Let’s see if MC shares any positive news with shareholders that attend PDAC. That is if anyone besides BE is going.

Greetings to all in Mdmn land, been in the shadows for about 14 years, and I have a question I’m sure one of my fellow Medinahites can answer, how many outstanding shares are there with this stock? , and isnt there supposed to be a share issue, depending on the amount of shares a stockholder owns ? Sorry for if my poised questions arent quite asked correctly, but I’m sure the bright minds that are in this stock can differentiate my crude way of asking. TIA oneofakind5154

Gold up big again, that stockpile is appreciating by the day.

Plus they are in production according to BB (not in care/maintenance), so they keep adding to that stockpile daily.

1 Like

MDMN to AUMC will be somewhere around 200:1. But, that is assuming that MC doesn’t do anything that would change the value such as using stock to improve production. There is no timeframe when it will happen.

Also, the stockpile value ensures that we won’t have dilutive financing!

2.88 billion shares outstanding.

2 Likes

Hi One of a kind,

Welcome back, I think your timing might be prescient. Auryn has 70 million shares outstanding fully diluted. Medinah has 2.88 BB outstanding fully diluted. Medinah has a little bit of debt on the books (about $400K) that is zero interest debt. When you do the math, Auryn should be trading at about 200-times that of Medinah. Medinah is now a “holding company” (no operations of its own) which “holds” 16-plus million shares of Auryn which represents a 24% interest in Auryn’s shares.

Medinah’s plan is to sell a handful of Auryn shares to retire their debt after the share price of Auryn has advanced. This will allow that many more Auryn shares to be allocated to the Medinah shareholders. The remaining Auryn shares in the Medinah coffers will be distributed to the Medinah shareholders in a pro rata fashion. Once things get going, Auryn plans to seek a listing on a higher-trading venue than their current OTCMarkets “Pink Sheets” trading venue. This could be the OTCQB, the OTCQX, NASDAQ or possibly a Canadian or South American bolsa listing.

What you’ve missed out on lately is that Auryn’s game plan became to intersect the DL2 Vein at the point at which the previous artisanal miners ceased their operations. This was at about the 1,840 meters above sea level elevation which puts it about 110 meters below the plateau surface. The artisanal miners mined about 350-meters of the DL2 Vein on strike down to a depth of about 100-meters. This represents about 5% of the known dimensions of the vein. They averaged an astounding 64 gpt gold over the course of 30 years, involving the removal of 2,000 tonnes of ore. The average gold grade being mined worldwide today is 4.18 gpt gold.

Auryn successfully drifted an adit, the Antonino Adit, from the side of the mountain, at the proper elevation in order to intersect the DL2 Vein at the site where the artisanal miners ceased operations. They intersected 24 different “veins/structures” along the way. They intersected the DL2 Vein on 1/3/23. They sampled the vein at the intersection site via 2 groups of samplings. The first group of 4 “channel samples” averaged an off the chart 164 gpt gold. The second group of channel samples averaged 150 gpt gold. Later, Auryn did two smelter tests, one, completed at a lab in Lima, Peru, came in at 128 gpt gold and the other at the Enami smelter came in at 70 gpt “gold equivalent”. This second smelter test represents ore with a value of about $4,500 per tonne. Actually, after the recent move in the price of gold, it is now worth about $4,900 per tonne. Auryn also did extensive sampling of the DL2 Vein up higher in the vein structure within the “old works”. These samples averaged 85 gpt gold “without any blasting needing to be done”. Another sampling was done within the DL2 Vein where “Shaft A” ended near level 2. These 12 samples came in at an average of about 130 gpt gold.

During the “mining and stockpiling” phase, if Auryn has indeed been meeting their production guidance levels of 40 tpd for the 195 days they have been mining, then the tonnage of the stockpiled ore could be significant. This “sample size” could be statistically significant for us to much more accurately estimate the the intra-adit “HEAD GRADES” of the DL2 Vein ore. In mining, there are very well-accepted standards and guidelines in place to properly sample and assay stockpiled ore. If management can publish the results of a well-engineered study estimating the average grade, tonnage and total value of the stockpiled ore and if this value figure is a multiple of the current market cap for Auryn’s shares, then this might represent the catalyst for Auryn to get some attention.

The stellar grades accomplished by the artisanal miners (64 gpt gold) has clearly been corroborated by subsequent sampling where Auryn is currently mining. The key parameter for the 64 gpt gold vein was the “sample size” being 2,000 tonnes. This provides some statistical validity. Auryn learned that “froth flotation” was the best way to process their ore in order to remove unwanted “gangue” material. The testing suggested that if they were to process their own ore on-site, starting with froth flotation, they could make an extra $5,000 per tonne, over and above the $4,500-$4,900 per tonne the Enami smelter was willing to pay. The assumption here is that Auryn can average that 70 gpt “gold equivalent” figure.

Auryn now has the option to pay for their froth flotation circuit by shipping ore to the Enami smelter or by evaluating and accepting, any offers they receive for financing the construction of the plant.

In this interim timeframe, Auryn has been in “production and stockpiling” mode at their new DL2 Mine. Shareholders of Auryn and Medinah, have been suggesting that it would be informative for management to keep shareholders up to speed by revealing the tonnage, approximate grade and approximate value of the ore stockpiled to date. Auryn has been in “production and stockpiling” mode for about 195 days. Auryn management’s prior guidance was that they should be able to average 40 tonnes per day once they intersected the DL2 Vein, which they did, and were able to simultaneously mine 2 working faces.

THE FINANCING OF THE FROTH FLOTATION CIRCUIT

The 2 main options for funding the FF plant, appear to be going with an outside financier or funding it from within via selling extremely high-grade ore to the Codelco/Enami’s smelters. The problem with the latter is that they would be leaving about $5,000 per tonne on the table. It will be interesting to see if the recent upward movement in the price of gold (POG) to new all-time highs changes the calculus here or not. The “funding from within” option is now going to necessitate shipping a lot less ore to Enami’s smelters in order to pay off the construction of the FF plant.

The flip-side of that argument is that gold trading at all-time highs might improve the terms of any outside financing offer as any financier might perceive less RISK. As the value of the stockpiled ore increases, this possible “COLLATERAL” to any loan might open up the universe of potential financiers. The stockpiled ore plus the completed FF plant plus the fact that the value of the ore is going up $5,000 per tonne BECAUSE OF THE FF PLANT, would seem to constitute a fairly impressive package of collateral.

The BOD of Auryn recently unanimously approved the construction of the FF plant. Recent press releases revealed that the paperwork for the design of the plant was started in October of 2023. The preliminary on-site civil work was scheduled to commence in Q-4 of 2023. This aggressive timeframe suggests that management is not too concerned about not being able to pay for the facility.

From a shareholder point of view, the ideal funding might be a major or mid-tier miner paying for the facility in exchange for a piece of the action on one of Auryn’s many other ADL Mining District mineral assets, and the right to use the facility and the on-site assay lab it will house. This would allow Auryn to access that “extra” $5,000 via froth floating their own ore including the stockpiled ore.

HAS AURYN ALREADY LOCKED-IN A VICTORY, THE TERMS OF WHICH THEY JUST HAVEN’T LEARNED YET?

I would characterize the goals of “PHASE 1” of the DL2 Mine project as:

- Intersecting the DL2 Vein at the point where the artisanal miners ceased their mining efforts in 1970. This they achieved on 1/3/24.

- Corroborate the stellar grades of 64 gpt gold that the artisanal miners achieved. The grades found at the intersection of the DL2 Vein and the Antonino Adit not only corroborated those grades, but they greatly exceeded them.

- Construct a new ventilation system and safety egress system by accessing the 7 ventilation shafts and 5 ventilation chimneys contained within the “old works” (levels 0,1, and 2) where the artisanal miners had been working. This has been accomplished.

- Get SERNAGEOMIN (the Chilean Mining Authority) to sign off on this new structure so that Auryn could safely mine at the various sub levels under this new “level 3” of the mine. This has been accomplished.

- Finish the new “ANTONINO PRODUCTION ADIT” which will serve as the haulage adit for delivering the mined ore to the surface. This has been accomplished.

- Finish all of these tasks while maintaining 100% ownership of the entire ADL Mining District as well as only 70 million shares issued and outstanding. This has been accomplished.

- Be ready to ship ore when the price of gold is at favorable levels. This has been accomplished if they opt to fund from within.

I would suggest that Auryn has already locked in a victory, the rewards of which are yet to be defined.

Phase 2 would involve enhancing the already extremely high intra-adit “head grades” via dialing-in the ore purification processes such as froth flotation, perhaps carbon in leach, etc. This will get the ALL IN SUSTAINING COSTS (AISCs) down and therefore the marginal profits up.

Phase 3, I assume, would include MARKETING all of these accomplishments. Management has done pretty much ZERO marketing to date.

5 Likes

This poor guy/gal (oneofakind) shows up for the first time in 8 years to ask about the current sharecount in MDMN and the good old doc can’t resist the temptation of regurgitating HIS version of what is happening at the company.

Another set of premature victory flags, “mission accomplished”, the market just doesn’t get it, etc, etc. What if Oneofakind, who was simply checking up on an investment that is already down 99% becomes convinced that he should now double/triple/quadraduple down based on the wildly optimistic developments offered by BB? Will BB apologize when those points are negated? No. Will BB offer, as a caveat to everything offered on this board, that these are conclusions he has made up (again) without any feedback from the company? No

As a positive:

-

it shouldn’t be a long wait for investors to realize the false narrative being spun. Hopefully, accountability will be mandated and the narrative remedied/grounded.

-

given that MDMN is already trading at basically zero, the harm inflicted by sucking more investors into this stock with misinformation, at this point, has been blunted. There’s, by definition, not much downside. This is very different from years in the past but that damage has already been done.

-

the company doesn’t have to meet these ridiculous forecasts for the share price to stabilize and/or even appreciate in value. Both AUMC/MDMN have finally reached a valuation that properly discounts the investment opportunity: a call option. The nice thing about this call option is that it doesn’t expire (unless Maurizio packs his bags).

However, similar to any individual who falsely accuses the company of wrongdoings for financial gain (shorts, lower entry point, etc), I believe false assumptions of accomplishments that have not met or predictions for metrics that could never be met, should carry equal accountability.

If and when Maurizio gets this thing into production and begins to make company forecasts and set milestones, the “riffraff” needs to be dealt with to ensure normalcy across investor sentiment.

3 Likes

Hey John, did you meet up with MC at PDAC? If so, anything you can share with us shareholders without breaking the NDA you have with him?

Its me again, oneofakind5154, yes…back when I first got into this stock, I was obsessed with it, being totally ignorant of how to invest, and drinking the koolaid, I took my 401k in to it, which shortly after, and through a divorce, the ex took it all…but after a spell, and Mdmn going sub penny, I treated more 401k monies like Monopoly money and have purchased mutiple millions of shares, and have averaged my cost to .0012 per share. When I asked how many shares were outstanding, I was just curious of what portion of Mdmn do I own?? Being 60 years of age as of yesterday, and hearing about the frothing plant to possibly being built, I’m just hoping for a possible pot of gold at the end of this rainbow scenario. Mutiple shareholders have not lasted above ground to see their shares come to a possible fruitful blossom, and enjoy their rewards, after making healthy purchases. I wish I never invested in this stock…my financial standing would have been better off, but I’m an optimist, and not always the wisest, never the less invested, and hoping this froth plant gets built, and wanting to see ore processed to the benefit of our shareholders. If this all comes to pass, I’m curious, what is a possible share price that could become of this stock, or is Auryn going to be the great benifactor? My apologies for my jumping around of topics, just a optimistic ignorant speculator ,when it comes to investing. I digress, and wish you all a wonderful adventure. I’d love to get back to the .10-.15 cents per share ,when I first stumbled upon this stock, will we get there ,or above? I know that there are formulas, but that’s not my expertise…what says the members…I open it up to you all.

1 Like

I too fall under the same category! 60…. Been invested in this foolishness way to long to not hang in! We deserve some actual answers.

We listen and try to stay upbeat when Doc and others give us their spin but we would like to see some follow through. There has been a lot of $$ invested between these two companies over the years without any rainbows appearing!

2 Likes

I consider brecciaboy absolutely delusional after three decades of his outerspace projections. I guess it’s his catharsis for losing all that money like the rest of us.

1 Like

A few weeks ago I speculated we’d see a gravity circuit built into the mill but missed something important in some earlier information the company had already presented to us:

So what was I missing? Perhaps you can spot it in the following:

Caren Mining Preparation Commences

Jun 16, 2016

Metallurgical tests conducted at laboratories in Perú returned an average gold recovery greater than 90%. Test conditions confirmed the best recovery method entails use of a Falcon gravimetric system processing previously concentrated ore.

Caren Mining Preparation Commences | AURYN Mining Corporation

These results make us confident that we can produce a total of 5,000 troy ounces of gold before year-end 2016, and over 25,000 troy ounces in 2017.

I now see why this headline below was not followed up on:

Update on bonanza gold grades in Caren mine, have returned over 100 g/t Au at Fortuna – Merlin system in the Altos de Lipangue project, Chile.

Jan 27, 2016

Table 1 shows that the main bonanza grades are in samples collected in the Adit #2 at meter level 1,840 and in Adit #1 at meter level 1,875.

Update on bonanza gold grades in Caren mine, have returned over 100 g/t Au at Fortuna - Merlin system in the Altos de Lipangue project, Chile. | AURYN Mining Corporation

Note from the previous June 16, 2016 notification; “Test conditions confirmed the best recovery method entails use of a Falcon gravimetric system processing previously concentrated ore.”

That’s right, the ore had to be concentrated before the gravimetric processing was applied! So, what does that mean concerning the mill that is being planned? It was earlier, in the September 17, 2015 notification, that the goal to prioritize the best exploitation targets was presented with some important information:

Update on bonanza gold grades in Caren mine, have returned over 100 g/t Au at Fortuna – Merlin system in the Altos de Lipangue project, Chile.

Jan 27, 2016Of particular note are the extraordinary gold assays returned from the Merlin 1 vein, the first vein to be trenched, samples and assayed of five (5) parallel veins that outcrop to surface.

AURYN has focused its efforts on the Merlin Au-Cu±Ag high grade gold veins. Using a team of three (3) geologists and three (3) assistants, they have conducted geological mapping on the property on a 1:10,000 scale representing approximately 15% of the concessions. Over 1.5 km of trenching and over 200 samples of the 25 trenches and adits has been completed to expose the high grade gold in quartz veins that outcrop to surface. Gold assays have returned grades up to 66.5g/t gold with a weighted average of 26.9g/t gold on a diluted basis over widths of ~1.35 meter, adding high anomalies in Cu, Pb and Zn. These grades are better than expected. Currently the Merlin 2 vein is being mapped and trenches dug on 50 to 80 m intervals.

AURYN Mining Chile SpA Unveils Weighted Average of 26.9 g/t Gold in 200 Samples ~Bonanza Grades of up to 66.5 g/t Gold~ | AURYN Mining Corporation

I would strongly suggest that the Merlin Adits will be revisited after commissioning of the mill that incorporates a gravimetric circuit and will be used on appropriately concentrated ore by flotation, and possibly be followed up with CIL to avoid additional transportation costs. What would this gravimetric circuit recovery be expected to yield? I surmise the best recovery method using the Falcon system that is capable of increasing ore concentration 75-100X is now planning to be used in the FF circuit! (This is the system that allowed AURYN in that same June 2016 notification to state, “These results make us confident that we can produce a total of 5,000 troy ounces of gold before year-end 2016, and over 25,000 troy ounces in 2017.” )

Unfortunately, we all remember 2016 was also the year that the major share miscounts were discovered setting progress back far too many years… Is this why AURYN is now confident of attaining an initial listing on the OTCQB® tier as a goal? Is there anything that will ramp up value for AURYN’s shares quicker than production results and the unfolding of the economic value assigned to the exploitable deposits? Again, look at the June 16, 2016 notification. As the broad zone containing the veins are followed horizontally at the 1840-1900 meter above sea level, I would expect 5,000 troy ounces per quarter, or 25,000 ounces per year will be possible. Yes, my opinion starts with MC NOT being insane and having a meticulous plan that albeit slowly, is successfully being carried out. This is also why I remain confident staying the course will benefit shareholders as the anticipated secular gold market gets underway, and once started in earnest, will remain to bring value for a number of years.

EZ

3 Likes

IMO, unless Marizio gets serious about Auryn, nothing is going to happen of any significance. Auryn needs significant cash to begin development. What about selling off some of his bargain basement properties bought for pennies on the dollar. Then using the cash of whatever he can savage to develop Auryn??? At least there’s potential! Dreaming isn’t going to get us anywhere. I believe I made a similar comment last year after a friend (Pres. of ERO Copper) met with Marizio at the PDAC

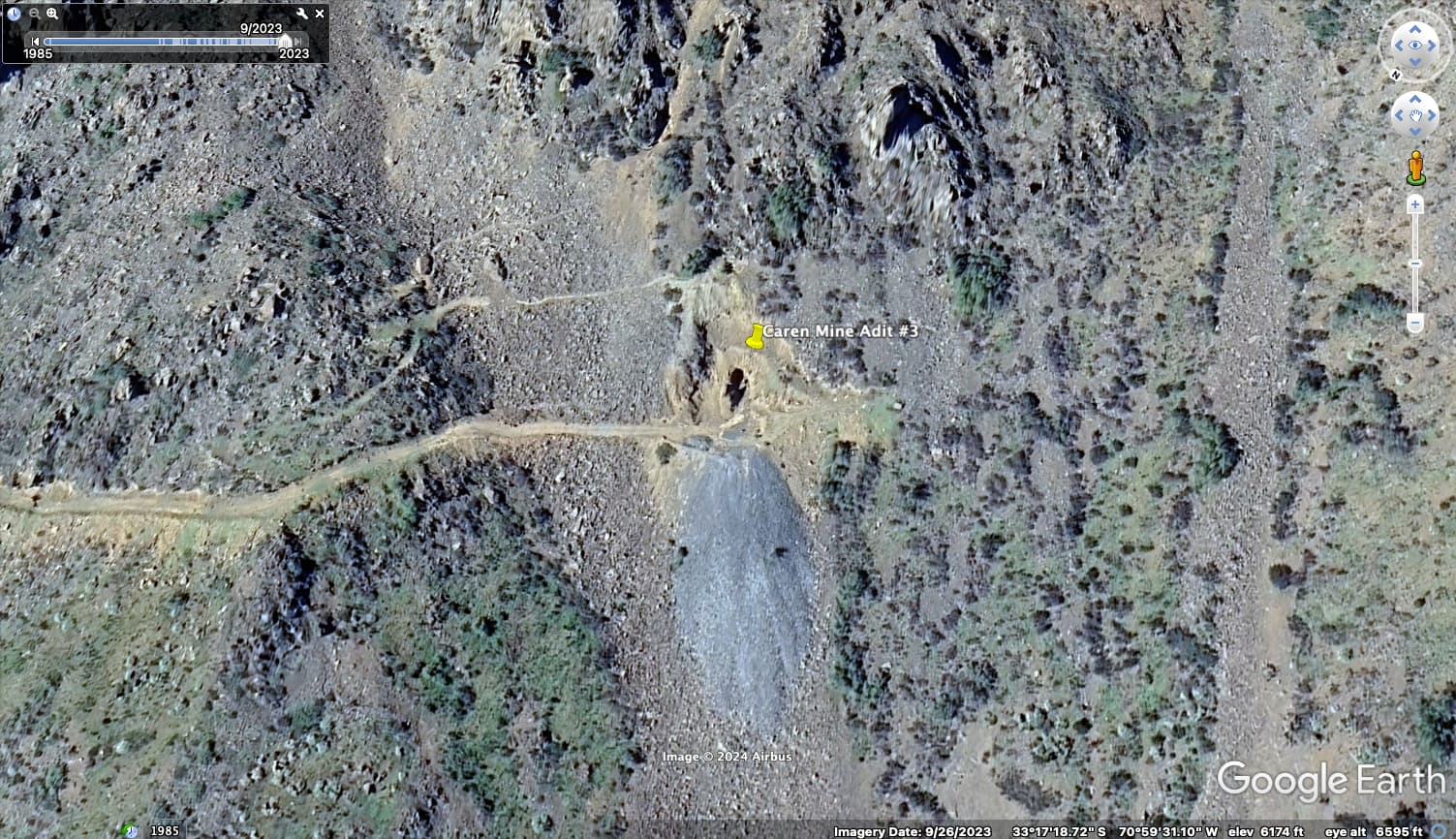

Google earth images from the Alto. I don’t know the date these are from, but downloaded recently. Anyone able to assess what the close-up shows?

TIA

The $5million plus he’s invested so far in the mountain without diluting us is just a joke, right Peter?

2 Likes

Hi Peter,

The 1st image looks like you were looking at the Caren Mine Adit # 3, shown below from September of last year - Note the orientation of N to show entrance more clearly :

The 2nd image below is the Antonino tunnel entrance and stockpiled ore, also from September of last year. Again, note the orientation of N:

Also note this 3rd image below from March of last year of the nearby camp infrastructure:

No telling how much things have progressed since these images taken last year.

EZ

3 Likes

Thanks, EZ. This post was from me, cabezon, don’t know how it linked to Peter. Thank you for putting it into context.

2 Likes

My bad, cabezon! Glad to have clarified the context a bit. I was in haste, and it annoyed me and just stuck in my craw where the post above yours said; “IMO, unless Marizio gets serious about Auryn, nothing is going to happen of any significance.” lol Maurizio is very serious, he knows what’s contained in the ADL, and is very methodically working with what he has to make it happen in a good way for all shareholders. In the meantime, I’m looking to have a payday day with the producing miners, like the top 5 miners comprising 44% of the GDX. The GDX currently has a 24,570,000 short position that should be cleared up in the next several months.

EZ

3 Likes

Gold ready to test 2200! Hey Jimmy, that stockpile is going more value by the day.

1 Like