MDMN discussion for week beginning 2016-04-04

Sooooo… according to the most informed posters, we should get some major news this week, actually even today…

Wouldn’t that be nice…?

1 Like

Hope it is not going to be shown after hours.

If you follow the bread crumbs I believe it is relatively obvious what has been happening. First someone knew that the deal was going to change a long time ago to no cash deal and as a result they did not want to wait and has been unloading the stock. JJ reluctance to sell his shares has probably forced Auryn and the Letts to change their strategy. They now have probably abandon buying out MDMN shares, therefore they now probably do not need to control MDMN and as a result Mr Letts has abandoned ship.

We had something that was rather firm and riskless assuming that Auryn could finance the purchase offer, to something that is now more risky, since it will all depend on production results, mining operations, and commodity prices to produce MDMN cash flow.

The pieces all seem to fit the new equation but the real question remains as to if we are better off or worse off. Better maybe in that we may have some positive cash flow sooner. Worse off probably as to establishing the true value of our stock, since we now own 25% of a private company which is hard to monetize unless it is sold or goes public. I see now no reason for Auryn making us a TO, since they can wait a long time before we recover $100M in cash flow from operations.That could all change with great production results and cashflow to MDMN, But there is now no urgency as to MDMN stock price since the $100 M purchase option has been removed.

I believe we have gone from a year and a half wait for the exercise of a $100 M purchase option to a much longer wait before we get over .07 in stock price. JMO

5 Likes

Thanks Karl for the kick in the Nuts this morning!

2 Likes

WTF When are we going to get some transparency?

“Worse off probably as to establishing the true value of our stock, since we now own 25% of a private company which is hard to monetize unless it is sold or goes public.”

You nor anybody else knows what assets Maglas has therefore you cannot make a prediction like this. Wait until they disclose their financials and then take it from there.

Just stating as I see it, and still looking for a silver lining which maybe there if MDMN still refrains from issuing stock to finance day to day operations, generates enough cash to pay off the debt of about $2 M and can go positive cash flow to the point they can pay a cash dividend. If those pieces fall into place my tune could change.

1 Like

No prediction just stating the fact that it will be more difficult for MDMN’s stock price to reflect the true value of our 25% interest in Auryn other than our cashflow from Auryn. Auryn could be worth $5 Billion, but for us to realize our 25% of that $ 5 Billion it would require either Auryn to be public trading (open market stock price) or for someone to buyout Auryn to $5 billion. JMO

That’s not how the market works. If a public company owns 25% of a private company worth $1B. The public company will trade with a valuation around $250M with a discount. The discount will fluctuate based on the anticipated liquidity of the private company (IPO or M&A).

I don’t agree with your comments on a TO. As soon as AMC believes that 25/35% of the value of the mountain exceeds the market value of MDMN/CDCH they will move to tender at a discount to that perceived value. Once they are able to “prove up” the ADL to the point where it can be monetised they will move to buy us out. IMO

First it is hard to verify or even ascertain a private company’s valuation and second you are right if the market can it usually trades a discount! That discount will depend on how the market perceives what it values as being closer to the fact.

I have yet to see a balance sheet for Auryn have you?

I guess MDMN would have to value their 25% interest in Auryn somehow on their balance sheet !

2 Likes

You should look up www.auryn.com. Very appropiate.

Weren’t you just saying a little while back that when mdmn starts to receive revenue, it should legitimize? You’ve also stated your opinion that a short position exists and that if a dividend is paid out from Caren production, a squeeze could take place.

If you know something that has changed your opinion, what is it?

1 Like

If you expect for AMC to go dark on all of their exploration results, let alone gross production figures in the shorter-term, than we will have problems valuing the private company. At this stage of the game, AMC’s “balance sheet” has just about nothing to do with being able to assign a value (as is the case with valuing most private companies). The only assets that matter are those they are finding and/or extracting out of the ground. FWIW.

AMC’s in the driver’s seat. As soon as they think their value is worth $X they will buy us out for 10, 15, 20 cents ($X - pick your discount). I guess the ultimate irony (for some posters) is that AMC is going to be the one leveraging the DISCONNECT to their advantage not MDMN’s. This is what happens when you lose control and why the HISTORY (discussing our incompetent BOD) is and was a very pertinent variable when discussing this investment.

I’m not sure how anybody could have trusted our BOD to take any action that would benefit shareholders (it would be first) so now it’s up to AMC to “drill baby drill” to expedite our exit (hoping this year). A TO will present itself BEFORE the ADL is monetized. IMO.

3 Likes

THIS IS GETTING TO BE SUCH A JOKE ! We’re paying $13,102 + $95,081 (almost $110,000) so the accountant and the legal dept (LOL) can cut and paste the same mistakes over and over !!!

NOTE 10—INVESTMENTS

On February 7, 2012 a joint venture agreement was signed on the Altos de Lipangue properties as to an option to sell 85 percent of these properties for $180,000,000 to be received over a three year period from Amarant Mining.

During the year 2015, the Company accepted 750 million shares of newly issued Cerro Dorado, Inc. in exchange for payment of a $151,325 receivable.

I THINK IT IS WAY PAST TIME FOR AN INDEPENDENT AUDIT. We are losing shares hand over fist.

Sixteen thousand dollars for Offices - Which of these offices can I contact ?

Salaries and wages $71,381 , Management fees $104,410 = $175,000 to our BOD for ???

Operating Expenses:

Salaries and wages71,381$

Repairs and maintenance3,011

Rents14,404

Travel56,694

Automobile2,395

Bank charges10,016

Legal and professional95,081

News service27,513

Office7,502

Las Vegas office8,500

Postage2,394

Telephone14,296

Accounting13,102

Computer repairs7,092

Management fees104,410

Trust and transfer78,478

Web site6,998

Total Operating Expenses523,267

2 Likes

I have repeatedly state that cash is king and positive cashflow is the kingdom, especially if that cash flow goes to the shareholders. Yes If there is a short position and there is a distribution of cash to the shareholders that would probably cause a major short squeeze.

All I am saying is without any upfront cash I believe there is substantially more uncertainty and more risk to our investment and causes a substantial longer time horizon for the appropriate return.

1 Like

I believe that is what I said that the cashflow from production will be what places the value on MDMN shares in the short term!

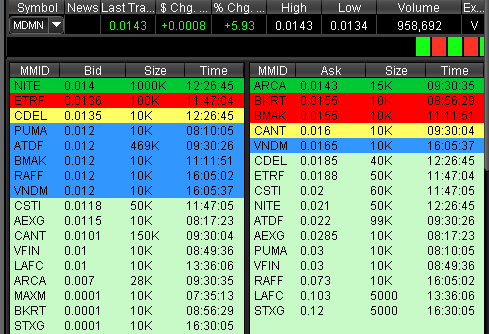

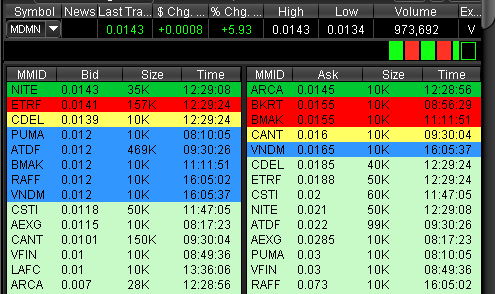

1,000,000 share bid @ .014

and then suddenly the Million share bid causes someone else to step up

1 Like

Total Operating Expenses $523,267

3.55 Million shares issued for services so far (2015).

Advances (repayment) of stockholder loans $838,993 (This money went … where? )

Expenses paid with stock $73,880

Leaving ??? # of shares to be given @ $0.015 (or less) to make up the Total Operating Expenses &

Advances of stockholder loans