There’s a lot of that going around

Sure is!!! I do own some

I think there were a few who did sell believing MDMN was in a holding pattern until production started. Maybe they will transition back.

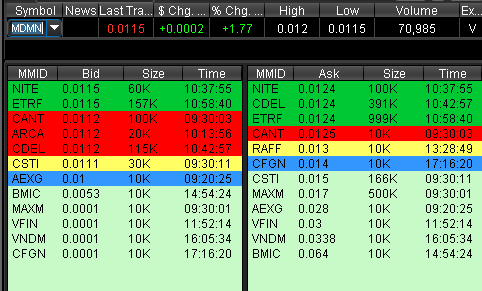

Wow somebody just keeps dumping 1.5 million on the Ask .0124

2 Likes

Seems endless dumping. Got to wonder who and why?

Yes Who, Why and When will it stop.

Could it be the higher ups are converting the preferred and selling. Also GC is owed money back for all the years he kept this company around could it be him selling??

This selling makes no sense knowing what Auryn is doing to the mountain. So my thoughts is its an insider selling that has No cost basis jmo

It’s probably bogdan manipulating the stock so he can buy back those shares…

(TIC post)

(TIC post)

1 Like

Rick, Thanks for this post. I suggest that anyone who finds themselves questioning why they remain invested in Medinah return to review your words to assist them in finding the answer.

3 Likes

This is much better than a crystal ball.

We are all set now…lets see what it does for us.

TDK

2 Likes

Maybe we should suggest to Kevin they install a webcam at the adit ,that’ll keep some people occupied. I’ve actually seen it done by a couple companies

1 Like

Only 54 days before the Informational Meeting (financed by AURYN/MASGLAS) where shareholders are sure to have a clearer idea of where we are at, and plans/expectations for future monetization. An hour to have questions answered by the new Medinah BOD, and an additional hour for Q & A from AURYN promises to be very informative for all shareholders.[quote=“Hurricane_Rick, post:461, topic:1377”]

For me, this is the time to buy…

[/quote]

Incremental buying by current shareholders is absorbing the shares being offered. It is unfortunate if available shares are being sold by those needing to meet financial obligations.![]()

This is not a time to feel hopeless or fearful. AURYN is indeed continuing to show progress!

1 Like

Silver Falcon Mining comes to mind. It didn’t work out well for them. However,this mine operation is at a whole different level. I like the idea once the mine is producing.

So we can count the loads actually leaving this time😎

1 Like

(WARNING: doc just had a cancellation and had an extra hour of time on his hands.)

It feels to me that we’re coming to the end of a transition period during which the market perceptions refuse to budge from historical mode and convert over into present/future mode even though prior management is completely out of the picture. In the mining sector, historically this time frame right before going into initial production has proven to be the investment sweet spot of choice but this is clearly not the case for the Medinah market yet anyways. I was expecting at least a small pop in the PPS when the new BOD came in replacing the much maligned old BOD and the production timing firmed up but no such luck.

If a development stage miner can successfully make the transition from posting typically a couple of hundred months of zero production to actually getting some monthly “production runs” on the scoreboard the statistics suggest that this will probably continue for some time i.e. the projected mine life. Why? It’s because the big bucks dedicated to engineering, mine prep, infrastructure development, permitting, etc. get spent up front and won’t be spent unless the projected mine life and projected economics justifies it. Since the positive production decision was made by AMC, gold has gone up over $200 per ounce as the share price continues to slide. How long this divergence can continue is anybody’s guess but there has to be some potential energy being stored up somewhere once it does turn the corner.

If the mining district being developed has multiple early production opportunities wherein the permitting process is advancing smoothly then the projected ounces of production can take on more of a parabolic flight path as both new sites become permitted simultaneously with existing permitted sites being allowed to increase their production rates. Whether the new producer is publicly traded and has cranked out the exchange mandated 43-101 compliant technical reports, a formal preliminary feasibility study or a more detailed bankable feasibility study confirming positive economics or if they are private and don’t need to it doesn’t matter. The deposit is not going into production unless the engineers have proven to management that it is ECONOMIC and all of the permitting and environmental hoops and hurdles have been already successfully cleared.

Although we shareholders don’t have access to it, there is a very long list of milestones that has to be checked off on prior to that first truck heading down the hill. This is a part of the “derisking” process for prospective investors. We also don’t have access to Masglas/AMC’s risk-reward analysis that they, as prudent mining professionals, follow before cutting the next round of checks but the checks keep getting cut. The lack of visibility in dealing with a private entity isn’t a lot of fun for anxious investors but we can easily sense that the actions of the “smart money” involving massive share purchases and exploration/development dollars being spent certainly don’t align with Medinah’s dwindling market cap. It wasn’t that long ago that “AMC and associates” (the smart money) was paying nine times the current share price (10-cents) at the end of their purchasing of their first 150 million shares. This was back when going into production seemed to be an eternity away.

My own takeaway is that the market will place pretty much ZERO trust in Medinah until the new management team irrefutably proves the bona fides of the deposit and their ability to monetize it. I sense that there won’t be any “credit” extended to Medinah by the market until this time even though those of us that live and breathe Medinah may have no doubt that Masglas/AMC is highly likely to knock the ball out of the park on this project. The flip side of this lack of any extending of “credit” by the market is that there might be a bit of a frenzy occurring when the market does get confirmation of the bona fides of the deposit and the new management team’s ability to exploit it.

In addition to being taken out by a major, going into production and generating cash flow is obviously the rarely reached goal for the junior explorers as a group. For Medinah, whose market cap through time has rarely reflected the positive corporate developments being achieved by Masglas/AMC, gaining access to positive cash flow also opens up an entire new world for management to provide shareholder rewards through share repurchase programs and cash dividends that are not subject to the vagaries of an untrusting market hung up on the past.

If the market for some mysterious reason absolutely refuses to provide shareholder rewards proportionate to corporate success then management can simply take whatever portion of the profits they can allocate to share repurchases and buy back and cancel large amounts of mispriced shares. If the market perceives that management’s accomplishments have paved a pathway to several decades worth of hopefully progressively larger cash dividends then the repurchasing and cancellation of a large amount of shares early on will increase the amount of all of those subsequent dividends on a per share basis.

In Medinah’s case, having access to that second route to provide shareholder rewards, if needed, provides the quasi-guarantee that shareholder rewards will indeed parallel positive corporate developments. Until you enjoy positive cash flow, however, there are no guarantees that shareholder rewards will mimick positive corporate developments. Thus Medinah/AMC finally making it into production after all of these years represents a very critical milestone to reach when it comes to the provision of long overdue shareholder rewards.

12 Likes