MDMN discussion for week beginning 2016-04-11

I hope Auryn will release all mdmn mining data they are sitting on when the deal is officially signed. The rumor is that there are significant findings that they have not been released. Hopefully, that will help increase the sp.

1 Like

It’s nice to see a stock like MUX move then watching this stock sit idol

Also Gold up to 1253

GDXJ 31

So much for our SP being tied to the price of commoditie. With us finally closing a deal on the ALTo we should be trading at a minimum .04

3 Likes

I hope so but I hardly believe it.

Just like clock work, he’s back. Those 1.8 million shares (beginning as 2.5 Million) have now been used for a week to cap the price and cause anyone looking to sell to move to a lower price.

Is this someone who is simply looking to sell these shares and does not care how long it takes to get 1.5 cents for them? Whatever the answer, he has reduced the short term flipping opportunities, at least until someone else has reason to step up and buy the lot.

I’m looking forward to Auryn’s next update. Especially if we have to wait until after Les puts his finger print on the paperwork in Chile.

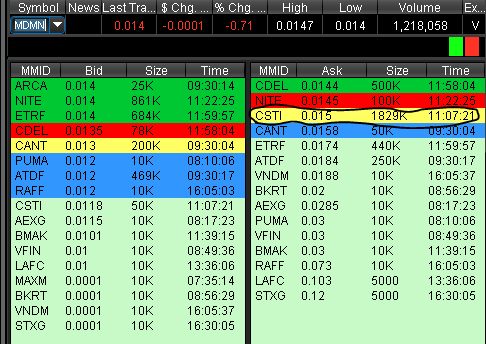

upated L2

1 Like

You are correct.

Speculation alone took us to .19 with Partner A and to .16 with the Swedish Sensation. That means we cried wolf twice. Are they gonna believe us for the third time just on speculation?

I truly hope so!

2 Likes

Hi Commerciante,

I’m confident we’ll get there but for now I think it’s a bit premature to take the terms of the 5% option i.e. each percentage point of the mining district/AMC being worth $10 million and extrapolate that to Medinah’s proper FMV today. In regards to this option, even more exciting to me is the possibility of some 3rd party having their arm around Medinah currently suggesting that Medinah management get AMC to throw in a 5% “clawback” option like this just in case the values of the mountain blow us all away.

I just can’t see Medinah management asking for that option without somebody else suggesting it. Instead of spending $50 million on another 5 percentage points of AMC in addition to the 25 percentage points upon inking the deal, I would think Medinah would be more interested in doing just the opposite and raising cash. Of course, a couple of long intersections into the Cu-Mo porphyry and all of a sudden that option might be worth a pretty penny and be in high demand.

If you parse the contents of Medinah’s last PR real carefully, I think we’re selling ourselves short by putting a value on the consolidated mining district/AMC and assuming that Medinah should be valued at 25% of that number. I think we’d be better served to think in terms of “MEDINAH’S PARTICULAR 25%” of the mining district/AMC because of the various terms and conditions (T’s and C’s) cited in that PR.

Assuming a potential 20 to 30 year mine life or so, Medinah appears to have a “free carry” on all future “exploration expenses” like mapping, sampling, geophysics, etc. Those expenses over that time span are going to represent a lot of “savings” (increased income) to Medinah. The same goes for the “free carry” on all drilling expenses. It’s going to take many tens of millions of dollars of drilling to do the block modeling for the porphyries and do the kriging and the pit optimization studies.

It appears that we also have a free ride on the mining costs themselves as far as day to day operations. This would include the on site working face drilling, stuffing, blasting, mucking/scooping, stockpiling, loading, etc. The mills and smelters typically auto-deduct the cost of milling, smelting, reagents and TRANSPORTATION if they supply the trucks. So it appears that Medinah will be on the hook for these built-in costs. As far as the “encumbrances” like taxes and surface rights payments it appears we get a free carry there also. There are rumors circulating of a contractual mandate that Masglas must also build an on site processing plant at their expense.

This will benefit Medinah greatly because the TRANSPORTATION charges will be a lot less since the product shipped will be a much higher percentage “concentrate” and less truckloads will be needed to ship a fixed dollar value worth of ore. Medinah’s share of the built-in “crushing/milling/reagent” fees charged by mills and smelters will also be lessened since a lot of that will be done on site at Masglas’s expense before shipping to the mill or smelter. To me, this appears to be a well-designed “win-win” with the main loser being the tax man.

If the original terms of the option stayed in effect and Masglas handed a check for $100 million to Medinah then I would imagine the tax man would have been right there at the ceremony grabbing a check for perhaps $20 to $30 million of that. That’s the last thing “partners” like Medinah and AMC want to experience. With all of these “savings” being granted to Medinah their quarterly checks will be much higher than otherwise but the tax consequences more drawn out.

One way to visualize this structure is that Masglas did indeed give Medinah a bunch of cash up front, the tax man got none of it and Medinah metaphorically handed the cash back to Masglas to pay what would have been their 25% of all of these various costs and “encumbrances” if this were more of a “working interest” with Medinah on the hook for their pro rata share of all of these costs/encumbrances. Net-net, between Medinah’s approximately 28% of “the action” for the mountain due to their retained 15% Nuoco stake and all of these “savings/delayed earnings” I would think that from a valuation point of view Medinah’s “package” might be valued at more like one third of the value of the overall mining district.

From a valuation point of view, the question arises as to what is the value of this Medinah “package” of ownership interests in AMC, the 28% of “the cash flow action” on the mountain, the free drilling, the free exploration work, the lack of “encumbrances” associated with paying the annual property taxes and/or the surface rights fees, the free mining/operations, AMC’s management team calling the shots, the infrastructure, the cash flow from the future discoveries, the eventual cash flow from the porphyry mining, etc. How appealing is this particular “package” of assets/savings to other parties (or Masglas) now that the entire mountain is open pitable subsequent to the property finally being consolidated? What is the worldwide “supply” of comparable “packages” in an infrastructure like this? Is some third party behind the scenes designing this “package” and this new 5% option for themselves and Medinah is just a puppet? Owning as many Medinah shares as Masglas/AMC currently does or in the future will own, are they not financially incentivized to “broker” a lucrative deal between Medinah and a major mining third party?

4 Likes

My whole heart is with you, it’s just my brain that is a little slow to catch up…

Slow day question. It has been posted that Letts is no longer involved in AMC/Masglas. Did I miss something or is this speculation. TIA

1 Like

He’s no longer on the BOD for Medinah. I don’t know about him not being no longer involved with AMC or Masglas

I am not sure why almost everyone is “assuming” that our share price will move dramatically, if and when we close the deal later this month. If it was that easy, we would be surely be seeing some more buying at this point. Or at the very least, less selling. I guess the general belief is that the buying will come in “after” the deal is completed. Perhaps even by Auryn. My expectations are hovering at a high of .05 in the next 90 days, based on a signed, sealed, and notarized agreement. Frankly, I would be thrilled with that, and would love to admit that my prediction was on the low side…

As stated Medinah is an “Asset Holding Company”. Until Auryn starts to mine and Medinah benefits from their efforts and we actually have assets I do not see appreciable PPS improvement. I feel bad for those on the edge but that’s how I see it.

2 Likes

I don’t see it that way at all. The market typically looks out 6-8 months. It will this time too…after we bury the boy who cried wolf.

1 Like

Hopefully your vision is better than Uneverknow.

BTW, who’s gonna be the undertaker?

The weekly chart is showing a double bottom with the potential now for at least a re-test of the low to mid - 02’s. We do seem to be leveling out and the time that this is taking could easily be reflective of the timeline we could be looking at in terms of income from production, which is still several months to possibly years away, depending upon who you choose to believe.

It also looks like the 1.8 M seller through CSTI at .015 has disappeared for the time being.so far today.