Yes please. Give Andy his alias back. He was smarter as Done Deal… l

l

3 Likes

He was smarter as Done Deal…

Let me see if it’s possible for you to switch back.

My answers to the above were.

“It’s a brand new MDMN but . . . “

”$0.10 . . .”

"$0.20 . . ."

“As long as AMC / MDMN pay dividends . . .”

4 Likes

You are now back as DoneDeal.

2 Likes

Seems like most would like to stay around for the LONG TERM and collect dividends. That’s fine with me. Another poll question. At what share price would you accept a Tender Offer? I do not know how to create a poll. If the poll is worthy help would be appreciated.

Tweek it as you please.

0.10…0.20

0.20…0.30

0.30…0.40

None of the above

.30 - .40 for me.

1 Like

The first time a TO is offered, regardless of how fair some here may consider it, it is likely the PPS will rise above the TO. This will allow those who wish to exit to do so. This first TO offer should therefore be rejected and allow those who would like to collect a dividend to collect a dividend for a while. This strategy would be successful unless the mining market does not recover. Of course, if AURYN proceeds to gain a controlling interest, as others have suggested, this strategy would not likely work as MDMN would have effectively been acquired by AURYN. It may be one reason why JJ has not completed the 350M share transfer. Perhaps we will learn otherwise when details of the recently completed meetings and negotiations are announced. At any rate, every shareholder should have an acceptable exit strategy and PPS in mind by now.

1 Like

I don’t have a firm PPS in mind. There’s are way too many unknowns and AMC has barely scratched the surface. Until we have industry standard resource to work with and/or until there is a consistent and predictable stream of production it’s impossible to determine value.

The probability of a TO as our ultimate exit is really up to AMC. They control the largest block of shares which may grow (hopefully) via JJ’s last remaining shares or open market purchases. The “larger” shareholders will, IMO, take anything in the 10-20 cent range depending on time and results.

If AMC reaches a point late this year, early next year, where the cash flow from production exceeds their needs for self-funded exploration, it wouldn’t surprise me if they use those profits to buy shares of MDMN in the open market. That’s what I would do.

1 Like

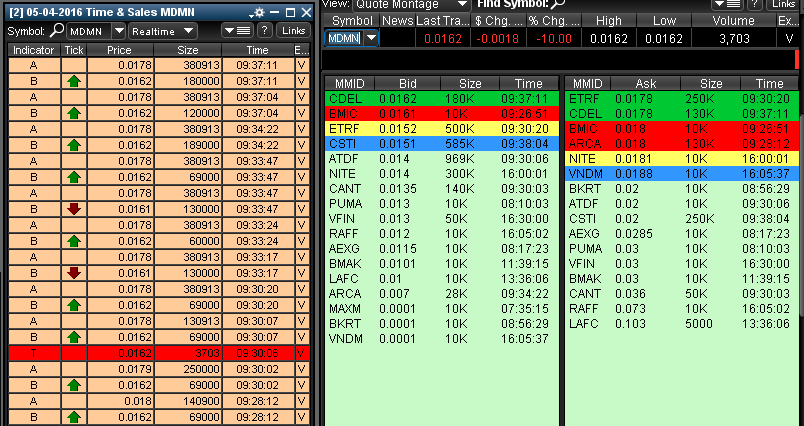

3703 shares @.0162? A bit obvious

Loosely speaking, if AMC did reach that point of cash flow exceeding expenses wouldn’t that generally be considered profit? If there is profits then wouldn’t those profits be shared between partners based on percentage of ownership? Based on currently assumed ownership percentages, for each $7.00 of profit AMC received that was available to purchase shares then wouldn’t MDMN have possibly received somewhere between $2.50 and $3.35 available for paying bills, buying back shares, and issuing dividends.

Once MDMN is in possession of income from shared profits I would expect the share price to increase substantially above our current position. Would you agree?

Don,

The assumption of your calculation is that there is SAVINGS = $0. If there are expenses in the future that may require more money than what is being generated on an ongoing basis, then the decision could be made to save that money and use it in future development (construction).

That is why when you look at mining companies (or any company for that matter) their cash balance in the bank account is non-zero (if they are healthy).

E.G. - Barrick Gold pays a measly 0.4% dividend. They have $2.5B in the bank in cash.

Q: Where did the cash some from? A: Savings from past profits which was not distributed to shareholders.

4 Likes

Not too many sellers out there a bit of buying pressure and the stock will pop.

Thanks for responding and I do understand your point(s). My post was mostly offered to see how BE felt about MDMN’s likelihood of seeing profits from production as he was commenting on AMC in possession of profits. I have to assume that he believes that if one partner would receive profits from production then all partners would be entitled to receive profits. Of course, you are correct that it is very likely that if the decision was made to save that money and not declare any profits then neither partner would have profits to share from, but just to follow along with BE’s assumption that if profits were available to AMC then those same profits would be available to all partners, including Medinah.[quote=“cornhuskergold, post:72, topic:1234”]

The assumption of your calculation is that there is SAVINGS = $0.

[/quote]

After considering your “savings = $0.” point, it occurred to me that it does not have to always be " $0." if there is declared profits. All of the partners could agree that 50% of all production income is returned to fund cost and saving for future cost and the other 50% is declared as profit to be shared by all partners based on their respective percentage of ownership. (The cost/savings vs. profit percentages could be moved around to reflect any number. 50/50, 60/40, 40/60, 90/10, etc.) The point is that, while saving would grow slower that 100/0 the partners would begin receiving some amount of profit income as soon as income exceeded cost of production. Unlikely but possible?

Yes. And that is exactly what typically happens. And that is exactly what is occurring in the Barrick example where they are paying a 0.4% dividend but otherwise saving profits.

The point others have made, (HR, BE, etc) is that as a minority shareholder in AMC, we do not control the decision to set the “if and how much” decision (the ‘percentages’ as you outline them). As far as anyone here knows, there is nothing to compel AMC to set the dividend percentage to anything other than 0.

Another related argument has been made that the probability of anything other than 0 is low because of the need for profits for future development. And I have responded to this argument saying: it is not unreasonable according to my calculations to believe that there could be excess profits for a year or two before the serious expenses come. So imo dividends are a possibility but in no way a certainty given our current state of information.

Clearly the ‘dividend meme’ is a strong one among MDMN shareholders and has been even among the BOD etc. over time. There is a strong desire to believe the meme. That always makes me suspicious of the meme. So far Auryn has said nothing about it. That makes me more suspicious of the meme. The current industry practice is no dividend or very small dividends. That makes me even more suspicious of the ‘big dividend machine’ meme.

On the other hand, Masglas is a big AMC shareholder. It would benefit them as well, as long as it does not harm long term plans.

So IMO, I would not buy shares based on this meme alone (there are plenty of others, imo). But I wouldn’t be shocked by it either. Once we see more details on production (tonnage increases, expected grades) and if the POG hangs in there or continues to improve, then we will be in a better place to assign odds.

4 Likes

How will AURYN produce a revenue stream quickly and cheaply from the Merlin and Fortuna claims? On Monday, George Young and Jose Manuel Borquez Yunge (part of the new BOD for Cerro Dorado) made a presentation that mentioned the equipment to be used on a proposed gold recovery project. The Alto Adigio project for the “new CDCH” is designed to generate cash from a near term, small scale reclamation of ore tailings. The equipment for gold recovery that was described is a gravity based system capable of processing 100 tons of ore per hour (2000 tons per day) which was efficient (75% recovery for the previously crushed and “washed” ore tailings). This type of equipment is portable and relatively inexpensive. Units were noted to be available for lease cheaply (shorter term projects) or purchased for the long term at bargain prices due to the several year down-turn in the mining industry. Specifically, proposed for use was a Knelson Concentrator - a hydrostatic centrifugal bowl-type concentrator in which a high speed, ribbed cone traps heavy particles (gold), while lighter particles in the ore slurry are washed away. It uses much less water than the conventional sluicing methods. Of course, if AURYN was to go this route they would also need to set-up a grinding/crusher circuit to obtain ore of a size amenable to the most efficient recovery. This method, if deemed suitable, would have several desirable features. It would be environmentally friendly, not involve chemicals, and be ideal for an initial gold recovery plant prior to shipping concentrate that could be up and running quickly. Tailings could be stored for later cyanidation techniques used after a heap leaching plant is constructed. Will we hear any news regarding progress in this direction?

2 Likes

On this point I keep reminding myself that Medinah was setting at the most recent negotiations and holding a card that said “you owe me $100 million if you want to exercise your option”. That would have been a perfect time to play that card for an agreement that resulted in a win for both sides of the table. I just hope they were smart enough to sell the concept. We could know the answer within the next week or so.

Too many unknowns still re dividends.

What happens if Caren. averages 80 gpt. or 100 gpt?

What happens if gold exceeds $1500 or $1800?

If these things happen, I would think there would be enough to go around

Could go the other way too but not enough known for anyone on this board to make a definitive call IMO

Now it’s NITE with the 1 mil bogus on the ask he and ETRF are taking turns trying to discourage buyers.