Here’s a link to the type of deposit that the LDM might host. They’re called copper stratabound deposits and in Chile they’re referred to as “manto-type” deposits. Typically, they’re mined for their copper and silver contents. Hoch is big into silver and that might be what attracted them to the LDM. I would think they would be a thousand times more interested in JV-ing with Auryn on the very high-grade gold epithermals (mesothermals?) that Maurizio is going after. That’s their specialty i.e. underground vein mining. The cynical part of me says that Hoch did a JV on the LDM in order to backdoor their way into a deal on the very high-grade vein system. I have zero proof of that, however. IMO, we do NOT want to share those with anybody at this time unless and until the area near the confluence of the Merlin 3 which runs east to west, the Fortuna Oeste which runs NW to SE and the Fortuna Central which runs NNW are proven to be dense enough so that open pitting is deemed the right approach to exploit them. Auryn is currently (Q2) going after the much wider (2M) “massive” veins near the Merlin 3.

It’s obviously extremely exciting to be mining gold with the kinds of grades shown to date. Even at a miniscule 40 tpd rate a ton of money can be made. The real exciting part is getting in there in order to explore the subsurface aspects of that 5,000 meters of veins revealed in the trenching program that actually made it all of the way to surface. Every time they turn a corner, they seem to find a new extremely high-grade gold vein. The difference in the Merlin 3 area is that the veins average over 2 meters in width. In an underground tunnel, almost the entire working face of the adit will be vein material. If these are indeed “mesothermal” veins then they’re not only going to be likely to get wider with depth but also extend downwards a very, very long distance.

I would predict that the comfort levels of shareholders will go up immeasurably when cash flow information becomes available. Then as each day passes, the cash starts piling up and the investment community as well as the mining community takes notice. With cash flow, we can finally take pencil to paper and get a better feel for an appropriate price and market cap. In this exploration sector, until that point investors are kind of in the dark. From a risk/reward point of view, this is the sweet spot I should have been concentrating on over the last 40 years in this sector. Oh well!

I would suggest a somewhat different logistical approach as suggested by CHG a couple of years ago. It is also an explanation of why 5 years has been prominent in the initial loan to MDMN and also the Hochschild option. Excerpts are from Aug 18 post by CHG (see post #278 p Q3 2018) These are only excerpts from the post:

Pretty clearly, the original ‘LDM’, the Pegaso Nero, and probably the Gordon Pipe area are all included in the JV (3000 hectares). All of this is titled the “currently named LDM project” in the PR. Yellow marks indicate those new claims that were published this past May, obviously filling in some properties for the JV.

That leaves some 7500+ hectares for Auryn including the Caren, Merlin 1 (2, 3, 4, etc veins) and Fortuna plus quite a lot of undefined / unexplored stuff to the south going down the side of the mountain from there. ,…

… Note they could spend $7M and decide they don’t want to try and put the skarn into production, but still own 41% of that 3000 hectares. And they and Auryn could turn around and JV the PN to a bigger partner, with $7M of exploration already done, and potentially still make out with the copper / moly porphyry. Else if they define a nice skarn project and decide to spend that extra $23M, they can go into production for a while and JV at any time or explore themselves if interested.

In fact, you can note they basically split the south side of the mountain in two. If there is a porphyry right there where the Pegaso Nero is pointed, the property of both companies would obviously be involved in any future JV / mine etc. having to do with that target.

Hochschild has $750M in annual revenue or so. Legit to be sure and profitable (about $50M last year). On the other hand Freeport has about $16,000M ($16B) in revenue, so they are much much larger. I would guess Auryn got a better deal going this route than with FCM or anyone larger, being able to retain the potential gold production and 40% of the JV property worst case.

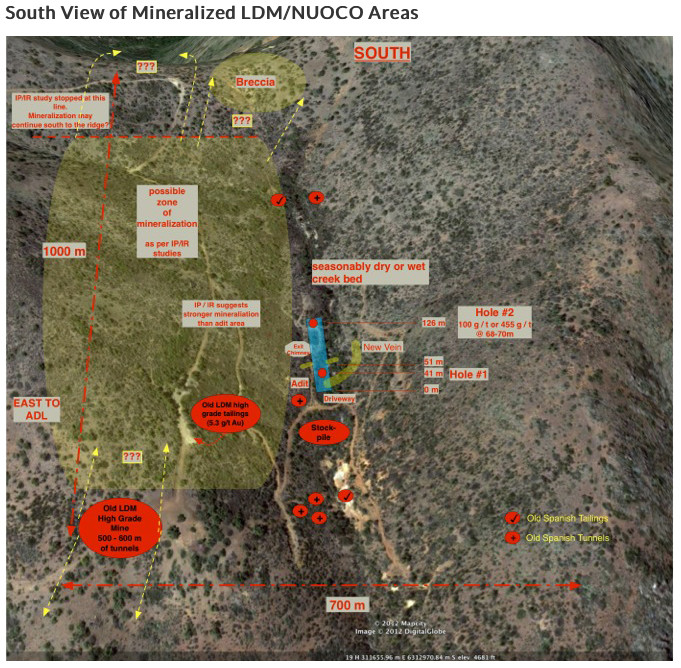

Back in 2015 CHG showed an LDM image detailing available information at the time. (Note the image below is portrayed “upside down” with South at the top):

From post #280 - an annotated image by CHG:

I believe the image below shows what that area looked liked earlier this year. It is around the area where NUOCO had an adit entrance for exploring the LDM. CHG can correct me on this if I’m mistaken, or add to his impression from several years ago what may be transpiring during the next couple of years regarding Hochschild. No apparent recent activity in this image that I can see.

Mints are running out of gold; not enough physical silver to cover paper - former U.S. Mint Director

(Kitco News) - A global shortage of physical gold and silver products has created a premium on coins and bars, and this premium is causing a disconnect between the spot price and the “true” price that retail investors need to pay, said Ed Moy, former director of the U.S. Mint.

Moy, who was the director of the U.S. Mint between 2006 and 2011, cites the inability of the mints around the world to keep up with physical coin and bar demand as a reason for this shortage.

“Not only the U.S. Mint, but other Mints around the world, Australia’s Perth Mint, the Mexican Mint, have all run out of gold, they can’t keep it in spot and there’s so many shortages retailers are having problems accessing that gold,” Moy told Michelle Makori, Kitco’s editor-in-chief.

Premiums on these physical gold and silver products can run as high as 20% in some places, Moy said.

Formations below the surface like this cross section of a lava flow mountain, is why the buyers want the claims drilled out.

To try to determine, just where, the goods are?

They want you have to prove it up for them someway…

Geology and Genesis of Major Copper Deposits and Districts of the World A Tribute to Richard H. Sillitoe

January 2012

DOI:10.5382/SP.16

ISBN: 978-1-6294-9041-0

Authors:

Jeffrey Hedenquist at University of Ottawa

Michael Harris

Francisco Camus

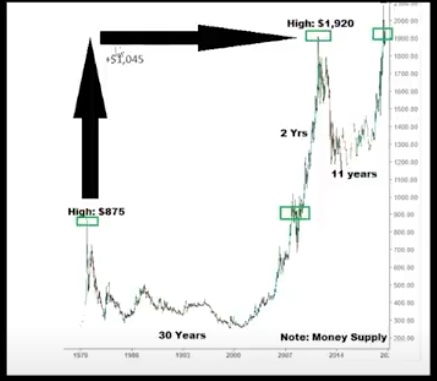

Very nice chart. Thanks for posting. For those that don’t have time to research further, here’s a shorter term chart projection by Gareth Soloway (May 11 - Palisades Gold). Gareth gave a two year time frame for the move to $2965 to take place, FWIW.

What the chart shows is that the move from $875 to gold’s high of $1,920 (i.e. $1,045) yields the projection to $2965. Just adding the $1,065 to $1,920 = $2965. Using this method for the megacycle that many are saying we are in the early stages of yields the very high projections over larger time frames. No one really knows what factors or how long it will take for gold to reach the stratospheric levels that keep appearing in articles, but many think it will be quite sudden.

(addendum - the above is just a simple additive method to project the next high resistance level. I believe using Fibonacci would use the 1.62 factor on the $1,045 which would yield $ 3,613 for the next projected high on a longer time interval. On a megamove some would use a 2.62 factor which would yield $4,658, but who knows what the future may hold. Maybe TR can comment on that.)