Gold >3,800 this morning, fixing to take my shovel down to Cile myself and help out.

3 Likes

Im hoping a small initial dividend to get the MDMN debt paid off is in the plans.

Speaking of which, who are these MDMN creditors? How do we know they weren’t tied into the LP scam? Why should they even be paid back? Shouldn’t Greg Chapin pay them back out of his personal funds? He was completely negligent at best. Worst case, he was complicit in some way.

I was shocked to hear some of you were actually cordial to him at the last Vegas xxxxxxxxx

3 Likes

I’m not sure of the exact amount of MDMN’s debts, but yes a small dividend would take care of that and maybe trigger some other interesting events. Or, MDMN could sell some of those Auryn shares it holds to pay the debts off. I prefer the former, because I would like for MDMN to maximize the amount of Auryn shares that are distributed to MDMN shareholders. I recall MDMN’s debts non-interest bearing, so we’re not prejudiced waiting for the dividends to pay it off. If production is anything close to what management has been suggesting, this should be easy to accomplish.I think I recall Brecciaboy estimating (he was not sure of the numbers) that MDMN’s debt could be about $400k, plus maybe $200k of legal/administrative fees, total $600k. That may have changed, don’t know. I’m sure when the time comes MDMN will make proper disclosure.

Once Auryn starts production with some estimates on revenue they should file so mdmn can start trading on pinks again. This way us long shareholders can sell and get out of dodge because with out any doubt MDMN will fly once those positive numbers from Auryn come out. I am not here for the long haul been here done that! Time to sell make a profit hopefully , and move on.

3 Likes

Even more so to give loyal shareholders an opportunity to increase their exposure if they choose. They’ve handcuffed us, which is completely unfair.

Plus Baldy needs a re-entrance opportunity ![]()

![]()

![]()

![]()

![]()

A couple things about this AP article caught my eye. Can you spot them? ![]()

By MICHAEL LIEDTKE AND MICHELLE CHAPMAN, Associated Press

Electronic Arts, maker of video games like “Madden NFL,” “Battlefield,” and “The Sims,” is being acquired for $52.5 billion. The private equity firm Silver Lake Partners…and Affinity Partners will pay Electronic Arts’ stockholders $210 per share… If the transaction closes as anticipated…it will end Electronic Arts’ history as a publicly traded company that began with its shares ending its first day of trading at a split-adjusted 52 cents.

– madmen

1 Like

Gold pushing for 4000! Will it get there this week?

1 Like

Teacher, teacher, call on me, can I try?

The .52 per share is kind of close to what Auryn has been trading for, which could account for that dream I had the other night, but never mind about that.

And the way the construction looked like in those pictures MC gave us the other day kinda looked none at all familiar but like a real life video game, is that what you’re driving at?

3 Likes

Well, Mister B, here in my classroom, one correct answer does indeed earn you a passing grade.

The .52 share price in fact did catch my eye, as it seems AUMC has been flitting around near fifty cents for some years now. Well done.

The other correct answer would be the $210 per share payout. Because that is pretty close to exactly what I’m expecting from our MDMN/AUMC payout. No one here talks about the possibility of a short squeeze any more, but the fool in the market indeed lives on inside me. Plus, the decades-long dividend stream that we hear is coming our way could easily drive the value of this whole thing to incalculable heights. Who knows?

Before posting that news snippet, I edited it some, including a short mention about investors who held Electronic Arts at .52/share having waited 36 years for their $210 payout. That seemed way too depressing to leave in.

But thinking about it just now, with my morning ![]() , it occurs to me that there are probably one or two people here who were seduced by, and began investing in, the Mountain close to 36 years ago. I remember that when I stepped in here 14 years ago, there was talk of old-timers who’d already been in MDMN (or its predecessors) for nearly twenty years. That might have been the basis for a great extra-credit question, but alas, I can’t think of everything.

, it occurs to me that there are probably one or two people here who were seduced by, and began investing in, the Mountain close to 36 years ago. I remember that when I stepped in here 14 years ago, there was talk of old-timers who’d already been in MDMN (or its predecessors) for nearly twenty years. That might have been the basis for a great extra-credit question, but alas, I can’t think of everything.

Thanks for taking my test!

– madmen

6 Likes

At first I thought it had something to do with who acquired EA - mostly by Saudi Arabia with Kushner’s Affinity Partners. ![]() No passing grade for me.

No passing grade for me. ![]()

Your comparison is more interesting!

2 Likes

Nice Bid of 21,000 Shares at .80. Update around the corner.

2 Likes

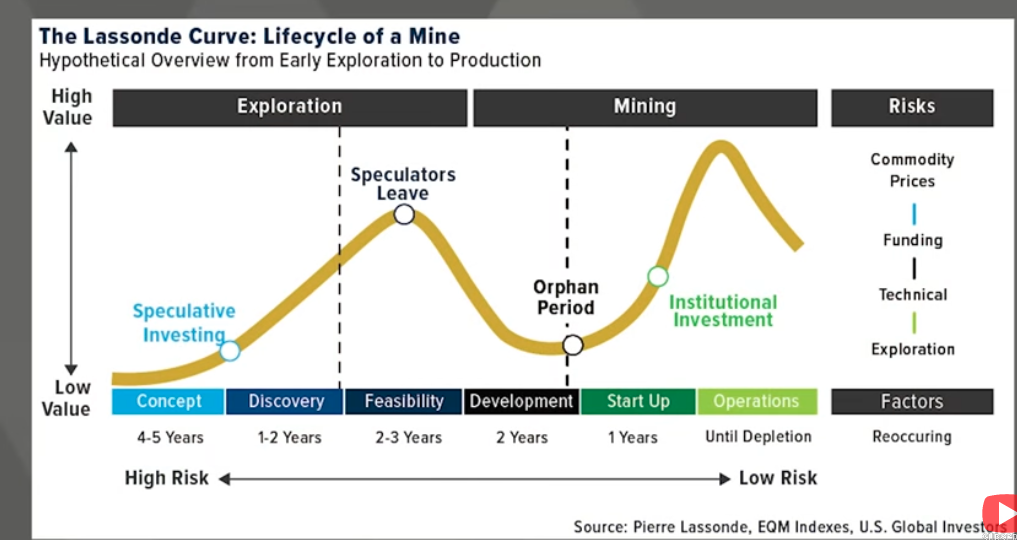

I FEEL THAT WE’RE IN A SECULAR BULL MARKET FOR GOLD THAT IS GOING TO LAST FOR A LONG TIME. AT THE CURRENT POINT IN THIS PARTICULAR CYCLE, I SEE THE PRICE OF GOLD AS PROVIDING A SUBSTANTIAL “TAILWIND” FOR TWO GROUPS OF MINERS. THERE ARE THE “CURRENT PRODUCERS” AND THERE ARE THE “ABOUT TO BECOME PRODUCERS” CATEGORIES.

IN THE CURRENT CYCLE, THE “PRODUCERS” I FOLLOW HAVE ALREADY GONE UP AN AVERAGE OF SOMEWHERE AROUND 150% TO 200%, AND IT’S BEEN A LOT OF FUN. THE “ABOUT TO BECOME PRODUCERS”, FOR THE MOST PART, HAVEN’T BEEN NOTICED YET. THEY ARE ALWAYS THE LAST TO “CATCH A BID” IN A BULL MARKET, BUT THEY HAVE THE MOST POTENTIAL EXPLOSIVITY OF THE ENTIRE GROUP.

THIS BEING THE LAST TO “CATCH A BID” IS BECAUSE THEY’RE HIDDEN AMONGST THE 3,000 OR SO OTHER JUNIOR EXPLORERS/DEVELOPERS, 95% OF WHICH ARE GOING NOWHERE AND WILL NEVER GO INTO PRODUCTION.

THE WAY I SEE IT, IN ORDER TO TAKE ADVANTAGE OF THE CURRENT “TAILWIND”, YOU EITHER HAVE A SAIL ON YOUR BOAT THAT IS CURRENTLY UP IN THE AIR CATCHING THIS WIND i.e. YOU’RE A “PRODUCER”, OR YOU ARE ABOUT TO HAVE A SAIL UP IN THE AIR THAT WILL CATCH THE WIND i.e. YOU’RE AN “ABOUT TO BECOME A PRODUCER”.

IN A BULL MARKET, WHEN THE WIND IS BLOWING YOU NEED TO CLEAR OFF YOUR DESKTOP AND ROLL UP YOUR SLEEVES AND DO SOME SERIOUS DUE DILIGENCE. WHY IS THIS? IT’S BECAUSE IN A BEAR MARKET, NO MATTER WHAT YOU DO IT’S TOUGH TO MAKE A BUCK NO MATTER HOW GOOD YOU ARE AT DOING DUE DILIGENCE.

IN REGARD TO AURYN/MEDINAH SPECIFICALLY:

IN TERMS OF THE “NET PRESENT VALUE” (NPV) OF THAT WHICH AURYN/MEDINAH OWNS, WHAT EXACTLY HAS CHANGED AT AURYN’S ADL MINING DISTRICT AS THE WIND STARTED BLOWING AND THE PRICE OF GOLD HAS RECENTLY INCREASED FROM $1,800 TO ABOUT $3,800 IN A LITTLE OVER 2 YEARS?

I should preface this with noting that the single most explosive event in the building of any mining company occurs when a junior mineral explorer/developer successfully defies the often-quoted 1-in-1,000 odds of getting a mineral prospect into production and accomplishes what is needed to make that transition into PRODUCTION especially if they have their own on-site ore processing facilities. It goes without saying that If a junior miner can time this monumental transition with the 3 metals being mined and sold all trading at or near their all-time high levels, then the level of explosivity is likely to be significantly augmented.

Medinah and Auryn shareholders all sense that it is a good thing that the 3 metals being mined and sold at the ADL are all trading at or near all-time highs, and without a doubt, it is a very good thing. But then they look at the share price performance of Auryn, and nothing ever seems to happen. The question arises as to what accounts for this DISCONNECT between significantly enhanced asset valuations and no market reaction?

I think that shareholders can partially remedy this DISCONNECT by at least taking comfort in the fact that behind the scenes, something difficult for investors to perceive has been breaking out to the upside in addition to the prices of the 3 metals being mined. What is breaking out to the upside is the NET PRESENT VALUE (NPV) of Auryn/Medinah’s mineral assets. This is tied to the close proximity of these assets generating significant levels of FREE CASH FLOW, and with only 70 million shares issued and outstanding, extremely high levels of FREE CASH FLOW PER SHARE (“FCFPS”). For me, Auryn is the prototypical “about to become a producer”, but at a VERY fortuitous time.

LEVERAGE TO THE PRICE OF GOLD

The first concept to keep in mind is that gold mining stocks have an enormous amount of LEVERAGE to the price of gold, silver, and copper. This LEVERAGE applies to levels of cash flow for those miners that are currently cash flowing but it also applies to “NET PRESENT VALUES” (“NPVs”) of the mineral assets, for those miners, like Auryn, that are on the brink of being able to generate significant cash flow. Parenthetically, I’ve NEVER witnessed a more opportune time for ANY junior miner to be transitioning into high-grade, near surface, gold, silver, and copper production, with their own on-site ore processing facilities, and with a tiny number of shares outstanding. As the saying goes “timing is everything”.

The financial metric that you want to concentrate on the most and is the best arbiter of value in this sector is EARNINGS PER SHARE (“EPS”) or FREE CASH FLOW PER SHARE (“FCFPS”). Of all of the financial metrics in use in this industry, EPS and FCFPS are the one most closely aligned with SHAREHOLDER REWARDS.

Compare the scenario described above to a miner working hard on exploration and development while blocking out ounces of MR/MR, but still remaining 4 or more years away from making a “positive production decision” and hopefully getting funded and into production. The ounces of MR/MR might be increasing nicely, but there is no TRANSMISSION MECHANISM yet available to DIRECTLY tap into the higher metals’ prices. When the prices of the metals are doing what they’re currently doing, the junior miners find themselves in a “RACE” to get into production and then in a subsequent “RACE” to aggressively ramp up production levels.

“NPVs” are estimated based on PROJECTED CASH FLOWS through time using a “discount factor” to account for the time value of money. For instance, $50 million that you will receive one year from today does NOT translate into $50 million worth of “value” today. The “discount factor” I usually use for modeling purposes is the 10-year Treasury yield plus 300 basis points.

Although we don’t have Auryn’s exact anticipated CASH FLOW numbers yet, we do have enough information to create some models that will lead us to a RANGE of potential CASH FLOW figures. At a minimum, the shareholders should at least recognize that the “NET PRESENT VALUE” of that which Auryn owns has gone up MARKEDLY since the POG has advanced from the $1,800 level to the $3,800 level. The TRANSMISSION MECHANISM needed to monetize this appreciation in NPV and convert it into shareholder profits appears to be close at hand.

The LEVERAGE to the POG works both ways, however. If the POG gets cut in half, then the damages can be irreparable, and a once “economic” deposit might no longer be “economic” at all. Likewise, if the POG were to double, then the increase in the estimated “NPV” of a mining district can be expected to be a lot more than twice the original value. Why is this? It has to do with incremental additions to metals prices tending to drop straight to the bottom line and things like AISCs, “cut-off grades”, and the “threshold” for ore to be deemed “economic”.

For Auryn, at the end of the day, a mineral deposit either meets the “threshold” for being “economic” at TODAY’S prices of gold, silver, and copper, or it doesn’t. It’s pretty much black or white. If a deposit is deemed to be “economic”, there is a vast array of just HOW “economic” it is, based primarily on the price of the metals being mined, the AISC, CASH FLOW generation, “mine life”, the “discount factor”, and how much LEVERAGE is present for that deposit or for that mining district.

100% OWNERSHIP AND EARLY PRODUCTION OPPORTUNITIES

Auryn has managed to maintain ownership of 100% of the entire ADL Mining District. There is currently present a vast array of potential, near term, “early production opportunities”. Management has already listed 8 of them that they are going after in the near term. The more “early production opportunities” a junior miner has, the greater is the LEVERAGE to the price of gold, silver, and copper.

With “disseminated” types of deposits (VMS, porphyry, sedimentary, SEDEX, disseminated sulfide, etc.) that will be open pitted, there are typically no “early production opportunities”. This is not the case when it comes to vein deposits, especially if there are multiple adits already in place from prior mining efforts.

If Auryn had, let’s say, 40 areas of interest at the ADL, and the price of gold was still trading at perhaps $900 per ounce. Maybe 2 of those 40 were “economic” at a POG of $900 per ounce because the ALL IN SUSTAINING COST was somewhere between, let’s say, $800 and $900 per ounce. If the POG more than quadrupled from that $900 level to the current $3,800 per ounce level, then perhaps all 40 potential production opportunities suddenly became “economic”. Each of the 40 will have its own incremental increase in its “NPV”.

In this example, although the POG approximately quadrupled, the number of currently “economic” potential production opportunities may have increased 20-fold after exceeding the appropriate “threshold”. In a scenario like this, the “NPV” of that mining district will have greatly appreciated even though the share price may not have reacted one iota as the price of gold was breaking out to the upside. Shareholders might sense that it’s a good thing that the POG is breaking out, but it’s in understanding what NPV is all about that makes it more tangible. This is known as “LEVERAGE” and is sometimes referred to as “OPTIONALITY”.

Compare the above situation to one in which the miner had modest land holdings in which there was only one or two potential production sites. This would greatly curtail any increases in the NPV. Recall how the former Head of Underground Operations at Yamana Gold’s (now Pan Am Silver’s) El Penon Mine cited how he felt that Auryn’s underground vein mining operations had the potential to be very similar to those at El Penon. At El Penon, where they, like Auryn, are also mining 7 Main Veins that compose a “Vein Set”, they are now mining from 38 different operational sites.

Ramping up production when mining a “Vein Set” is very straightforward and somewhat mechanical in nature. The heavy lifting was done by a combination of the work of the artisanal miners at the DL2 Vein as well as Medinah’s and Auryn’s combined efforts over the last 15 to 20 years.

When the POG goes up, some ore within a mineral deposit that was formerly “non-economic” because it didn’t meet the threshold for being “economic”, might all of a sudden have robust economics. This is going to extend the “mine life” of a deposit because it will take that much more time to mine those “extra” ounces of gold that just became “economic”. This will also increase the ounces of MR/MR contained within a deposit because it will also lower the “cut-off” grade which is the ore grade needed to achieve in order to make it “economic” and worth mining.

Suffice it to say that moderate increases in the POG can significantly enhance the “NPV” of a mining district and enormous increases in the POG, which we recently witnessed and continue to witness, can have a gigantic effect on the NPV of a mining district with many “potential operational sites”. All of this has to do with the THRESHOLDS to determine if a deposit is “economic” and how NET PRESENT VALUE is calculated.

An extended “mine life” translates into a longer period that the cash will be “flowing”. NPV calculations deal with CASH FLOW over time, but you need to keep in mind that CASH FLOW that is perhaps 15 to 20 years out, will need to be heavily discounted when calculating its NET PRESENT VALUE with the emphasis on “PRESENT”. When a miner like Auryn has its own on-site ore processing facility, an extended mine life represents the ability to keep that facility productive for an extended amount of time.

THERE IS A TREMENDOUS AMOUNT OF “LEVERAGE” ENCASED IN HAVING ONE’S OWN ON-SITE ORE PROCESSING FACILITY

If the prices of metals being processed is constant through time, then a froth flotation facility typically pays for itself in somewhere around 15 to 18-months. If the prices of the metals being processed at that plant are breaking out to the upside, then that timeframe will be greatly truncated.

Without one’s own on-site ore processing facility, a miner typically has to enter into a “tolling agreement” with a party that does own a mill and plant. These are very expensive because the owner of the plant that might be the only plant available within a certain distance from the mine, knows that the TRANSPORTATION COSTS for the miner to ship its ore a greater distance are going to be significant.

Auryn borrowed $4 million from an institutional funder to build its ore processing facility with a new crusher, ball mill, and froth flotation plant. If the life expectancy for the facility is 20-years and if the “mine life”, due to being extended by the increase in the metals prices, comes in at 20-years, then that $4 million plant could conceivably increase the profits from operations perhaps hundreds of millions of dollars over that extended mine life. This, once again, represents LEVERAGE and LEVERAGE gets magnified when the prices of the metals being mined are trading at or near all-time high levels. What Auryn did here is successfully LEVERAGE their balance sheet.

As Auryn will no doubt do everything in their power to rapidly ramp up their PRODUCTION RATE, this LEVERAGE gets magnified even more. As the PRODUCTION RATE increases, Auryn can increase the “nameplate throughput” of their froth flotation plant by adding new “cells”, “banks of cells”, and “flotation columns” in a modular fashion, further enhancing the LEVERAGE.

If the Pegaso Nero copper-moly porphyry prospect or the LDM stratabound copper-gold (skarn?) deposit prove to be “economic” then the ore from those sources can be fed into that same mill complex. The NPV of assets like those at the Pegaso Nero and/or the LDM deposit become greatly magnified when there is already an on-site fully owned ore processing facility present. The recent breakout in the prices of gold, silver, and copper also create LEVERAGE for the NPV of those assets.

If Auryn is able to drill a deep diamond drill hole at either the LDM and or Pegaso Nero prospects, and if that drill core shows “contiguity” of the ore to depth, then the NPV of those assets will grow parabolically.

The increases in the prices of the metals being mined act as a “tailwind” for Auryn. All of these varied sources of LEVERAGE act to increase the size of the sail capturing the tailwind. The incremental increases in the NPV of the overall Mining District are analogous to the forward progress being made by the sailboat itself. There is most certainly a SYNERGISTIC effect at play here as the different variables interplay with each other.

Don’t overlook the importance of Auryn’s new on-site geochemical assay lab. The recent increases in the price of gold has increased development activities like diamond drilling campaigns. Most of the players don’t have their own on-site assay labs. They bring in samples that get put into a quieu based on first in-first out. Processing times are now taking 4 to 6-weeks.

Auryn’s on-site geochemical assay lab will greatly streamline BOTH production and exploration activities. Auryn’s recently completed all-weather work camp that houses 50 workers will also greatly streamline both production and exploration activities. Any major or mid-tier miners wishing to come “kick the tires” might also find the new lab and work camp beneficial.

9 Likes

Just a reminder of another great post from BB explaining where we shareholders are at, and where this stock will be going … see the post from earlier this year. Since a picture is worth a thousand words, I’ll choose the former:

Get the picture! ![]() I know where we’ve been and where I’ll be going.

I know where we’ve been and where I’ll be going.

Patience…

EZ

4 Likes

Where does government stability fall in the equation? Venezuela was stable 20-25 years ago and was a rich country doing a vast amount of business with American companies and is now a dump in deep bankruptcy due to the instability of the government.

The government took over the oil in Venezuela -

I know most would probably say this could never happen to our gold, but what is the true situation with the government?

1 Like

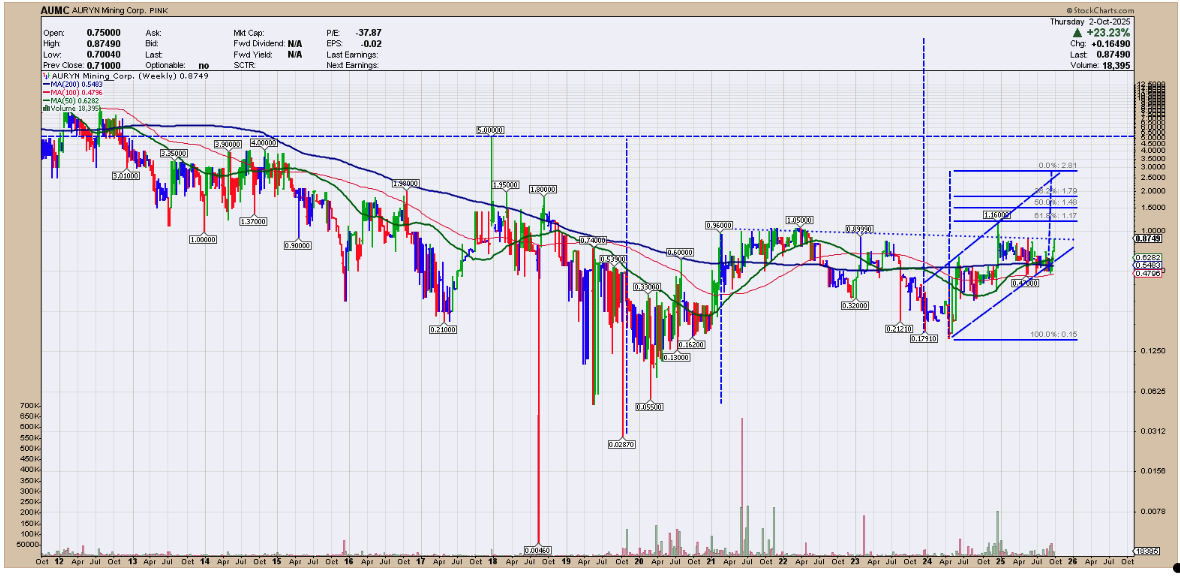

Well madmen, I’ve been working these past 13 or more years on this one particular puzzle that seems more like a test of endurance for me. Since I like “pictures” of a problem that can assist in finding a solution, be it a puzzle or a test, whatever the problem, I came up with sort of a cheat sheet that may work itself out sooner than later in a satisfactory way. This “roadmap chart” does seem to depict where I’ve been on this journey, but I may need some help in seeing where this particular journey may end, or is Auryn truly “The Neverending Story”?. Some stories seem to go on for 50 years or more! Could Auryn’s story be one of those?

The clues I have, as you can see, are drawn in with a few rather cryptic construction lines. What may one expect to see as time fills in the journey’s MA lines as time goes on? Whatever are those annoying dotted lines anyway? Could they be clues to unlocking this most amazing puzzle? Why does that one very long vertical dotted line that reaches skywards keep going right off the chart? Why does that green MA 50 line cross up over the MA 100 anyway? Does that mean anything? Will that darned red line ever come up through the blue? I’m sure some here could help in deciphering some of the clues, but alas, I suspect only time will complete this picture.

By the way, I’m still working on earning that passing grade. I’m sure this “roadmap chart” will complete its own answers in time without any further help from me. From what I can see, the clues do look quite promising.

EZ

3 Likes

Thank you, Easy - good, long-term perspective there.

Following is my short-term trading perspective - all lights are green right no …… for me.

There must be some “new” investors coming in - I wonder who they are - could it be people who were previously spooked for one reason or the other? I think we all know who I’m talking about - Bwahahahaha!

2 Likes

As far as I can find , the all time high was $1.05. Why does your chart indicate higher prices ? $4 …& up .

Chart actually says high was $1,571.87 in 1998 . Then $0.35 in 2003 !

https://www.marketwatch.com/investing/stock/AUMC

Rod,

Good Question! ![]() Chart adjusted for the 100 to 1 RS of CDCH shares converted to AUMC shares. The posted chart is for the CDCH shares, not MDMN, and would show $12.50 if time went back to the summer of 2012 and $27.00 if all the way back to Dec 2011. It was the price of CDCH shares that were directly converted over to AUMC shares. That is the answer to why that one vertical dashed line goes completely off the scale of the chart. For asking the relevant question of the day, the teacher tells me you passed the current quiz. I’m still searching for answers to the journey all shareholders are on. I’m sure you do know some mines of sufficiently large mineral deposits are mined for 50 or more years. It is size, grade and life of mine (LOM) which makes them much more valuable than smaller mines with LOM of only 7-8 years.

Chart adjusted for the 100 to 1 RS of CDCH shares converted to AUMC shares. The posted chart is for the CDCH shares, not MDMN, and would show $12.50 if time went back to the summer of 2012 and $27.00 if all the way back to Dec 2011. It was the price of CDCH shares that were directly converted over to AUMC shares. That is the answer to why that one vertical dashed line goes completely off the scale of the chart. For asking the relevant question of the day, the teacher tells me you passed the current quiz. I’m still searching for answers to the journey all shareholders are on. I’m sure you do know some mines of sufficiently large mineral deposits are mined for 50 or more years. It is size, grade and life of mine (LOM) which makes them much more valuable than smaller mines with LOM of only 7-8 years.

EZ

Mr B,

I’m surprised at you for showing short term trading levels on a mostly illiquid stock! Surely you realize the macro view chart that was posted is not for day traders, but for the serious investors still following this journey we seem to be on. The day trading charts will be relevant after 100K or 1M shares are traded daily. My opinion, and it’s only an opinion, is that the long term $5 MA line will be passed, and the $27 is only a fair value estimation of what CDCH deposits were worth when POG of gold was at it’s high in 2011. It is not inflation adjusted, yet!

Go ahead and chuckle. ![]() It’s good to laugh.

It’s good to laugh. ![]()

EZ

2 Likes