The AUMC “market overhang” looks like it will be de minimis from here on out if good news should appear. The total “float” of AUMC is 3.9 million shares and 3.5 million of that is held by the Cerro shareholders who are way under water. So, a big % of the non-Cerro float just went bye-bye.

Maybe we attracted the attention of a “whale”. Is this her or his opening salvo or did they shoot their entire wad in 10 minutes. Monitor for follow through.

It’s possible that part of the Medinah selling was directed towards AUMC buying but I doubt it. The ratio has been clinging to that 200-to-1 ratio pretty tightly lately. Now all of a sudden it’s 300-to-1. Auryn’s PPS can “pull” Medinah’s PPS up or Medinah’s PPS can “push” AUMC’s PPS up. I’d bet on the former and not the latter but there will be arbitrage opportunities which might provide liquidity anyways.

If the AUMC PPS runs like a rabbit then Medinah will follow because of arbitrageurs like me. On the day of the allocation and distribution of AUMC shares the ratio will be EXACTLY 200-to-1.

I like the idea of the insane tightness of the AUMC share structure spilling over to Medinah in an indirect fashion. All of a sudden 2.8 billion shares is indirectly tight. Hard to figure.

Somebody may have gotten a heads up on the width of the DL1 Vein at the intersection with the Antonino Adit. If that thing comes in at 2-meters width then about two-thirds of the working face will be the good stuff instead of half as presented earlier in those calculations.

I’ve often thought that the place to be in a situation like this is at Enami where they calculate the grade of the ore being shipped. “Hay amigo, look at this”.

Yes, quite strange. I wasn’t watching the trading today. Was it an “arranged” sale and repurchase? Are brokerages allowed to buy from companies in advance of an imminent distribution of shares of a related stock they know they’ll be short on when distribution occurs? Did someone’s estate liquidate? Or maybe something as simple as Medinah getting ready to “go away” after distribution occurs. Here’s the thought I had quite a while ago.

Whatever is transpiring, I’m inclined to think it is laying the groundwork for something good coming to shareholders.

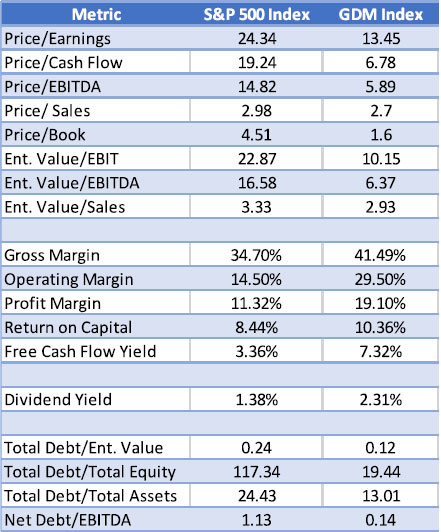

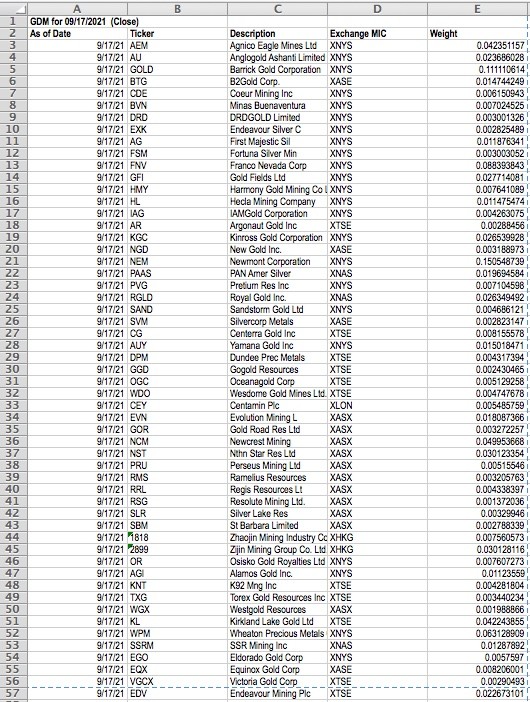

Metrics are important, especially if one is diversifying into the companies listed in the S&P 500 or GDM Index funds, rather than the very risky speculative stocks many here seem interested in. I like and have investments in some of the GDM listed funds: GDM_Index_Composition GDM0319 .pdf (39.0 KB)

However, an old (2016) Motley Fool article has more relevance for what we may be anticipating for AUMC (and MDMN) in the hopefully not to distant future. You may want to follow the highlighted “it’s cah flow per share” link in the article below. Looking forward to a relaxing weekend of pleasant reading and DD.

My favorite metric for gold and silver stocks

It’s cash flow a perfect measurement? Well, no. It doesn’t tell me anything about whether or not a company is profitable, it doesn’t give me any idea of what sort of debt or solvency issues a company might be facing, and it certainly doesn’t tell me anything about future cash flow expectations. These are metrics and findings that I would get by analyzing a full income statement and balance sheet, as well as by listening to commentary from management at least once each quarter. And make no mistake about it, I wouldn’t suggest investors overlook or ignore other important metrics when analyzing gold and silver stocks. But when it comes to the most important metric to me with mining stocks, it’s cash flow per share.

Easy. The point of my providing that table is simply to show what the actual P/E of the “blue chip” gold and silver producers ACTUALLY is today. Even suggesting that AUMC could be trading at a $800M to $1B valuation on 18koz of annualy production (let along 100koz) is so beyond insane that I decided to simply provide a valuation table as any longer response to BB’s “analysis” would require a trip to the Metaverse.

Nice to know Baldy, thanks for the explanation of the relevance that you obviously knew would be of interest. I couldn’t figure that one out for myself! You have excellent research and analytical skills. Also, I forgot the forum doesn’t support the PDF file in my previous post, so here is a snapshot of the stocks in the GDM index you referenced…and yes, I have long positions in all the stocks listed in that highlighted Motley fool article “it’s cash flow per share” link which I hadn’t actually seen before today.

“Metals and Mining”: current P/E 30.21, trailing P/E 44.42, forward P/E 41.86

When the subject is Auryn Mining, why would you post the P/E’s for the biggest miners on the planet like Barrick that also have the lousiest P/E’s? In the P/E multiple the “E” is Earnings Per Share. The P/E multiple is what the market will pay for those earnings per share. A much more accurate ratio is the “PEG” ratio. Here you divide the P/E ratio by the projected growth rate. The “PEG” ratio is much more accurate than an EPS ratio. It gets the young producers a seat at the big boy’s table. The statistics cited in the NYU study is not for just the big boys. It’s for all of the boys that can produce earnings, big and little.

Here is a link that explains it better than I can:

Barrick might have 20 underground mines in operation each working, let’s say, 40 working faces. That’s 800 working faces. Auryn is currently producing from, let’s say, 1 working face. Barrick can’t grow production sites any longer. Once those sites are mined out then their production sites go down in number unless they go out and buy new ones. A new producer like Auryn could conceivably grow their working sites from 1 to, let’s say, 8 very rapidly. They can also “cherry pick” the richest and widest veins. Barrick already did their “cherry picking” 40 years ago at their current mines. You only get to do it once. But during that “once” the market tends to reward growth rates that can approximate parabolic growth. Barrick’s concerns are more aligned with replacing the ounces they are currently mining by stocking their pipeline with new projects. They’re going to have to divert a lot of todays profits into those new projects. Auryn doesn’t have to do that yet.

Auryn could easily have 10 or so years of dynamic growth that Barrick could only dream about. But Auryn’s production rate will eventually plateau out as it always does for miners. The market will pay a handsome P/E ratio at first for all of that growth and later it will pay less. It’s true that the shareholders of Auryn might not sleep as well as the Barrick shareholders UNTIL those first couple of working sites are cranking out production.

Ok. Let’s cherry pick the segment of precious metals that has the highest P/E. But while we’re doing so, it’s probably important to include certain discount factors like 1) no production to date 2) no working capital with the exception of personal loans from a director 3) no permit in hand for exploitation beyond bulk sampling 4) no onsite plant (toll milling) 5) no defined resource. If you apply the discount factors to the “fundamental” valuation you end up with a highly discounted valuation. Most importantly, as anybody who has actual investment experience in this sector will tell you, you don’t get a 20, 30, or 40 multiple unless you have some visibility on “life-of-mine”. I’m not saying that you need to have 30 years of reserves and a mine plan in place to support a 30x PE but to make the giant leap of ZERO knowledge to any life-of-mine to an industry standard (according to you) 30 P/E is misplaced. To be VERY polite.

But hey, a professor said it looks like it will be a world class deposit, and the historical grades clearly show this will be the highest grading mine, ever…Why doens’t the market get it? Bunch of dummies.

Find me another precious metals comapny trading at a $500M+ market cap with ~20koz of annual production (currently at zero) and no defined resource and I’ll disappear into the Metaverse.

Could you SPECIFICALLY address which item in my analysis you have a problem with. I also don’t understand how you can multiply $8 by 70 million shares and get an $800 to a $1 billion market cap. Thank you in advance.

Lot’s of discussion/speculation on similarities to El Penon which is certainly a WCD based on a professor kicking some rocks and putting his thumb in the air.

I’m happy to be labeled a grinch. Just trying to add a little reality to this cocktail. Talks of 30 PE average multiples (total joke) etc, etc are more down the alley of Santa Claus Way. I enjoy reading some of BB’s geo “what ifs” as much as the next guy but, in all honesty, if his type of analysis was offered anywhere outside of the forgiving walls of this message board, he would be laughed out of the room. I don’t see any harm calling this out unless participation here is as a means to a support group vs. debating the merits of an invesment.

When Auryn begins officially confirming the grades, offers a timeline on increasing working faces mined, and presents an earnings forecast, then pps will multiply.

Your analysis is appreciated because it offers AUMC/MDMN investors a sneak peak before the company begins putting out similar figures and expectations.

Like you have said many times, Auryn is bypassing fancy Feasibility Studies and instead getting straight to turning a profit. So for me the next big thing I’m waiting on is when the company feels confident enough to put out an earnings forecast. That will be a significant development for the stock price.

Reading this message board is comparable to the broadcast of the BBC during World War II . Most is just idle chit chat, with hidden messages secretly

imbedded for the partisans among us. Be they on either side.

One of the forum participants recently was kind enough to post an interview with Eric Sprott. Sprott somewhat chided mining investors for not doing the basics of investing in this sector when it comes to vein deposits. He stated that it’s really pretty simple; you take the strike length of the vein, multiply it by the average width of the vein as best as you could determine and then multiply that by the estimated depth of the vein. This gives you the volume of the vein in terms of cubic meters. You then multiply that by the estimated density or specific gravity of the ore. This gives you the tonnage of the deposit in terms of metric “Tonnes” with a capital “T”. You then multiply that by the estimated average grade of the deposit in terms of ounces per Tonne. This gives you a very rough ballpark number of the number of contained ounces of gold within the deposit.

This is a way to do some preliminary “screening” of a potential mining investment. It also provides a ballpark estimate of the potential mine life of the deposit. In the case of the Don Luis1 Vein, there are many, many hundreds of pages of information that have been provided by at least 27 Professional Geoscientists from a variety of entities (especially Enami and their predecessor CCM). If you can’t come up with a minimum of 2 million ounces of gold in this one vein and perhaps a projected mine life of 20 to 40 years then something isn’t right. If you want the company to spend $30 million-plus in providing you with the EXACT amount of ounces and EXACT number of years of projected mine life then you came upon the wrong investment and wrong management team. You either have done your homework and can trust your gut or you can’t. If you can’t and you like the mining sector then buy shares of Barrick.

What you can’t do is conflate the way to do due diligence on a major like Barrick and a junior like Auryn. It won’t work. The big money in this sector is made BEFORE a junior with a discovery dilutes its share structure to death by being FORCED by circumstances, namely no early production opportunities, to do what is necessary to attract a major miner. The Board of Directors of the major is going to want a completed drill program and an NI 43-101 compliant feasibility study formally defining Mineral Reserves and Mineral Resources (MR/MR). That’s just how it works in this sector. This covers the butt of the Directors should they make a decision to enter into a strategic alliance with the junior. They want the project to be DERISKED and they want the shareholders of the junior to absorb the damages from this process i.e. massive levels of DILUTION of either their share structure or the junior’s percentage of ownership of the project. The shareholders of the major deserve a good night’s sleep; their potential rewards are somewhat limited as was their risk.

Auryn got lucky, most projects that a junior stumbles upon don’t have many hundreds of pages of corroborating information available from a variety of Professional Geoscientists. They don’t have an existing mine infrastructure consisting of 156 meters of existing shafts, 162 meters of chimneys, and 535 meters of drifting and access levels THAT HAVE ALREADY BEEN SAMPLED TO DEATH BY A VAST NUMBER OF PROFESSIONAL GEOSCIENTISTS AS WELL AS THE LIKES OF SILLITOE AND OTHER AURYN P. GEOS. The standards and guidelines for blocking out ounces of MR/MR allow the QP (“Qualified Professional”) to use prior production results, sampling from existing mine workings, drill results as long as they’re tightly-spaced and trenching results from surface. The question boils down to whether or not the information available to either Auryn management or to a prospective investor is sufficient to contemplate an investment to an investor or to justify putting the project into development for management. Management made a decision. It is “feasible” for us to put this project into production WITHOUT LEARNING THE EXACT NUMBER OF OUNCES OF GOLD PRESENT OR THE EXACT NUMBER OF YEARS OF MINE LIFE AVAILABLE WHILE BYPASSING THE DILUTION INVOLVED IN FINDING OUT THE SPECIFICS. In one sense, mining isn’t that complicated. The goal is to get the contents of the deposit into the mill and the cash into the bank as long as it has been determined to be “FEASIBLE” to do so by the risk takers. If you’ve been blessed with the presence of a bunch of access adits/tunnels and the ability to determine where the goods are located then go for it WITH AN INSANELY LOW NUMBER OF SHARES OUTSTANDING TO BOLSTER EARNINGS PER SHARE AND THEREFORE SHARE PRICE. You have the option of getting the ore to the mill NOW or 5 years from now with a much more bloated share structure but with a higher level of knowledge of the details. Management does NOT need a drill program to identify worthy targets. The Larrissa and Antonino Adits as well as the prior Fortuna Mine workings have provided a smorgasbord of options.

Management has already stated that they intend to provide MR/MR numbers in this current Q-4 of 2021. Auryn’s Luciano Bocanegra already released a preliminary resource estimate of 664,000 ounces of gold in just the top 200 meters of the DL1 and Merlin-1 Veins. This was completed several years ago prior to the drifting of the Antonino Adit and all that it uncovered. Enami’s P. Geos already provided a longitudinal cross-section of the existing works at the Fortuna Mine. This is not available on the Internet, I had to purchase a copy several years ago. Their geoscientists already blocked out triangular shaped ore blocks “A thru N” that they recommended being developed first. The prior owners were not able to follow through due to a variety of reasons, some financial and some political.

Don’t swallow the red herring that “without formal MR/MR you can’t estimate mine life or identify production opportunities.” Management didn’t ask us to take that risk; they took it by agreeing to not being paid back the cash they advanced UNTIL the profits from the mine permitted that.

If you aren’t kidding, you really should be embarrassed making this statement. The market nor any financier will place any value on some historical data used to extrapolate resources. This is exactly why regulation fell into place post Bre-X requiring QPs etc.

This is also why Mauruzio couldn’t land any financing for three years (fact) and ultimately had to self finance as a result.

BB is right, it’s certainly possible to bootstrap an operation based on one’s “gut” but it’s a very, very long road as the project will have to expand organically. But you would, theoretically avoid dilution. What BB fails to realize is that Maurizio will jump at the chance to finance this thing (dilution) if the market ever gives him the chance. He’d be crazy no too.

Assuming that AUMC will self fund through the this entire process is naive. If the project turns out to have merit (a total guessing game without known resources) this will allow the company to raise equity.

None of my preceding comments are negative but rather industry standard realities. My biggest issue with AUMC is the valuation. This isn’t a $10M market cap exploration spec play that you can take a flyer on based on BB’s gut and some artisanal fun facts on grade. AUMC sports a very healthy $70M market cap so they need to execute and actually perform like a big boy company to grow into this valuation. That’s the only reason why I’m not long the stock at these levels.

Nothing wrong with his statement. Just because that is what a financier requires DOES NOT mean that reasonable estimates of resources and mine life cannot be made.

You said it yourself somewhere back in your posts, you agree that there are over 1 Million Oz of Gold. How the hell can you make that assertion without a technical report Baldy!

You’ve used google maps to show us ‘updates’ on the mountain activity.

I’m having a problem trying to get recent images of Havieron project & Artemis Res. recent Apollo drilling. The ‘google earth’ & ‘google earth pro’ maps are extremely outdated.

How are you able to get updated (recent) maps of the AURYN activities ?

Last fly over occurred in May 2021. The new workings are very obvious similar to photos provided by Auryn. However, I don’t see any other activity on the mountain at that time such as at the LDM, Caren etc suggesting that they are concentrating all their efforts on the development of the Fortuna mine.