Thank you - I like this company, looks like it’s paying 1 cent per month dividend and when you divide that by the current share price of 1.69 you come out with about 7%? And that was over 2015 when the price of gold was suffering! Sounds pretty good to me - where are you going to get that in this market? When things settle down and the production has had a chance to sink in, our share price at very least will “adjust” to the dividend rate (as brecciaboy has stated).

Actually, I’m the only one talking about what’s in the contract. Show me the contract provision that talks about an escalating clause.

What I’m concerned about is the continued propagation of the BS lies I bought into at $2.00 a share and the same ones others here bought into at $0.17 cents a share at the AGM all talking about pie in the sky numbers.

The contract is published. If you and all the others want to speculate about how AMC is simply going to throw the contract out and give us more money or how MDMN is going to tell AMC that they’re not honoring the contract, be my guest.

If AMC wants early production on the MDMN owned claims (not Caren and Not Fortuna) or they want to put some of that 100 million into the ground instead of into MDMN coffers then they and MDMN are more than able to renegotiate the contract. Until then, I’ll stick with what’s real. The contract and AMC’s published news releases.

3 Likes

mdmnholder – click on the icon that has a thick horizontal line and an up arrow over it. It’s two to the right of the " (quote) icon.

EXACTLY! Thank you!

1 Like

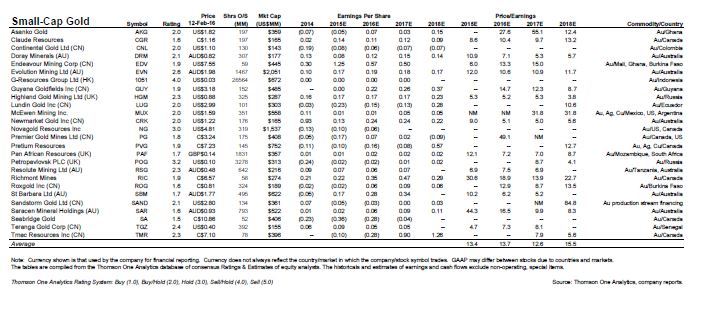

I get this from a friend of mine at Scarsdale Equity, he sends this out weekly, I am only posting what he terms the small cap gold companies, Sorry if is hard to read but a good guide for valuations

2 Likes

Seems like good information - but I can’t see it.

It looks like if you move your cursor over the pic, a bar pops and you can click the link, a separate window pops up with the pic and you download it to your computer. Then open in a photo program and enlarge

http://www.kitco.com/commentaries/2016-02-15/Metals-Mining-Analysts-Ratings-Estimates-Juniors.html

That’s Bill Matlack’s work . He posts it regularly on Kitco’s home page under “contributed commentaries”.

3 Likes

Yes, correct, he hosted an event for me. Haven’t talked to him for a while, but he sends out the Large Cap and Small Cap comps for gold, silver, base metals, Potash, etc.

2 Likes

Still comes up fuzzy and illegible - but the website brecciaboy suggests is easy to see. Thanks.

1 Like

For those that harp on about how it would be unfair and stupid for MDMN not to have an escalation or clawback in the contract. Think about it from AMC’s perspective. When the option is executed MDMN receives 15% of ALL of AURYN Mining. That includes Caren, LDM, Fortuna, and the other claim blocks that AMC owns.

The option agreement isn’t exercised yet. Do you know how much of that 124 g/t bonanza grade is MDMN’s? ZERO, NADA, ZILCH. Once the option is exercised, do you know how much we get? 15%.

How about LDM. Do you know how much is MDMN’s? 15% of Nuoco currently. Once the option is exercised we get an additional 15% participation through our ownership in AURYN.

Gee, what if they discover billions under that property or another porphyry system. It’s not fair that AURYN has to give us 15% of it. It wasn’t our property. (using the same logic applied against me)

Oh, what about Fortuna? MDMN owns nothing there currently.

Wait, there’s more. Do you that cu/mo porphyry? Guess what, MDMN’s claims on the ADL don’t cover the entire thing. But AMC has the other claim blocks that do — and post option MDMN will have 15% of it all.

So instead of thinking of me as stupid and saying MDMN wouldn’t be so dumb to write a contract without an escalation clause – just read the bloody contract and be thankful AURYN was persisent enough to consolidate all the claims and remove the blockage that has kept it from being developed for the last 20 years and that MDMN will participate in the entire ADL mining district and will do quite well from $0.02 where we are now!

If we end up getting $0.01 to $0.04 a share dividend every year that puts us at $0.10 to $0.40 a share stock price. Not bad when you can buy that at $0.02 today if you believe in the mountain.

Stick a fork in it. I’m done for the day. Out.

PS. In my opinion this is irrelevant anyway because MDMN and AMC will get together and figure out a way to exercise the option early under different terms. This will allow AMC to use some of their cash to go into early production on the CAREN and Fortuna claims and with MDMN participating immediately in the cash flow of that (something they cannot do without the option being exercised.)

9 Likes

No need to point this out but it might make sense to not accuse those who do understand how to value companies every time they come up with a number. You may not like discussion related to 10 or 20 cent price targets but those of us who like to have one foot in reality are weighing comparable valuations in the market along with the potential on the mountain (much of which is still be proven) to come up with reasonable expectations. Many people have lost more than they can afford by paying attention to the hyperboles offered by the same old posters claiming that the “sky is the limit” potential of the mountain while ignoring all of the basic laws of investing. Some of us are offering an alternate to these views so that they can better manage how they handle their exit or long-term goals here.

To make the claim that MDMN should or could be trading at 50 cents exceeds common sense and, to Wiz’s point, taints the discussion with uniformed “penny stock” like dialogue.

The contract says we will get 7 cents for 85% of the ADL. If we try to value MDMN at 50 cents or a $750M market cap for our remaining 15% that would mean they ADL/Mountain is worth $5B. If anybody bothered to spend five minutes understanding what it takes to support that type of market cap in this or any environment I can promise you they would be too embarrassed to post those numbers to our audience here.(but that would require understanding basic valuation metrics so the cycle will no doubt continue).

7 Likes

“Some of us are offering an alternate to these views so that they can better manage how they handle their exit or long-term goals here.”

I understand your point but that’s all it is your point of view just like analysts predict the market or stocks will go up based on fundamentals and then they find themselves scratching their head when they tank! When precious metals are in demand you just don’t know how the market is going to react.

Katanga is in the DRC, the ADL is 40 km from Santiago , big difference at first brush I think.

The only reason I posted the Scarsdale Equity Mining Company analysis was to give some, who desire, a chance to compare MDMN/AMC with other public comparables.

I did not intend, nor do I want to direct the board into discussion on various, non MDMN related, miining companies.

But in regards to Katanga, suggest looking at their website and look at their operations and financials, 2015 was a disaster, but for 2014, the company had over $1 billion in revenues and $135 million in net income. Not to mention they are a copper and cobalt company.

1 Like

Hi Wiz,

I don’t have a dog in this fight re: this topic but those 124 gpt numbers occurred in the south aiming adit at the Caren Mine. That adit will be under Medinah’s 100% owned Millalelfun northern property boundary at any time if it isn’t already there.

1 Like

BB, where are you getting your information from? Your intel is contradictory to the information that AMC published in their news release.

The Caren mine, through the acquisition of Minera Mantos Azules Chile, which in turn holds exploitation and environmental permitting to start early production of up to 5,000 t/month on the identified high grade veins that yield grades as high as 124 g/t (Update on bonanza gold grades in Caren mine, have returned over 100 g/t Au at Fortuna - Merlin system in the Altos de Lipangue project, Chile. - AURYN Mining Chile)

I believe that property is 100% AMC until an option is exercised.

1 Like

Hey brecciaboy, is it normal in mining deals that if a company allows a JV partner to come into the deal that one of the provisions is that if the JV partner discovers mineralization which extends to additional properties not already under control by the company say within 5 kilometers of the boundary then that additional property becomes part of the JV deal too? I thought I read where you said this before.

Wizard, BB is correct. Other than the first few meters beyond the entrance to that adit were samples was taken, it’s all Medinah’s.

1 Like