Ha! No. Recall my premise that the Option Agreement is being vacated(along with auxiliary agreements) and a new agreement will be signed and immediately executed…ie basically Auryn fully acquires the Alto at signing.

1 Like

Of course there will be cash calls on the partners. Doh! L&G, your expectations are completely unrealistic. No company could survive giving 15%+ to one partner (MDMN), 5% to another partner (CDCH), and another 5% to another (NUOCO) – and having none of those partners contributing to the development.

Per a friend who spoke with LP … If the above is how it ends up (already 2/3 of the way there and just waiting on MDMN.) The expectation is that Masglas will finance the development with favorable terms for AMC & partners with the debt being repaid from future production (or sale of porphyry) as opposed to the sale of shares i.e. dilution.

2 Likes

Lean maybe Auryn has structured the new deal for us to gain more percentage. If this mountain holds what it holds I’m good with that. Auryn needs Medinah Medinah needs Auryn. Let’s get this done already!

1 Like

Lean - does Auryn bring any properties to put in with ours - or are we merely getting back a minority percentage of what we owned 100% of previously?

I am not sure the genisis of original option agreement, which IMO, was an unrealistic dollar amount to begin with, but it could have been nothing more than “saving face” move on MDMN’s part. Having said that, not sure why AMC which is reputable with go along with the charade.

But if the ADL contract is renogotiated with no upfront cash, this is looking more like a standard “farm in” agreement where a company (MDMN) has attractive claims but no money or experience, and MDMN allows AMC the right to explore, develop etc. the claims in return for receiving a percentage ownership. The ownership creeps up based on the amount of exploration dollars spent. The end game is usually the company spending the money ends up with 80-85% ownership.

2 Likes

Interesting read

The company has the cash to put this plan into action. The company closed out fiscal 2015 with $7.5 billion in the bank (its fiscal year end is March 31, almost a year ago), a marked contrast with the debt-burdened balance sheets of most North American mining majors.

That company is Viscount Mining Corp. (VML:TSX.V). Viscount’s flagship asset is the Cherry Creek project in Nevada. And last February Sumitomo, through its subsidiary Summit Mining, signed on to earn 75% ownership by spending $10 million on the project over eight years, in addition to producing a bankable feasibility study at an estimated cost of between $30 million and $40 million.

Actually, yes, Doc and others have been completely unrealistic if they ever thought we would get a 15% FCI on this project. I was quite naive to buy into that at the time as well. Please show me some comps where companies like MDMN are getting 15% FCIs? I’ll wait.

Also, I think Baldy is completely wrong regarding his idea of waiting for the $100M. I could go into a detailed analysis, but I’ll try to keep it short.

Baldy knows and has expressed quite often that what we own on the ADL in its current state of development is NOT worth $100M in today’s market. Of course, AMC knows that as well and they won’t exercise the option until it’s worth more than $100M to them. Meanwhile MDMN is on the hook for costs and continues to dilute all of us while we wait. If / when AMC gets to the point that the ADL claims that MDMN owns are worth more than $100M to them, they’ll exercise the option. Meanwhile, the $100M continues to decrease in value to you and me through dilution. We are the ones who suffer by waiting.

If the MDMN claims prove up well enough to exercise the option then in hindsight we know that we would have been better off with a larger percentage of the entire pie (including Caren, Fortuna, and LDM) than we would be with $100M and 15%.

If the MDMN claims (for whatever reason) do not prove up well enough to be worth $100M to AMC, then they will not exercise the option. In that case the only thing we’d have is the dilution it took to get to that point and the Merlin claims which we’d have to sell off to AMC or someone else.

When those are the two options, it’s a no-brainer for me to close the deal now rather than risk the remote possibility of significant dilution and a bust on the Pegaso Nero.

In other words the choices are:

a) A nice large profitable percentage in the Caren / Fortuna / Merlin / LDM claims today, and the same percentage in the mega porphyry if it proves up.

b) The option for 15% of the Caren / Fortuna / Merlin / LDM claims and $100 million after whatever dilution we suffer occurs while AMC seeks to verify that the mega porphyry is indeed worth over $100 million to them. This choice also means if for some reason it doesn’t prove up to be worth $100 million to AMC we are left with 0% of the Caren / Fortuna and own the Merlin claims which we will then have to figure out what to do with.

Given those two choices, I’ll take “a” all day long. I lock in a win and have a larger percentage upside! I eliminate the downside risk.

2 Likes

Yes, they do but many conveniently ignore that because it doesn’t fit their view. The Caren (the only one currently permitted and showing bonanza grades is theirs.) Of course, from MDMN’s perspective the Fortuna is theirs as well. Also if you look at the claims map, you’ll see plenty of property to the east and south that includes what they think is part of the porphyry is AMC’s alone as well.

This is not hard to understand. The problem is for too long we’ve been sold pie-in-the-sky talk about 15% fci’s and billions and billions of $$$$'s while we were diluted and nothing ever got done. It pisses me off how stupid I was to listen to that bunk.

This post right here is reality …

4 Likes

What ever happen to all the tailing from LDM and I thought that was permitted as well? I am assuming since we did not get our FCI from LDM that the ore is still stock piled waiting to go to the mill!

You eliminate the downside risk? We are trading under 2 cents. The downside risk is very definable. I’d suggest you don’t get too cozy with the boys at AMC. Their opinions are based solely on their self interest (as they should be). But don’t think, for a minute, that they aren’t expecting you to come on this board and start talking up the merits of a renegotiated deal. We all know they follow these boards and I’m guessing they are over the moon that a consensus is building that a larger percentage in AMC is acceptable im lieu of cash.

No, I don’t think the ADL is worth $100M but that’s the number we got in the contract. AMC’s valuation of the ADL won’t be determined solely by drills in the ground but rather the strategic proximity of the claims. Without the ADL, AMC would be limited on several levels vs if they owned the entire mountain.

I don’t mind a little dilution (and its little compared to the last decade) to allow us a year or so to let the contract play out.

If you think that getting 25% with no cash vs 15% with $100M is sensible, you need to be comfortable valuing AMC at $1B. I guess CDCH should be trading at 20 cents. (Please make that happen)

I think there is way more risk in agreeing to rework the contract at this stage. Yes, maybe they walk from the deal but I find that outcome highly unlikely. If MDMN stays firm the more likely scenario is a TO or a “better” reworking of the deal as we get closer to the option expiration. IMO

4 Likes

Baldy, while your thoughts are rational, flip the coin. If AMC walks, they still have enough claims to make substantial money. Where does that leave MDMN/ADL? Partner 4,5… with some of the near term production claims owned by AMC and all exploration data becoming unqualified with the need to redo the work to be used for Technical Report/43-101/JORC. As importantly, the ADL primary jewel becomes copper/moly, which is the domain for the big boys, which with the exception of a few (Sumitomo as I posted today) have little cash and even a lower threshold for greenfield projects of this scope.

2 Likes

Perhaps you don’t understand how boards work? The very purpose is to create a diverse group with a blend of differing expertise, with the hope of a achieving “the whole is greater than the sum of the parts” type of thing in order to provide strategic vision and professional execution.

And wasn’t Kirkland the one who warned us the Auryn deal was perhaps “not in the best interests of stockholders” or something to that effect. Remind me what has happened to our market capitalization since we made the deal with Auryn?

I don’t have any idea where your going regarding the casino angle, doesn’t Chapin have ties to that industry as well?

Did Kirkland personally explain to you why he left, or did this story come from Leslie and the usual, always reliable, communication channels?

3 Likes

Disagree. You know and I know that the ADL isn’t worth $100 million. AMC knows it too. They also know it’s not going anywhere. There is no way they exercise it for $100 million. They’ll just move forward with what they have now and let MDMN hang in the wind. Nobody is going to come in and swoop us up until the end of the option agreement.

If it isn’t reworked the likely scenario is the option agreement stays as is. AMC proves up the ‘P’ to the level they feel it is worth far more than their $100M, then they TO. Under that scenario, if it doesn’t prove up to be worth more than $100M to them (which is a real possibility for any number of reasons) they simply don’t exercise. Then where are we? No cash, more dilution.

So we’ve covered the possibilities. I’m not willing to risk hanging out with “option, option, option” for the next 18+ months. I’d rather have “done, done, done” for real and a larger piece of the pie. That’s just me.

2 Likes

As long as it’s not a Chapin’s “done, done, done”, I’ll hang with you…

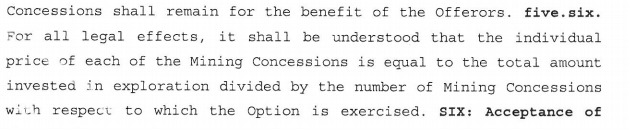

While I’m posting . . . does anyone want to offer an explanation / interpretation of this clause from the contract?

1 Like

The question comes down to are we still dealing with the original people from the original deal. I find it very interesting that the officers of Auryn are no longer posted on their website. This raises the question on whether something has changed in the back ground. In other words are the Letts family with their billions still involved or is Auryn going a different route after JJ refused to sell his shares. Just something to think about!

5 Likes