Don’t know. One could guess that with the fall of commodity prices, that project got scrapped. I do know that Auryn has at least committed monies for a new processing facility of some sort of their own. I think that with an agreement likely imminent on the sale of the Alto, Auryn will release monies for a much higher level of activity on the mountain such as a MASSIVE drill program on the new porphyry target, building of the new mill and continued construction of a core shed large enough to handle the crazy amounts of drill core that will be generated.

3 Likes

We went to 16 cents on a handshake from the Swedish sensation. Now we’re hooked up with a real outfit. We will do very well IMO.

Just going back in time, looks like Til Til is substantially closer than Enami and comes with less transporation issues. I shake my head with the info put out in this update, but good info on milling.

Yes it is amazing how quickly we forget statements like this and whatever happen to the ore?

From what I’ve been told I think it’s fair to say that a number of the statements made by Juan in shareholder updates may be considered factually inaccurate. :-/

That said, my understanding is AMC is going all out in their efforts to handle the milling requirements on their own.

I have much more confidence in the information obtained from south of the border than that which is passed on from north of the border.

5 Likes

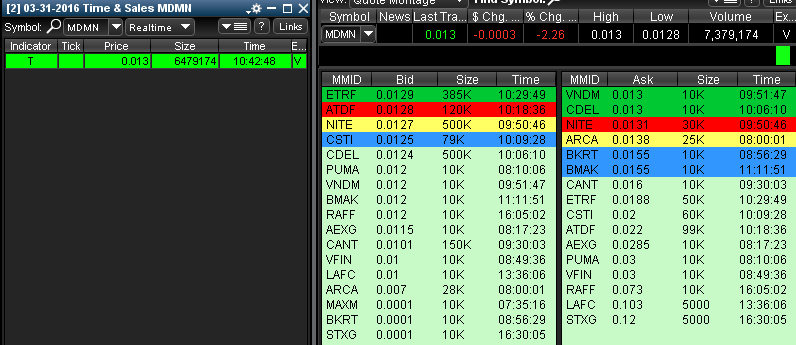

And we continue to have a thorn in our foot seller!

Are we really at 7 million traded?

Wow and they don’t move the ASK

Some one getting in on the cheap. May be news is close IMOH

The mm turds take turns on the ask now its VNDM for a couple of weeks on endless amount going through the ask and not budging before VNDM it was BMAK.

I would love to see MDMN get some cash out of the deal and issue a dividend even if its .005/share. These basturds would have to cover their azzez.

5 Likes

Unbelievable we continue to have a seller, just unbelievable. It HAS to be somebody who has NO idea as to the value of this mountain and the good things happening. Personally, I’d like to see our guys get say $30 Million out of the option exercise (with an increased percentage in Auryn of course) - then they could use that money to buy back some shares (say 300 million shares at up to 3 cents per share, $9 Million) and pay a one cent dividend ($13.5 Million), with more left over to satisfy obligations and operating cash going forward. Attack these idiots on multiple fronts.

7 Likes

How can someone with that many shares NOT be in the loop. That is the part that has NEVER made any sense to me, and is still concerning. And no, I do not have an explanation as well. I just don’t like it…

1 Like

I have an order in and it does not show on the bid list?

Here’s a very rough draft of a paper I’m working on that addresses some of your thoughts.

ONCE ANY UP FRONT CASH PAYMENT IS MADE OR CASH FLOW FROM PRODUCTION COMMENCES, CONCENTRATE ON TOTAL SHAREHOLDER REWARDS WHETHER THEY BE FROM SHARE PRICE APPRECIATION OR FROM CASH DIVIDEND DISTRIBUTIONS. THE QUESTION ARISES: IS THERE OR IS THERE NOT A CLEAR PATHWAY ESTABLISHED FOR MEDINAH INVOLVING PERHAPS SEVERAL DECADES WORTH OF LIKELY TO BE PROGRESSIVELY LARGER CASH DIVIDEND DISTRIBUTIONS?

From one point of view, one of the driving forces behind a deal between AMC and Medinah being done NOW rather than 18 months from NOW (upon option expiry) is hopefully Medinah’s gaining access to QUICKER CASH in order to buy back and cancel a significant amount of shares at TODAY’S ridiculous prices. This will then “prime the pump” for the potential for relatively larger dividends for perhaps 30 years (projected mine life?) due to lesser shares being issued and outstanding post-cancellation of those repurchased shares.

There are two components here. Management needs cash and needs to deploy that cash at the same time that the share price is in the toilet i.e. NOW. We do not want management buying back and cancelling shares when AMC is producing from 5 different sites on the mountain, dividends are flying out the windows, pit optimization studies are being done and the stock is trading much higher than it is NOW.

Note the relative importance and necessity of a share repurchase/cancellation program for a company like Medinah if they were dealing with a mine life of 30 days versus perhaps 30 years when it comes to the need to tighten up the number of shares issued and outstanding immediately upon gaining access to cash. A one time concentrated tightening up of the number of shares I/O can “supercharge” shareholder rewards for a very long time into the future in a scenario like this dealing with an extended mine life and the caliber of the mining professionals Medinah is working with i.e. Alegria, Cordova, Bocanegra, Bent, etc.

It’s the current paltry $17 million market cap that says DO THE DEAL NOW. If we were to land, let’s say, $25 million up front in a modified ADL purchase agreement deal, that money has the same share repurchasing power as $100 million would if the share price was just 5-cents like it was not that long ago. In a scenario like this with this large of a DISCONNECT present between Medinah’s market cap and the NPV of its assets you HAVE TO do an aggressive share repurchase and LEVER the DISCONNECT. It really is FREE MONEY.

WE NEED A “TRANSACTION” TO CONFIRM THE DIAGNOSIS OF A MASSIVE DISCONNECT

IT’S THE TERMS OF A TRANSACTION ENTERED INTO BETWEEN TWO WILLING PARTIES WITH (temporarily) COMPETING INTERESTS THAT CONFIRMS TO THE WORLD THE EXISTENCE OF THE DISCONNECT. A company with a $17 million market cap is not supposed to be landing perhaps $25 million in cash and a big percentage of a consolidated mining district with the promise this one is showing. That just doesn’t happen in an “efficient market”. But until a TRANSACTION is done you’re left with only an OPTION that the public might view as something that may or may not get exercised. It’s time to remove that UNCERTAINTY. We nutcases that follow THEMININGPLAY religiously on a daily basis sense that a deal will indeed be done but we have to realize that we’re the exception and not the rule from a behavioral point of view.

Disproportionately large dividends post-share repurchase programs (one form of shareholder reward), in turn, can and will drive the share price up (another form of shareholder reward). There are synergies present here. Opportunists, even if they’re just “dividend flippers”, will be attracted prior to the dividend record date to generous (on a percentage of share price basis) dividends. The share price will seek a level at which the dividends are just generous and not insanely generous. If a new investor were to opt to “flip” the dividend and sell shortly after the dividend “Ex-date” then that would be wonderful for those of us with dividend cash in hand wishing to buy more shares (at the corporation’s expense) in order to access the synergies involving exposing progressively larger shareholdings to progressively larger cash dividends throughout time.

Companies with share prices in the toilet are not supposed to be in a position to potentially distribute 30 or so years of generous dividends. DISCONNECTS like these set up arbitrage opportunities but only for those aware of the DISCONNECT. If the share price continues to refuse to budge, that’s great if management has cash in hand. With share repurchases followed by demands for delivery followed by cancellations, each shareholder will end up owning a larger percentage of the company and a larger share of any profits to be distributed out as dividends in the future.

A corporation with a current 10-to-1 DISCONNECT could theoretically buy back and cancel 50% of its shares by spending only 5% of its net assets. Possessing powerful leverage like that borders on insanity. In a scenario like this, something has got to give; either the share price takes off or shareholders get rewarded via these synergies regarding dividends. Both are forms of SHAREHOLDER REWARDS. The market will dictate the path of least resistance for shareholders to be rewarded.

In scenarios like Medinah finds itself in, cash dividends can be looked upon as THE GREAT EQUALIZER. Why? It’s partly because those carrying legitimate or “naked” short positions are forced by law to MATCH all cash dividends while they retain a short position. Not many junior mineral explorers are afforded a clear pathway to distribute a long series of cash dividends. But when found in that position and your market cap is ridiculously low then you ABSOLUTELY HAVE TO aggressively buy back and cancel shares when the opportunity presents itself and the cash is there.

The potential for a very long series of cash dividend distributions forms what amounts to a SAFETY NET in regards to “shareholder rewards” and represents the worst case scenario for shareholders IF the share price continues to refuse to budge. Management simply shifts gears on their methodology of providing SHAREHOLDER REWARDS. The goal of management should be to GUARANTEE shareholder rewards proportionate to the risks taken and the success of the company. Whether these shareholder rewards come in the form of share price appreciation or a generous flow of cash dividends shouldn’t make that much of a difference to shareholders. You can’t rely on corrupt markets alone to provide shareholder rewards proportionate to the risks taken and the success achieved. The problem is that UNTIL you gain access to up front cash and/or a stream of cash dividend income you have no option but to rely on shareholder rewards coming through corrupt markets.

KEY CONCEPTS

- To me, it’s critical to stop thinking solely in terms of share price and more on a pathway being established to GUARANTEED SHAREHOLDER REWARDS incorporating cash dividends. A deal with AMC NOW might provide that pathway. The mountain itself has spoken very clearly.

- The absolute best time to execute a deal like this, especially if up front cash is included, is when your share price is in the toilet. It’s the FLOAT TIGHTENING POWER of the cash that is critical and not just the nominal amount of cash.

- It takes a TRANSACTION preferably involving up front cash to confirm the existence of a DISCONNECT especially if the amount of the cash alone exceeds your existing market cap. Ownership interests in mining projects are notoriously difficult to value, cash is not. To mainstream investors unaware of the nuances of this particular deal options represent UNCERTAINTY because some are not exercised.

- The POWER associated with initial share repurchases is proportionate to how large the disparity between the current market cap and the NPV of your assets is. The projected mine life is also critical because that tightening of the float is going to last for the duration of the dividend flow which is tied to mine life.

- The generosity of cash dividends should drive the share price up. If it doesn’t then shareholders could simply deploy the cash they receive via the dividends back into the market and buy ridiculously cheap shares so that they can expose that many more shares to the future flow of cash dividends. In a sense the SHAREHOLDER REWARDS become essentially “GUARANTEED” because the generosity of the cash dividends on a percentage of share price basis (a form of shareholder reward) is inversely related to the share price which is the other mode to provide shareholder rewards.

- If the cash dividends become progressively larger over time (as is the norm for a mining project like this)then a very powerful positive feedback cycle can be established via exposing PROGRESSIVELY LARGER SHAREHOLDINGS to PROGRESSIVELY LARGER CASH DIVIDENDS. This sets up more of a geometric progression for SHAREHOLDER REWARDS than an arithmetic progression. Think of it as compound interest on steroids.

- If there is a significant short position in existence, no short seller in their right mind is going to elect to MATCH 30 years of progressively larger cash dividends.

- When management has cash in hand and is buying back shares, corrupt markets actually benefit the corporation as management could buy back and cancel larger amounts of shares given a finite amount of cash allocated to that purpose.

- The concept of GUARANTEED SHAREHOLDER REWARDS is the key. The pathway to those rewards will be dictated by the market.

- The ROCKS themselves, the infrastructure present, the prices of the metals contained therein and the skills of the miners will determine the amount of the cash flow available for cash dividend distributions.

- There are buyers out there that purchase predictable “streams of cash flow” generated by capable mining professionals. Selling a portion of Medinah’s share of cash flow would also be a possibility. Periodically receiving bids on these percentage points from outside sources will help Medinah management calculate the NPV of their assets and therefore gauge the size of any DISCONNECT.

- As more of the areas on the mountain receive their production permitting and as the permitted production allowances go up over time for any one particular group of concessions the NPV of the percentage ownership points in AMC will likely grow accordingly should Medinah want to sell them. Medinah should be constantly in touch with AMC asking them what AMC might offer them for Medinah’s AMC stake so that Medinah can constantly gauge the NPV of their assets. The cash flow and dividend size will also grow accordingly should Medinah opt NOT to sell some of their AMC percentage points. The biggest “ramping up” of production might be subsequent to an open pitting of either the early production opportunities or the deeper porphyry assets.

- Despite generous cash dividend distributions, IF the market should continue to undervalue Medinah shares management could simply sell a few percentage points in AMC and take that cash (in addition to its portion of the cash flow)and go back into the market and buy and cancel that many more ridiculously priced shares. The value of the percentage points in AMC would therefore be set by industry standards not corrupt markets. To facilitate share repurchases Medinah might even consider swapping some of their AMC percentage ownership points for the Medinah shares held by AMC.

- If Medinah were to sell perhaps one fifth of their AMC equity interest and take in cash equalling their market cap then once again a massive DISCONNECT would be revealed to the investment world. This would represent a TRANSACTION which would serve as a valuation BENCHMARK.

- The basic philosophy here is let AMC and their team mine the ore while Medinah management shuts down the monthly corporate burn rate to a trickle and concentrates on mining the DISCONNECT. Mining the DISCONNECT does not involve any of the risks associated with mining the ore. It’s a “riskless transaction”.

- The magic of dividends has partly to do with the fact that the last vestige of integrity our OTC markets have is that short sellers must MATCH all cash dividends made while they hold a short position. This is in addition to cash dividends serving as the only reliable means to GUARANTEE SHAREHOLDER REWARDS within corrupt markets.

MORE ABOUT CASH DIVIDENDS IN THESE OTC MARKETS

Shareholders owning shares on a “dividend record date” (DRD) are entitled to cash dividends. Short sellers holding short positions on the dividend record date must either cover their short position prior to the dividend record date or “MATCH IN LIKE KIND AND QUANTITY” the cash dividend and provide them to the buyers of the shares they sold short.

In the 30-day period prior to the DRD for a generous cash dividend, opportunists might be likely to buy shares in order to cash in on the generous dividend even if they plan to sell those shares immediately after the “Ex-dividend date” and “flip” the dividend. Unfortunately for short sellers, if they want to cover their short position prior to the DRD they are going to have to buy shares amidst the upward pressure in share prices caused by the buying by opportunists whether they be “flippers” or long term investors. Not many new short sellers are going to short sell into those buy orders because they will immediately be on the hook to match those dividends. Not many shareholders are likely to sell their shares prior to a generous cash dividend DRD either. You’re left with a perhaps 30-day time period in which buying will be exaggerated and selling, whether short selling by new short sellers or those with preexisting short positions or long selling, will be minimized. If Medinah’s nonstop sellers are ex-insiders or abusive naked short sellers both parties would think twice about selling prior to a DRD for a generous cash dividend.

This 30 or so day imbalance involving buy orders dwarfing sell orders would drive share prices upwards which in turn would decrease the generosity of the cash dividend on a percentage of share price basis. If the cash dividend in question is the first of what is expected to be a long series of what are anticipated to be PROGRESSIVELY LARGER CASH DIVIDENDS (PLCDs) then the opportunistic buying before the first DRD might become intense as investors might want larger long positions to ride that wave of synergies.

People carrying large short positions into a DRD thought to be the first of many dividends in series are put into a bit of a bind. They certainly don’t want to MATCH a long series of generous cash dividends. But they also don’t want to cover their large short position amidst a bunch of opportunistic buying within a confined period of time. Short covering during this 30-day period may add to any explosivity. A similar phenomenon might occur in the 30-day timeframe before ALL of the upcoming DRDs except for the fact that in the case of all dividends after the initial one the shareholders will have a lot of cash in their jeans at the time from the prior cash dividend distribution which might add even more to the explosivity. Pre-existing shareholders already know the story and don’t need to be educated as to Medinah’s assets.

CASH DIVIDENDS ARE ALMOST “MAGICAL” FOR COMPANIES LIKE MEDINAH

Cash dividends are very honest. If you don’t have corporate success you’re not going to be in a position to distribute any. In corrupt markets like Medinah’s they are a godsend. With the ability to declare and distribute cash dividends, management can now distribute shareholder rewards that can’t be manipulated. In fact, the generosity of cash dividends can help confirm prior manipulation of share prices resulting in these DISCONNECTS. Periodic cash dividends can serve to help “purge” a corporation’s share structure of the readily sellable “security entitlements” that result from abusive naked short selling.

A MATH EXAMPLE

Medinah is trading at 1.25-cents. A shareholder owns 1 million Medinah shares. Medinah declares and distributes a 1-cent cash dividend. It costs them $13.5 million. The shareholder earns $10,000. The share price drops to perhaps 1-cent. The shareholder takes the $10,000 and buys another 1 million shares at 1-cent. He now owns 2 million shares. The next dividend is for, let’s say, 1.25-cents. His 2 million shares earn $25,000 in dividend income. If the share price were to remain at 1-cent, he could buy another 2.5 million shares. He now has 4.5 million shares. The next dividend is for, let’s say, 1.5-cents. His 4.5 million shares earn $67,500 in dividend income. Note how powerful the synergies are when BOTH VARIABLES i.e. the cash amount of the dividend and the number of shares earning those progressively larger dividends increase over time. The annual dividend earnings rapidly increase from $10,000 to $67,500.

Theoretically, in fair markets the share price should drop by the amount of the cash dividend. A $100 stock issuing a $4 dividend will drop in price to about $96 on the “Ex-dividend” date. If this were to occur in Medinah’s case, the scenario would be much more explosive than pictured above as the share price would drop from its original 1.25-cents to only 0.25-cents and that $10,000 in dividend income from the first dividend could all of a sudden buy 4 million more shares instead of only 1 million more shares.

This can’t happen in corrupt markets like ours because the lower the share price gets the more obvious the DISCONNECT becomes and there are plenty of shareholders aware of the story with plenty of fresh dollars in their jeans from the previous dividend. This represents the WORST CASE SCENARIO i.e. the share price continues to refuse to budge like we’ve experienced for many years. In reality the share price will probably gap in the 30-day time period before each dividend. But in reality this is a pretty favorable WORST CASE SCENARIO.

THE CURRENT MINING SECTOR

I think an approach like that described above fits in quite nicely with today’s mining sector. There aren’t very many interested investors and those out there have all kinds of bargains to consider in the junior exploration sector. This is not an environment in which you PROMOTE yourself to success especially in corrupt markets. It’s just the opposite. You want to resort to MECHANICAL measures that are predictable. If there’s a major DISCONNECT you lever it. Period! A TRANSACTION or two helps you confirm and measure the size of any DISCONNECT as well as remove the UNCERTAINTY associated with whether an option is going to be exercised or not.

DUE DILIGENCE TASKS

- Try to gain an appreciation for how the early production opportunities and the cash flowing therefrom might ramp up over time. When might new production permits be granted? When might existing production permits be increased?

- What kind of mine life are we talking for all of these high grade near surface early production opportunities? Does 10 years or so sound fair? Will there be any gap in time in between the end of the cash flow from the early production opportunities and the open pitting of the porphyry?

- Are the stellar grades found at the Caren Mine adits in the Merlin 1 Vein likely to be representative of what is found at the same depth level elsewhere on the Merlin 1 Vein?

1 Like

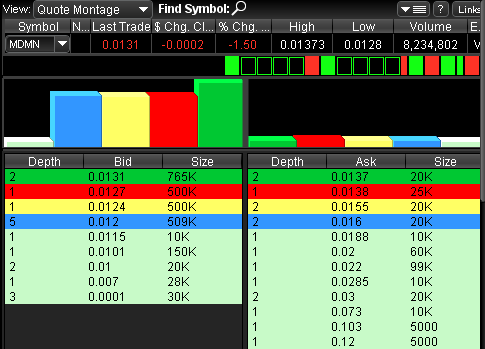

Nice to see the BIDS building. Hopefully it can start taking out the ASKS

1 Like

An alternative opinion . . .

It’s very likely that there will not be any cash to MDMN. In my opinion, MDMN won’t be able to sell any of their interest in AMC (at least for the near term) and if they did it would be a huge mistake.

This is not difficult and it doesn’t need a book to solve.

-

MDMN will end up owning a percentage of AMC.

-

AMC is going to be cashflow positive this year and next year will likely begin to distribute a portion of their profits to shareholders.

-

Tighten up MDMN. Clean up the books. Maybe completely get rid of MDMN (and its stigma) by merging into a listed shell with a reputable / fully trusted BOD. List on a real exchange. Possibly put the company into a business trust (if it’s economical to do so.)

-

Remain as a publicly traded pass-through entity and live off what AMC produces from the mountain.

Assuming the world stays relatively stable, environmental issues don’t crop up, and Chile stays mining friendly . . . If AMC executes properly we’ll be seeing annual distributions that return close to 100% of today’s share price every year!

If there is a humongous short position, it will take care of itself.

Here’s reality. Those buying now are buying in at an undervalued price. Those who bought in during the hype of the Ulander move bought into an overvalued price. The penny stock story is done! There’s no more milk in the cow for those who played that game. We are now tied to a real junior mining company who owns (or will own) one tremendous property. We will live with what nature has given us.

moo.

7 Likes

The new deal without cash at least 10 mil is unexcept able like I said at least 10 mil to reward shareholders on short term. Dividend at .005.

2 Likes