And withdrawn less than a month later??? What does this say about their MO in regards to earlier handiwork in “distressed” stocks? The following monthly chart of MDMN shows more than 536 million shares traded this month. Anyone care to guess who might have been accumulating as others were selling?

Maybe Auryn loading up more, preparing for something delicious!

3 Likes

Buying started picking up again towards the end of the day.

1 Like

I guess its worth pointing out that any price action in MDMN is noise unless you are actively trading it. The only way to ascertain the value of your MDMN shares is by following AUMC. I realize AUMC is thin and nobody is going to try to run the stock. However, the percentage of AUMC that MDMN owns is ultimately valued based on the value of AUMC. If MDMN goes to a $1 and AUMC is still at 75 cents you will be very disappointed if you hold shares in MDMN post the distribution as that $1 will go to nothing and the distribution received is pegged to wherever AUMC is being value. As has been witnessed over the past several weeks, 100’s of million traded in MDMN hasnb’t effected the AUMC volume much. So this volume is a “cap structure”, technical play vs. anything fundamental, and there’s really no opportunity to arbitrage b/w MDMN and AUMC

5 Likes

THE CONTINUING EDUCATION OF THE MARKET FOOL

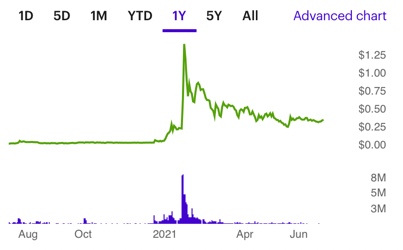

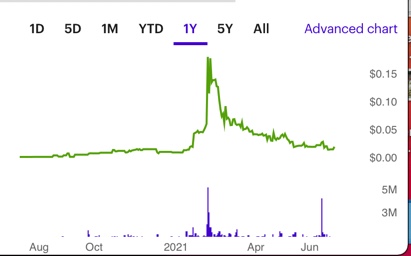

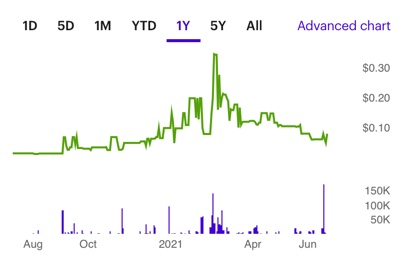

Below are E-trade’s graphs for the “last twelve months” for each of the four stocks Harvard/Wharton played with:

AMLM:

APLD:

OKSA:

CATG:

And here is the “last twelve months” graph for MDMN:

– madmen

Further reading says the parties have agreed to have further discussion/communications and thus they have decided to vacate the motion for now.

2 Likes

Here’s an example of a Court Appointed Custodian action in the state of Nevada and how it led to control in this case: https://sec.report/otc/financial-report/286108

1 Like

Here’s an article that discusses Custodianship Proceedings used via unwitting state judges to take control of idle public shell companies. Apparently this tactic is a thing and has been around for quite a while: https://www.securitieslawyer101.com/2018/custodianship-shells-and-reverse-mergers/

1 Like

MDMN’s “Dark or Defunct” flag on the OTC market is like an advertisement inviting such a scheme. MDMN having an actual potentially very valuable asset makes it all the better from the schemer’s point of view. … Maybe Les gave Barbara a call … :-). “… and then there’s this great thing called ‘next week’”

1 Like

The problem I see is if the Baumans revive the suit it may very well throw a monkey wrench into whatever timing AUMC had in mind for distribution to shareholders. All the Baumans have to do is successfully represent to an easily persuaded judge a negative measure of performance without presenting the true reflection of long-term economic value. Apparently the Bauman team is quite experienced in dealing with similar legal maneuverings. Medinah definitely needs to do whatever is necessary to be represented. I’m quite sure Medinah and Auryn have far too much at stake to allow this to go further than it already has. The Bauman lawsuit and attempted takeover by Court Appointed Custodian action has assuredly had a very negative effect on many current shareholders.

2 Likes

Easy they vacated the application so looks like Baumann is No longer moving forward. So I take that as good news

3 Likes

I assume this is confirming that MDMN is in fact NOT absentee…

2 Likes

Thanks Wiz. Much Appreciated!

Again, thanks for providing the explanation. MDMN and it’s shareholders are fully represented with standing in NV. The Bauman’s Application for the Appointment of Custodian is unlikely to be little more than a ripple after the July 1 hearing was Vacated. The Baumans would be foolish to refile this Custodian claim in court again after having been contacted by Medinah’s (Auryn’s) legal team. The original filing caused quite a commotion though and probably damaged a number of shareholders by inducing panic selling.

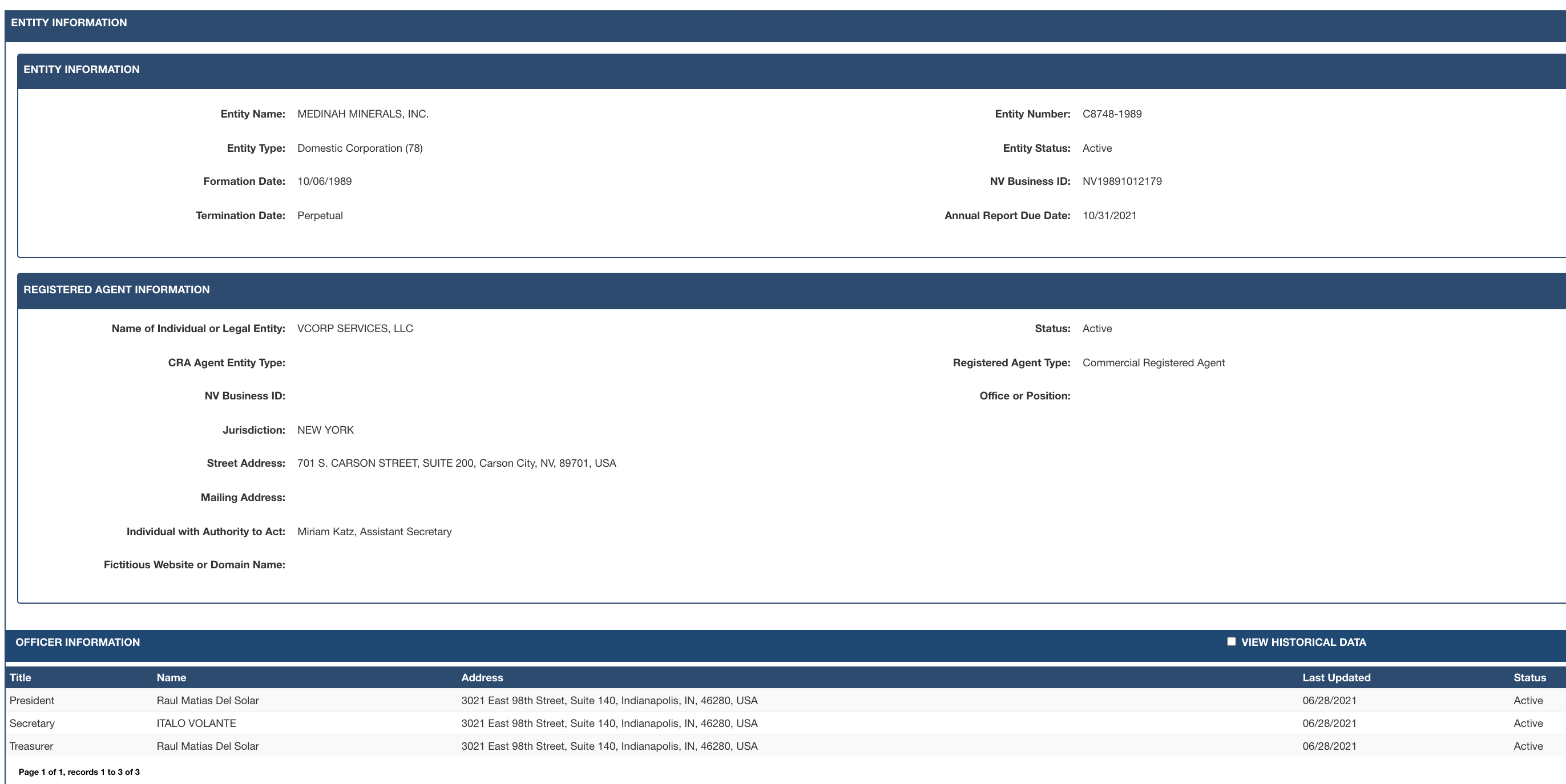

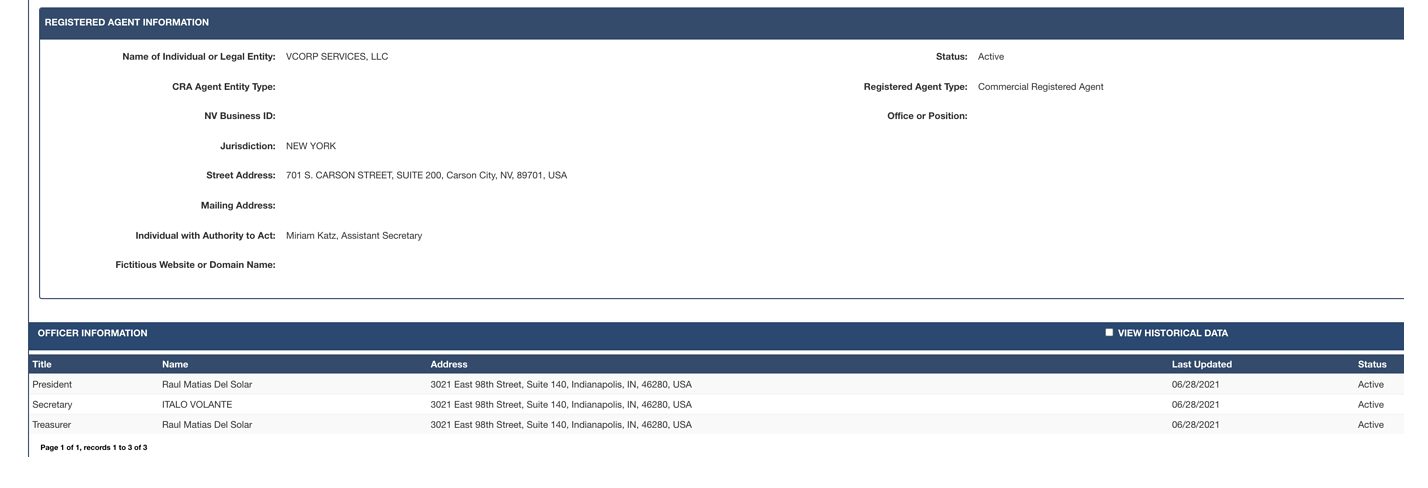

VCorp Services - “Enabling organizations to ensure adherence with ever-changing regulatory obligations, manage risk, increase efficiency, and produce better business outcomes.”

3 Likes

The Annual Report requirement is ministerial in nature, aimed mainly at keeping a public record of the agent for service of process (for lawsuit purposes) and various other public notice-type stuff. I have to say I’m a little disappointed our guys were not properly keeping up with this - the expense is relatively immaterial and a failure to comply can cause drama, as we all now know. I deal with this requirement on a daily basis, as proper compliance in this area can have an affect on tax issues - but I had no idea that there was a cottage industry out there of attorneys creating (or hijacking) these shells for sale to the highest bidder. Bottom feeders. Disgusting really. I feel sorry for the people who bought in early yesterday, thinking “this was it”, only to learn of this little game that was being played. Unfortunately, I don’t know that they have any recourse against the perpetrators.

2 Likes

Good News that our AUMC shares are protected.

Potentially disappointing news is that all that volume looks to have been strictly day trader and shorterm opportunists looking to make money off a Bauman play.

The positive here is that the company is not leaking out info which was one speculation of some. Here’s to hoping we get a nice positive quarterly update to push us up another level.

5 Likes

Hi Jimmyp,

Medinah is a bit of an enigma. For the time being it is simply a HOLDING COMPANY. It “holds” 16-plus million shares of AUMC. On paper, you’ve got a PinkSheet issuer that has “gone dark” and is no longer filing Form 211s. I don’t think it does its annual filings with the SOS of Nevada either. It has 2.9 billion shares outstanding and it is bumping its head on a 3 billion share authorized share cap. To Joe Public it looks like its on its deathbed. The reality is that it shouldn’t be filing Form 211s and it shouldn’t be doing the annual filings with the SOS of Nevada. Those expenses would be silly for a holding company like Medinah. Auryn does all of those filings already. The default assumption of Joe Public might be that the 16-plus million shares of AUMC are probably worthless and that Medinah really might be on its corporate deathbed. Management is making the correct moves but the correct moves create the misrepresentation that there are no assets.

The delays in the distribution of the AUMC shares also represents the correct move if management knows that the share price of AUMC is about to take off. Medinah is going to pay off its debt via the sale of a handful of AUMC shares. The more patience management has in distributing to the Medinah shareholders their shares the greater the amount of shares that will be headed to each shareholder. Less of those 16-plus million shares will need to be sold in order to satisfy the debt. Another thing that people don’t realize is that Medinah’s debt is noninterest bearing. Joe Public probably assumes that it is interest bearing further enforcing the potential deathbed scenario. There is no clock ticking in the background putting pressure on management to distribute those AUMC shares. I would also assume that Joe Public also assumes that the money that management is fronting to Auryn in order to go into production is interest bearing. It is not. Currently, there is a long list of DISCONNECTS between reality and what Joe Public might assume. Perhaps even a Harvard Law grad and a Wharton grad also failed to see these DISCONNECTS. Being active in the mining sector then again perhaps they did realize that the Medinah assets were for real. Who knows?

I think that all of these various DISCONNECTS result in a DISCONNECT between Medinah’s share price and market cap and developments on the ground. For people unfamiliar with geology and the ADL Mining District, that potential deathbed scenario is a tough possibility to get past and make an investment. Joe Public might sense that the definitive share structure of Medinah and Auryn is a big mystery. No it’s not. You take the number of AUMC shares in Medinah’s treasury. You subtract out the handful needing to be sold in order to satisfy Medinah’s debt. You then distribute the remaining shares pro rata to the owners of Medinah’s 2.9 billion shares. Medinah management was smart enough to turn their monthly burn rate to near zero. That’s why they “went dark” and no longer pay lawyers and accountants to file Form 211s when Auryn is already filing them. Medinah is already bumping their head on their 3 billion share authorized share cap. They can’t issue more shares without holding an AGM. Joe Public doesn’t know this. Auryn is extremely stingy on issuing more shares than the current 70 million outstanding. How do we know this? They’re fronting money to go into production via noninterest bearing loans and they agreed to hold off on being paid back until cash flow is positive. Joe Public doesn’t know this.

It’s kind of a strange scenario when correct, even brilliant management choices, result in the perception of a corporate deathbed scenario. It is what it is……for now.

8 Likes

Doc I still hold mdmn certs, how will they be handled in the distribution

With this latest snafu I (we) just witnessed, I thought I was back on the old buss that used to run between the army base, I was on and town. Just after pay day, watching the ole three card shuffle being played on the newbies.

Same game… just higher stakes.

… …So still some A Holes out there.

I guess. Well back to the creek to pan some gravel.

If you watched the trading yesterday, it’s not suprising that MDMN stuck at .004 for a considerable amount of the volume (16m sharres of AUMC at 75 cents/ 3b shares of MDMN = .004)…this mini “corporate takeover” probably assigned this value as their ceiling and picked up as many shares at that level until they abandoned ship. This would have given them the AUMC value and the shell and NOLs for free. Starting to make more sense but I still struggle with how anyone (of any technical depth) could value AUMC for any amount (high or low) and the headache of accumulating that many shares with existing liaibilities seems like a tall task. Perhaps that is why it didn’t move forward.

3 Likes