

Level 2 please.

Auryn seems rather confident that an open pit close to the old Fortuna mine is viable. What do they know we don’t? Do they have anything more than an IP and the narrow Fortuna vein? Is the open pit area really at surface or do they know good grades 25 meters down? Have they drilled it or found another adit?

"AURYN is also preparing the required mining application in order to obtain the required permitting for an open pit at the Fortuna de Lampa historical mine site.

After permitting is obtained, the mine preparation will follow, and production is expected to start during 2017. Actual production from this site has not been taken into account for our preliminary 2017 production estimate. We will update as soon as we have this data available

Fortuna de Lampa is an old mine that was active during the 1960’s. Reports from those days show a total production of 280Tn of concentrate grading 92.3 g/t Au, 133,7 g/t Ag and 0,8 %Cu.

During the fourth quarter of 2015, a mapping, sampling and trenching program was executed with positive results. See the table below containing the best mineralized intervals in trenches…The mineralization at Fortuna target is represented by several parallel veins with NS to NNW trending…Veins are characterized by quartz textures, dominated by crustiform, banded quartz-chalcedoniasulfides and massive types. The widths varies from 0.1 meter to 2 meters, and quartz stockwork several meters halo is very common in the granodiorite host rock. Sericite selvages are very common in the veins-host rock contact.

The hydrothermal alteration is dominated by strong argillic corridor (kaolinite – smectite), and is possible to see extended up to 200 meters width in FH trench sector. This is supported by geophysical response in the CSAMT survey. (See Fortuna targets maps)

Similar to Merlin veins, several veins were discovered after trenching, and the most common evidence are quartz floats and strong argillic alteration corridors. (see Figure 3)

also see:

Table 3: Fortuna mineralized intervals from Trench FD to FG.

Table 4: Fortuna mineralized intervals from Trench FH to FI.

Table 5: Fortuna mineralized intervals from Trench FJ to FON.

Regarding the Pegaso Nero (Copper-Moly area), AURYN is looking forward to reaching an agreement with the surface rights owners in the near future so that we can prepare the area for a campaign of Induced Polarization. This will help us clearly define the drilling targets.

I might have missed some commentary or something in some update, but who are these Pegaso Nero Surface rights owners? I thought Auryn got the whole enchilada by giving us 25%…

Wow, congratulations on the understatement! The Auryn release is further “proof of life” after all these years.

2 Likes

Ulander, was a pump and dump operation by insiders and Ulander?? Anyone else hear about this?

Les always gave us a bit of truth wrapped in lies or as his deceased friend Larry said “wishful thinking”. Tie a bright ribbon of hope around that package and deliver it to shareholders who don’t want to, or can’t give up hope and “BINGO”. It’s a money tree.

Thankfully Auryn has put an end to that predatory behavior.

Congratulations to those who survived and are finally able to see the way a professional, more transparent company can be run.

4 Likes

You’re overstating what I said. The deal was real in the sense that they actually had one. It was presented in the best possible light (truthful in a manner of speaking) but completely bogus and only those of us who were naive, ignorant, gullible, overly trusting, etc… fell for it.

Same with the cherry picked results from LDM that JJ posted about and “trucks” waiting.

It’s all done now. Let’s just move forward. A few more issues to clear up from the old MDMN and it will be a whole new ball game. Those of us who have held took the haircut.

5 Likes

Hi Albireo,

I don’t know the identity of the parties that Masglas is working with on this issue. In order to access and exit the Pegaso Nero in the most efficient manner the operators of the mine need to cut a deal with the owners of the properties needing to be crossed to gain access to the PN and egress from the PN for trucks loaded with ore. The miners have the legal right to gain access to their property so the 2 parties attempt to voluntarily agree on the terms of a “servidumbra de paso” which amounts to a right of way or easement. If they can’t come to an agreement then a tribunal will set the price for the easement.

As I understand it, Medinah went through this process with the tribunal and prevailed with the judge setting a favorable price. Masglas/AMC then did a bunch of geochem sampling and found high grade moly and copper pretty much at surface especially in the areas of the “tourmaline bx” and the “intrusive bx”. Masglas decided to greatly expand the PN project especially towards I believe the south and east perhaps beyond the parameters previously agreed to in the tribunal process.

Recall that the hyperspectral satellite imaging survey done by C.S Perez revealed a 7 Km swath of about a dozen intrusives ALONG THE SOUTHERN DOWNSLOPE OFF OF THE PLATEAU. This is where the PN is. Medinah/AMC must have had some type of easement in effect because they were able to do the geochem sampling program in the area of the two breccias which are on opposing sides of a certain ridge crest just east of the “South Road”. Recall that the “South Road” roadcuts into the side of the mountain revealed a 2 Km-plus long area of mineralized “veinlets” and “stockworks”. This is what porphyries are made of.

The key here for me is the SIZE of the area showing relatively high grade moly and copper right at the surface. The preliminary geochem sampling program was of a decent size but it barely put a dent in the 7 Km swath extent of the surface alteration detected by the satellite survey. Having moly right at surface tells us that the underlying porphyry is shallow. This bodes well for early near surface production opportunities. The melting point of molybdenite is so high that it only likes to hang around near the core of the porphyry. The top of the average porphyry worldwide is 1.5 to 3 Km below the surface. Ours appears to be right there near surface. The other key is the breccias themselves. These suggest a very good “plumbing system” to allow metal bearing hydrothermal fluids to head up towards surface under very explosive conditions. What used to be solid rock has been converted to gravel by this upward thrusting explosive activity. Gravel allows the upward passage of these fluids much better than solid rock.

To me the overall key is that huge SIZE suggests huge MINE LIFE. This in turn suggests A CLEAR PATHWAY TO A VERY, VERY LONG SERIES OF CASH DIVIDENDS. This is the ultimate goal for a Medinah like company. The high grade near surface early production opportunities might allow the commencement of dividend activity to occur sooner than later. I won’t have a good read on when this might start until we get more information on the various TERMS AND CONDITIONS associated with the deal.

5 Likes

Hi hulk,

I can only tell you what my digging has suggested. Masglas represents Peruvian and European capital that like their privacy. There is theoretically an UNLIMITED amount of capital available for the ADL project itself. I now firmly believe in this statement after putting a couple of puzzle pieces together.

A very large amount of prior successful entrepreurial activity is involved in a variety of different industries including real estate development worldwide. Mining is now a focus, especially grabbing cheap assets from majors that need to deleverage their balance sheets from prior excesses back when things were good. The ADL scenario doesn’t fit into this mold but the interest here goes back many years. It clearly appears to be the flagship for their mining activities.

Their modus operandi seems to be heavily concentrated on LEVERAGING their vast assets. They either have to be able to get assets dirt cheap like in the case of their First Quantum/Inmet assets or the project needs to have a lot of internal leverage build into it. It must be nice to put perhaps $10 million into a project and increase its NPV by 10 or 15 times that.

They’re obviously market players or they wouldn’t have bought as much Medinah as they did so early on. I’ve been told that there is plenty of interest by the big boys on our project but Masglas doesn’t need them. For instance, if they are confident that they can punch a hole or two into the porphyry at the PN and come up with long economic intersections then why bring in a major at this time and throw away that leverage? Their actions will no doubt reveal their confidence levels. In his Aurynblog, Kevin mentioned that in spending a couple of hours with MC at the PDAC, MC was approached by head geos from several majors asking how things were going at the ADL. I sense that the majors have been asked to “stand down” until MC should call them.

I don’t have a good read on whether Masglas is up to taking on the porphyritic aspects of this deposit or not. The fact that Alegria is on board suggests yes but I could also see them spinning off the deeper porphyritic aspects to a huge Cu/Mo player and riding the epithermal assets for 20-plus years. We’re into the development stage of this deposit wherein NPV can go up in an almost parabolic fashion with good results. When the NPV starts plateauing out might represent an exit strategy for them. Who knows?

1 Like

Survive is based on your reference, and purchase price to where we finally get to…

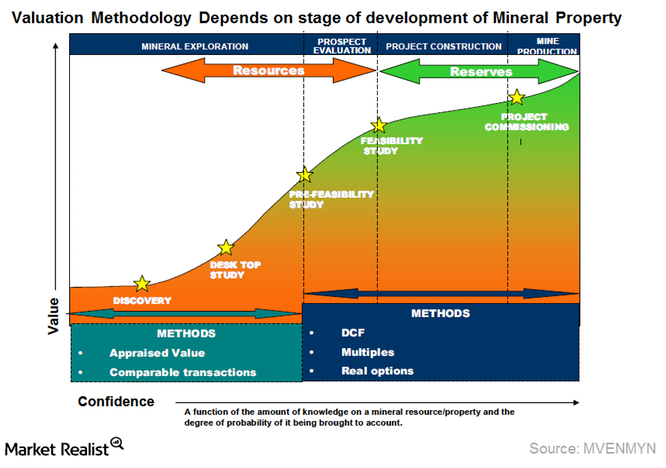

We’re in an overall wait and see mode. I found the following chart and article useful and informative, even though it is almost 2 years old:

I take it we are somewhere between the discovery and desk top study stage of the chart above. We have a ways to go yet, but if the next five years pass twice as fast as the last ten, I’ll be waiting to see where we finally get to … ![]()

3 Likes

I’m more excited about later this year and next year than the never ending “Next Weeks” of the past. Thanks to Auryn/Masglas for bringing some sanity to this investment.

5 Likes