Who do you use?

Not all posters are your friends. In fact in a stock like this one where there is so much “stuff” on the line, some are very likely looking out for competitive adavatage for other than MDMN holders.

They will probably sound very reasonable in telling you why we are not really worth much.

2 Likes

Well I’m off to the Cook Islands for 2 weeks. If you’re living and breathing this stock, I suggest you re-evaluate your priorities. I plan on not even thinking about this stock while I’m gone, course having limited Wi-Fi helps

1 Like

“(which I seriously doubt, as AURYN will surely find a smarter path to

their goals than turn over that much cash to MDMN as we now know it).”

They may find a smarter path but the only way they get out of paying the $100million is to walk or hope they can convince the MDMN board that there is a more lucrative option they can offer. As of our last update it is reiterated that we are expecting the $100million no later than August 2017.

I would take 50 million for more % in Auryn

Now let’s get this done already!

1 Like

I say take the $100 million plus and pay a nice dividend. Then sit back and wait for Auryn to ramp up production so we can watch our share price go up and continue to collect timely dividends. We are so close now. Hold to the contract and see this thing through to the finish.

1 Like

I bet Auryn is feeling a little pressure on their side right now too. They will be struggling to gather up funds to build a mine; keep up with their committed exploration plan timeline; not give any ownership away; accumulate $100,000,000 from processed and paid production; all within 19 months. The clock’s ticking on their side too and I don’t think they can get that all done. If not the options for them are not pretty. If this option goes through expiration and they’ve now proved that their neighbor’s property has significant value it wouldn’t fit their plan to have someone else take out Medinah.

I think their best bet now is get all the cash together they can and pay the rest in stock. There’s probably a high stakes poker game being played out.

1 Like

Once cash lands, I think the metric you want to keep in mind is book value per share or BVPS. This is ASSETS minus LIABILITIES divided by the number of shares issued and outstanding. Assuming very little or no debt BVPS is basically ASSETS divided by I/O. For Medinah, ASSETS would represent cash and ownership of AMC. If Medinah has $100 million in the coffers then the CASH only part of BVPS would be 7.4 cents. If the share price only went to, let’s say, 3 cents with news like that then in one sense this would be wonderful news. HYPOTHETICALLY, Medinah could take $30 million of those $100 million and buy back and cancel 1 billion of its shares if they could buy them at 3-cents (obviously not likely). Now all of a sudden they’d have $70 million left and 350 million shares I/O or 20-cents per share in CASH not to mention the 15% stake in AMC.In a situation like Medinah’s with such an obvious DISCONNECT between its current market cap and the NPV of its assets, it’s not the amount of cash you have it’s how you can LEVER it in order to provide enhanced shareholder rewards.

When you have CASH in hand corrupt markets like ours don’t bother shareholders like they do now without cash in hand. The ability to provide shareholder rewards via share buy backs and dividends comes onto the table for the first time and shareholder rewards go up in parallel with the corruptness of your market. It’s nice to be able to place a bet on the fact that your market is corrupt because it’s a sure bet.

As far as how much cash Medinah might want to negotiate as a down payment, perhaps the tax consequences should help dictate the correct path. Medinah has a huge tax loss carry forward built up over the last 20 years. If Medinah could pull out maybe $50 million up front and pay zero taxes then that might be wiser than taking out $100 million up front and paying perhaps $20 million in taxes. Those “extra” AMC percentage points of AMC above the 15% current option level are going to grow in value at a much higher rate than cash will earn if Medinah stayed with the current option deal. Then you need to factor in the tax issues.

If the market valued Medinah at just its cash holdings and totally dismissed the value of perhaps 20 or 25 percentage ownership points in AMC then that puts us at about 3 cents per share. This would be a wonderful level at which to buy back and cancel tons of shares in order to drive up the BVPS. The ideal of course would be to get some up front cash NOW so that the share repurchases could start at today’s share price levels. Gaining access to even a moderate amount of cash the sooner the better is a total game changer in a deal like this.

2 Likes

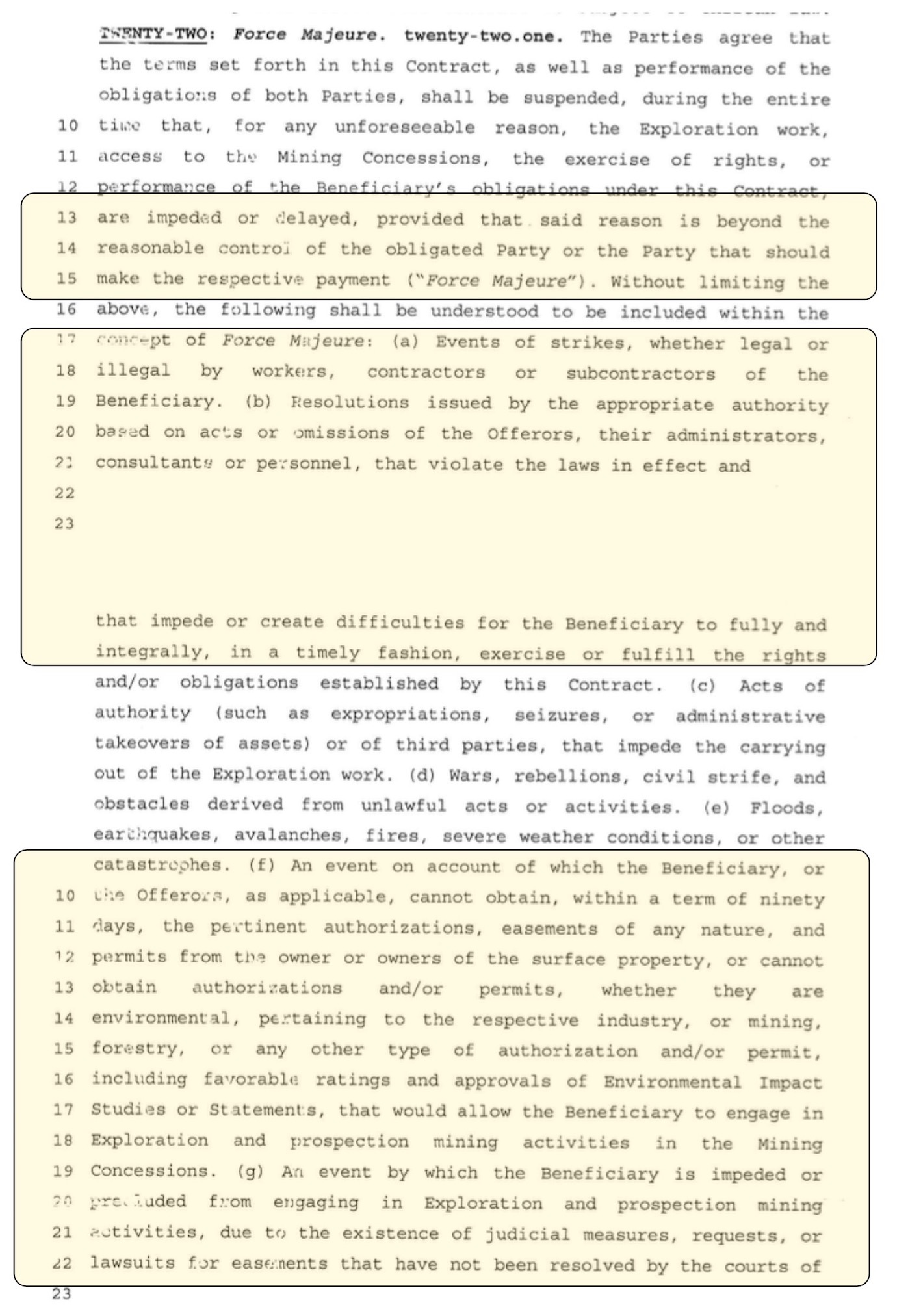

It’s simply not correct. Sorry. Read Section 22 of the contract. Also note 5.6.

I think the problem is we’ve been listening to the Vancouver Mill with respect to MDMN and not actually reading the contract and the financials.

1 Like

Frankly, this is absolutely the worst possible course of action MDMN could take, i.e. wait until AMC is ready to exercise the option. Have you read the full contract and the financials and the 15c211?

2 Likes

I’m not saying they may not be able to fulfill the work obligation under the terms of the contract. I think they will/have easily done that. I’m saying if they don’t have a pile of cash sitting around and they are dependent on mining their own claims to get a $100,000,000 for the option plus all the other funding needs they have they better get cracking. In fact I think it will be so hard and so risky they they will negotiate different terms now. That’s the pressure they are under.

I’m also assuming they would/will want all the claims.

1 Like

I am no lawyer but I will have to disagree with any implication that the term of the ADL Option agreement is subject to willy nilly change for the following reasons:

- Yes - Section 22 is a fairly typical Force Majeure which basically says: 'if Auryn is impeded by natural or human forces beyond their control from the “Exploration work, access to the mining concessions, the exercise of rights or the performance of the Beneficiary’s (chg - Auryn’s) obligations under this contract” then the timeline in the contract will be suspended.

Force Majeure is a legal term and sections like this are common in many contracts to mitigate legal ramifications of something like a natural disaster stopping a party from fulfilling their legal contractural duties.

In this case, also if there is no access allowed to Auryn to the claims to fulfill their obligations then a state of Force Majeure could be declared legally via lawyers and courts to suspend the time requirements of the contract. This has not been done as far as we know. Nor has anyone rumored any such a legal event occurring. This is not something Auryn could just wake up in the morning and say: 'I think I want more time, so I will declare Force Majeure nor could they just do so because they think Medinah was being slow on this or that task. It would have to be proven to be hindering Auryn from meeting their obligations under the contract.

The timeframe of the contract is thus not subject to willy nilly change due to declaration of Force Majeure

- Most importantly, Auryn has already met its one obligation under the contract spelled out in the first sections: spend $1M in exploration. They have no more obligations to fulfill.

Any further exploration say, on the P.Nero, is icing on the cake not fulfilling the contract obligations. They may be rather material to Auryn’s estimate of the value of the property though. So they could be rather unhappy about any situation that like those mentioned in the Force Majeure section, but it is not hindering Auryn from meeting their obligations. Of course, this could be a conclusion that Auryn’s lawyers would take issue with and want to fight and thus it could turn into a legal issue.

IMO if MDMN hinders Auryn in some way through incompetence or on purpose and they would risk pushing Auryn away or starting a legal battle and in either case they would risk self-destruction.

Otherwise, If MDMN due to incompetence or other reasons beyond their control would hinder Auryn’s hurried timeline, I would expect the two parties to work together to come up with some type of extension to the timeline. That could happen potentially.

But IMO, there’s no way the timeline in Auryn’s slide deck can / will be justified by Force Majeure or even MDMN getting in the way. The fact is the work being done is going way beyond the original $1M, or even the “up to $10M” phrase of the original contract and the original 3 years is just not enough time for everything Auryn wants to do to get done.

Aug 2017 is as certain as the ADL contract itself. The timeline is re-negotiable. MDMN could elect to give them 1 or 2 more years if they agree to some new set of work that must get done or some additional change in terms. Indeed this could be part of the current negotiations. This sort of alteration of agreements gets done all the time, as we just experienced with NUOCO/Auryn. And it could happen again.

As it stands, there is a clear conflict at this point in time between Auryn’s timeline in the slide deck and the ADL Option timeline. Either this forces Auryn to exercise by Aug 2017 with $100M and 15% equity, else there will be a renegotiation of terms perhaps including timeline, whether an immediate exercise for less cash and more equity, or a demand for the $100M and an extension of the timeframe.

2 Likes

Oh yes, I’ve read them. And I still say. We’ve waited this long so another year and a half is nothing. The more money Auryn spends on the ADL, the closer we get to the expiration date of the contract, the more leverage MDMN will have. Now if Auryn shows some hard asset proof that they are worth a great value, a value great enough to entice us to walk away from all that cash and own a percentage of their company. Then maybe we reconsider some things. But I have not seen Auryn show what they are worth to date and why we would want to own a piece of them as opposed to having some hard cold cash and the original % that is stipulated in the contract.

2 Likes

I’m sure they not only don’t want to lose the ADL, but I would bet they can’t afford to lose the ADL at this junction of the game.

I think Mike is right. Auryn/Medinah needs to wrap this up before production starts - otherwise it will be even messier to deal with changes going forward. IMO - If there’s going to be any kind of consensus it will happen within the next 30 days. As the option window closes there is probably less incentive to work out new terms.

1 Like

Please explain, they have enough near surface gold claims to keep them busy for years, IMO. Why is it important/imperative they need to have the ADL? TIA

The Boyz’s are going back to Chile after the Easter break…sometime in April.

I expect the Option agreement terms will be be modified during this trip…and Auryn will execute the Option agreement at the same time or shortly there after.

Production is still slated to begin in April albeit at a low level initially.

2 Likes

Mike, can you at least qualify your statement, saying “per Les”?

3 Likes

And Easter is only a week away (March 27) and no holidays in Chile or Peru in April… Hope they leave early April.

Mike you state “agreement terms will be modified” what do you mean by that? Could it be less money down more ownership in Auryn??hmmmm