Please disregard my previous confusing post. I have answered my own question.

1 Like

Not sure how to make a new post, sorry.

A friend of mine who’s also a MDMN shareholder raised the question: If Auryn is calling it a dividend instead of a conversion does that raise the possibility that there may be future, possibly yearly, dividends as well?

Thanks for any comments and insight.

This is Medinah issuing the dividend, not Auryn, and it’s a one-time dividend to put AUMC shares in our hands so that Medinah can dissolve or otherwise terminate itself. All of the value MDMN has is in the AUMC shares, so once they distribute those MDMN will essentially be no more, so there will be no more dividends from MDMN after this one.

1 Like

Thank you, TR.

2 Likes

TR is correct, this is a one-timer.

But, do recall that a recent news release by AUMC discussed their goal of commencing gold production at the rate of 40 tons per day. And, I think they mentioned the number 2.5 grams per ton somewhere along the way. If you multiply all that out, there could possibly be some money to distribute as dividends.

40 tons per day

x 2.5 grams per ton

x 350 days per year

x 95% recovery rate

/ 31.1035 grams per troy ounce

x $800.00 profit per ounce (maybe)

x 23% (MDMN’s portion?)

/ 2,880,000,000 shares outstanding

.000068 per share dividend (not considering taxes or anything else)

THE GOOD NEWS: If you have 1,000,000 shares of MDMN, then you might get 68.30 per year, don’t spend it all in one place - bwahahahahaha!

Now, if the head grade turns out to be along the lines of what they saw historically at the Fortuna, then things could change … maybe - you have to remember this is MDMN!

Well Bubba, I would just love to receive $680.00 a year per million shares of MDMN, because I’d be able to recoup my MDMN investment in approximately 184 years, but I think your wishful thinking hijacked your post and stuck a zero in there between the 8 and the decimal. Unfortunately I think the math part of your brain intended to type $68.00 instead of $680.00. ![]()

1 Like

Correct - I fixed it while you were responding - I wouldn’t want to be responsible for breaking anybody’s heart - bwahahahaha!

Mr. B.,

You math is wrong! Its not 2.5 grams per ton. Its up to 85 grams per ton.

This works out to .0023 per share; not bad at all!

2 Likes

Correct. They would not mine 2.5 g/t as they would not have that profit you show. They would lose money and thus not mine.

Well, God bless you Mike - but if that happens then things will FINALLY be looking … UP … for us. Would love to see that, but I wonder HOW MUCH of that level of mineralized ore is hanging around the Fortuna. Is it just that pile we have a picture of on the website, or is there more to be had?

You’re an old-timer here, aren’t you, Photoguy?

So you already know that Absolutely Everything is possible in Medinahville.

A crook sneaking down the back stairs of his hotel in Santiago, on his way to sign the final final final papers at the notario, can stumble, tumble, wind up in the hospital, put out a plea for Christian prayers, and people (right here on this very forum!) will believe and put in a good word for him!

I can’t wait for someone to write the screenplay.

Where will all this madness be filmed? Las Vegas? Vancouver? On the Alto? Or will the Alto be an open pit by then, with the spectacular Andean scenery marred by a line of monster trucks sagging under the weight of tons of pure gold?

Who will play Baldy? Who will play Brecciaboy? Who will play Wizard? Maurizio? Who will play what’s-his-name, the billionaire playboy from Sweden or wherever it was? (Remember FOAD?) Who will play Photoguy? And most importantly, will Brad Pitt be available to play

– madmen?

Outside the Oct 1, 2016, shareholders meeting in Las Vegas:

Inside:

Onscreen at front of room:

3 Likes

I am reading through the old 1999 Fortuna property report. There are lots of interesting tidbits but here are a few:

-

Auryn’s current 54 tonnes of ore is more than was mined in Fortuna in any of the last 3 years of recorded production in the 1941 to 1955 period: 1951, 1952, 1955.

-

40 tonnes per day times say 300 days / year would be 12,000 tonnes per year, more than 30x more than any recorded production year.

-

Auryn’s claim of “over 2 oz/ton” is right in line with the grades reported as produced in those later years. 85 g/t would be greater than any recorded years of production 1941-1955. One has to wonder how many tonnes Auryn thinks there are at this grade since it is so high relative to earlier production.

-

Auryn claims they are mining “free gold” without blasting, for at least the 54 tonnes so far. Did they find a hot spot of limited scope? Or do they think they can actually mine those 40 tonnes per day at around this 85 g/t grade?

4 Likes

This is the report: Geological Report on the Fortuna Gold - Cerro Dorado, Inc. (Should note the only a small portion of the mine was accessible back in 1999 when this report was written. The main production vein was not reachable and wasn’t sampled.)

Looks like about 2000 tons of ore has been previously removed. In 1968, it was estimated that there was about 5000 tons of proven/probable reserves and another 4000 tons of possible reserves. It listed the amount of reserves in dumps as a question mark. Only a little mining was done after that time so I think we have a good starting point.(168 tons removed between 1968-1970 then nothing further.) The report lists that there was over 800 meters of old workings. Since the main vein(and other parallel veins which may be just as good) can be traced basically all the way across the plateau, it is safe to say that the vast majority of gold/silver/copper has yet to be exploited.

4 Likes

TR, don’t be shy. Tell us how you really feel!

2 Likes

I’ll try to do a better job from now on. ![]()

3 Likes

Wow Rich. I would have thought you had figured this out by now. I know, Florida, right?

1 Like

Oh it’s not FL… I’m just a slow learner, if not a no learner.

1 Like

Doc or anyone. Is there still a scenario where there could be short squeeze or shorts covering due to the dividend?

2 Likes

Hi JCN,

A few years back, I was asked to chair a committee on abusive naked short selling crimes. The committee members were stud muffin economists, lawyers, former DTC employees, etc. My first handout to the committee members was 4 inches thick. It reviewed the various securities laws being broken and how the crooks did their thing. Basically, what they did was to lever the complexities of our clearance and settlement system so that the average Main Street investor didn’t know what hit him. One of the policies we adopted was to encourage small corporations under attack to NOT promote the purchase of their shares because of an imminent short squeeze. What we found was that assetless corporations with corrupt management teams would market their shares by pseudo-promising “the mother of all short squeezes”. This allowed the Wall Street crooks to point out how invalid the claims were of these assetless corporations when they yelled out “We’re under attack”. This ended up undercutting the efforts of truly abused corporations to fight off abusive naked short selling. When Wall Street circles the wagons, they’re pretty tough to take on.

The more predictable way to take on the crooks is to simply keep your nose to the grindstone and concentrate on building your corporation. I have nothing but respect for the job that the current Medinah and Auryn management teams have done. They wisely structured matters so that Medinah would become a mere “holding company”. They shut down the monthly burn rate to pretty much ZERO by “going dark” and not paying accountants and lawyers to provide the 15c-2-11 informational disclosures and not keeping up compliance with the Secretary of State of Nevada’s annual filing requirements. Although this was absolutely the correct strategic move to make, it had an untoward side effect. It made Medinah look like it was on its corporate deathbed because many ASSETLESS corporations do the exact same thing as they head off into insolvency. The cause of death of the ASSETLESS junior corporations heading off into insolvency is DILUTION and lack of CREDIBILITY. The COST OF CAPITAL for ASSETLESS corporations goes through the roof. Many financings are structured as “death spiral financings”. That’s if they can find a willing financier in the first place.

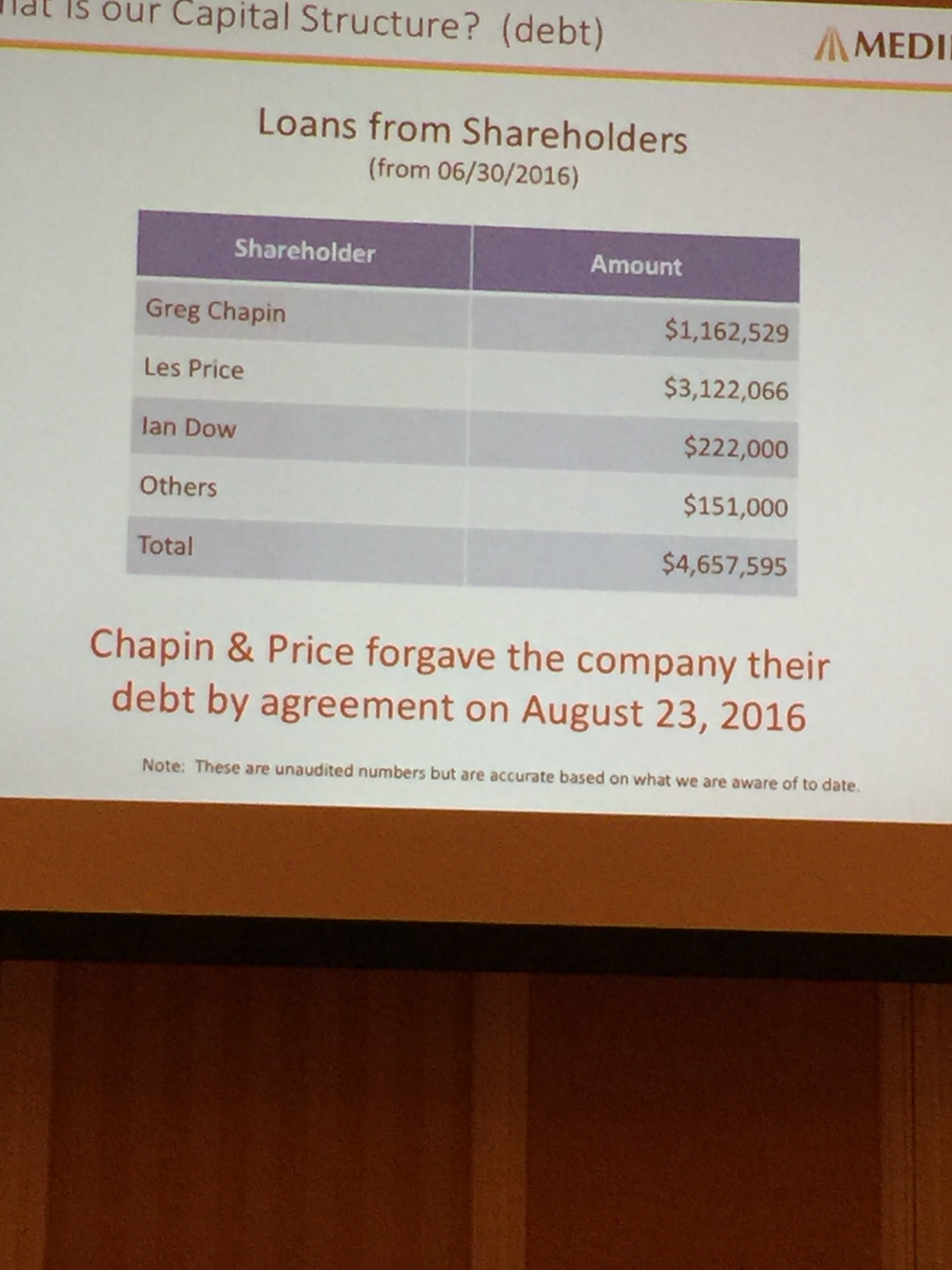

Think of Medinah as a safe deposit box with 16-plus million shares of “AUMC” and 11-plus million shares of “AMNP”. “AMNP” owns the Caren and Puange placer properties bordering the ADL Mining District to the north. They also have 4 other groups of mining concessions some of which are situated near recent discoveries. Maurizio already owns the Colliguay properties bordering the Caren and Puange to their north. As a mere “holding company” Medinah has no operations. They have no monthly burn rate. What little debt they have is noninterest bearing. This is important to understand. There is no interest clock ticking in the background. The debt has no formal due date. Medinah can wait for the “AUMC” share price to rise with positive corporate developments and then pay off their debt with a minimal amount of “AUMC” shares. This leaves more for the remaining shareholders. The delays in distributing the “AUMC” shares, IMO, is a very good thing.

Contrary to the PERCEPTION to many that Medinah could be on its corporate deathbed (which is very understandable but inaccurate), management’s actions as well as the geological realities have pretty much rendered it immune to such a fate. Fortunately for the current buyers of shares, Medinah trades with a “potential corporate deathbed” discount attached to it. They will trade this way UNTIL the investment world gets their arms around the value of a 24% stake in the ADL Mining District as well as perhaps Maurizio’s overall game plan which he concocted with the help of Dick Sillitoe-the most accomplished geologist on the planet. The MISPERCEPTION in the markets leads to a DISCONNECT. Why? It’s because the value of the assets don’t even factor into the share price. Geological values are tough to estimate in the first place and I’ve been doing this for 40 years. At this point in time, mining investors won’t provide the time to evaluate the value of a 24% stake in the ADL. They have limited time to do due diligence and they can’t get past the PERCEPTION phase. There are 2,000 other junior explorers out there currently.

Currently, the graph of the value of the ADL is going on a nice trajectory due to geological developments. The graph of the share price is on a different trajectory probably UNTIL production is established and the grades confirmed. Then there could be a whiplash effect independent of any naked short selling issues. IMO, the key historical reality is that the average Medinah shareholder needs somewhere around a “10-bagger” to get back to even. The question becomes, are these folks going to suddenly sell after they experience a triple or quadruple from today’s share price levels or are they going to hold on until they’re closer to breaking even? Contrast this scenario with a situation in which the average shareholder is sitting on a triple already just looking for an exit sign to flash.

What I’ve noticed in recent conversations with larger Medinah shareholders is that people don’t have much experience with investing in “holding companies” versus operating companies. The gigantic MISPERCEPTION we’re dealing with in regards to a potential deathbed scenario for Medinah might be easier to visualize if you consider that for Medinah to become insolvent then Auryn must become insolvent. But wait a minute, Auryn doesn’t share all of those scary characteristics of Medinah. They own 100% of the ADL. The value of the assets is on a nice trajectory with recent developments. They have 70 million shares outstanding not 2.9 billion shares. They don’t have past corporate governance miscues like Medinah is saddled with. They are current with all of their filings. Their management has proven the ability to consolidate many different groups of mining concessions throughout all of Chile. Some “related party” in the background is paying for all of Auryn’s annual property taxes and doesn’t want to be paid back. In mining, by far and away the single biggest breakthrough possible is GOING INTO PRODUCTION AND GENERATING POSITIVE CASH FLOW. The often-quoted statistic is that 1-in-1,000 junior explorers not only make a significant discovery but actually do what is necessary to get it into production.

8 Likes

Thank you sir.

1 Like