You can thank Les Price for that. In the meantime, and also thanks to Les Price et al, the company is in survival mode. They have no money except for that which has been loaned to them. Shareholders need to understand this. Revenues from ADL is not a given. Nor is clawing back the shares. Nor is the outcome of the lawsuit. Until these items are straightened out, the future of the company is in limbo. Do not expect the company to be concerned with share price or attracting new shareholders at this point. Those are afterthoughts of a publicly traded company that is on solid footing. Right now Medinah is just trying to pay its bills and recoup damages while it digs out of the hole.

4 Likes

I’ve been buying as well. I suggest opening up another account with a different brokerage house. There are plenty that will allow you to buy MDMN.

I believe it was similar to the US with a 30 day window for response. If anyone wants to look it up, here’s the link CSO - Search Civil By Party Name search for organization “Medinah Minerals” it should pull up the three cases from the 4th quarter. I didn’t complete the search because it costs $6 per case and then they charge again if you download a doc, and I didn’t feel like paying for it. Meh. If something interesting happens, then maybe I will look. But right now nothing exciting happening bc MDMN just starting their forensic audit review with the new company. IMO once they complete and file amended pleadings then it would be worth the $6.

2 Likes

Shareholder crowd funding anyone?

I have just received my SS pension increase (1st in 2 years) for 2017 —$66 a year!

I can still chip in if we need to overcome CPA & attorney fees for this cumbersome filing. Future filings should then be easier, right?

3 Likes

If Auryn holds with their recent press release pattern, I would think we would see a new update this week?

Nov 15, 2016 ADL Project Update November 2016

Dec 24, 2016 ADL Project Update December 2016

Jan XX, 2017 ADL Project Update January 2017???

3 Likes

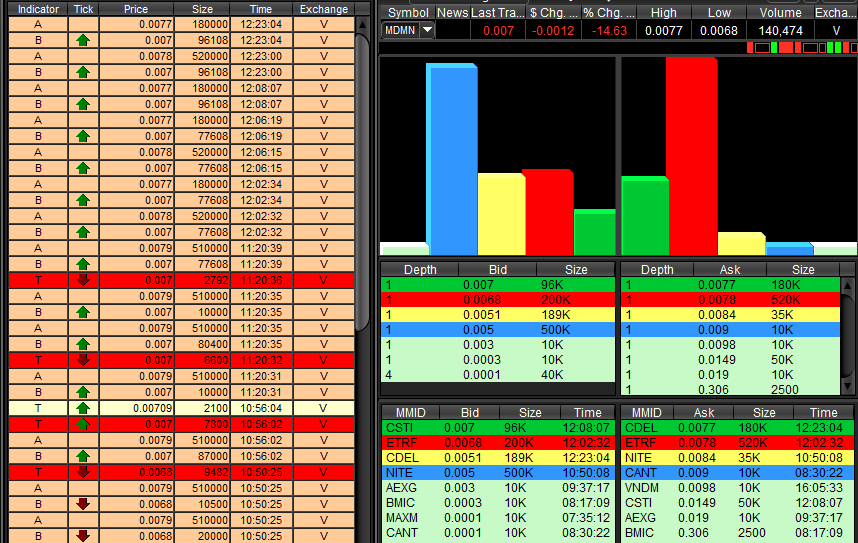

Stock price holding up nicely around .007, perhaps with great news we can crack the penny.

1 Like

Before the Les dumping of shares(blaming Claro) we were trading .08-.09 and that was with close to 3 billion shares outstanding. So you can imagine what kind of damage the slime ball has caused. On a positive note we have a new CEO that’s awesome and Auryn is shipping ore! now that should be valued at least and more before the dumping of the shares. Hold on folks because only positive things are on the way! Now where are those assay results??

9 Likes

That’s also my thoughts Hulk.

Hello there Hulkster!

Unless I’m mistaken, all we know to this point is that ore has been shipped for metallurgical testing - I’m not sure if we have started shipping ore on a regular basis for processing, but maybe I’m misunderstanding. I could be wrong, but if we are shipping ore, then GREAT, as that means income in the near future!

2 Likes

It is my understanding the ore is tested in order to arrive at a commercial contract for receiving subsequent future ore shipments for processing. ENAMI purchases the ore for processing, thus AURYN will have a cash flow based on the initial three truckloads for future ore shipments. Additionally, AURYN had reported last summer:

Metallurgical tests conducted at laboratories in Perú returned an average gold recovery greater than 90%. Test conditions confirmed the best recovery method entails use of a Falcon gravimetric system processing previously concentrated ore.

In November AURYN stated it had hired independent consultants to conduct a full granulometric analysis of ores presumably to see if on site pre-processing could make their ore shipments more profitable (fewer truckloads with concentrated ore shipments). Of course this would mean buying a crusher and gravimetric system. Cash flow from earliest truckloads of ore would be used for payroll, equipment purchases and further exploration expenses. This would be part of the conservative approach in AURYN’s mining plan. IMO

Yes, we should be hearing a report on the average gold content of ore shipped after the results are in. It will give shareholders an idea of how much each truckload of ore is worth and what AURYN expects in future quarters.

2 Likes

It is not absolute but it appears that one (1) truck transported the entire ore shipment in one run. I agree the ore in that shipment must have been concentrated. The transport truck is not one capable of holding 50 tonnes. There appears to be a cover over the dump body. The truck could be almost full or have only contained a tonne of concentrate. although the springs don’t appear to be heavily loaded. We just don’t know. . I thought we could pull 50 tones per day. Did we ship something less than 50 tonnes of ore or concentrate from ore? Anyone have any idea what we shipped?.

Still clear probably going to need definitive word from Auryn that production has started in a meaningful way, that the grades are excellent and some expected daily production numbers for Medinah to jump above one cent.

2 Likes

Lampa near the Alto is under “Red Alert” for fires.

The latest fire report does shows some fire activity near the Alto on the map:

1 Like

Bothers me less than a major earthquake.

They are getting towards the finish line of their promised at least once a month mining updates. Any news is better than no news at all.

2 Likes

Hi Mike,

While we wait on news regarding the preliminary Caren Mine production stats I think we should be prepping ourselves for keeping a sense of CONTEXT for whatever results we do receive whether good or bad. To me, the Medinah scenario has everything to do with the timing in the overall mine production and mine discovery cycle. The industry is currently at a 25 year low in new ECONOMIC discoveries. This is an industry in which if a major or mid tier producer doesn’t replace the ounces they produce annually then they don’t survive. For the most part the majors have shut down their own exploration efforts after overspending during the 2011 to 2012 peak in the price of gold. They’re now writing down those purchases. The industry is still producing about 90 million ounces of gold per year but new discoveries are nex to nil. The key metric here is supply and demand but not necessarily of copper and gold. It’s TODAY’S supply and demand of new ECONOMIC discoveries to feed the need for the majors and mid tiers to constantly replace their reserves. My thought is that the TIMING of AMC putting this particular discovery into ECONOMIC production (if true) could prove to be very fortuitous in this current mining environment.

Whether the Caren Mine preliminary results be good or bad, the most pertinent question then might have to do with whether or not we can assume that whatever ore tenor/average grade is being harvested as AMC advances southwards at the Caren Mine (Merlin 1 Vein) can be roughly extrapolated to be present in the other 5 adjacent veins i.e. Merlin 2 and 3 and the Fortuna Oeste, Fortuna Este and the Fortuna Centro Veins. Excepting for the Merlin 3 Vein which runs E to W, all of these “intermediate sulfidation sheeted veins” are pretty much parallel striking to the NNW. This simply means that the cracks, fissures and faults that were filled by rising metal bearing hydrothermal fluids were oriented this way. These are sometimes referred to as “en echelon” veins.

Keep in mind that the recent trenching program increased the lineal dimensions of these veins MAKING IT TO SURFACE from the 400 meters that Medinah and ACA Howe outlined to over 5,000 meters. The implication here might be that whatever the average grade mined from this overall well preserved epithermal system turns out to be then there is going to be a significant amount of ore/mine life if there is indeed “continuity”. The MAKING IT TO SURFACE aspect helps improve the potential ECONOMICS especially if the density of the veins and ore shoots makes less expensive open pitting an option. Remember the 25 year low has to do with ECONOMIC new discoveries.

What do we know so far about this system of veins? We know the most about the Fortuna Centro Vein (FCV) since it was in production from 1940 to 1970. The FCV is the second vein in from the east. One source says that the average grade mined was 92 grams gold per tonne while another states 64 gpt gold. The average gold grade being mined today worldwide is only about 1.5 gpt gold from open pits and about 3 gpt gold using underground methodologies yet these are currently ECONOMIC.

Of the 6 total veins on the eastern plateau we are 1-for-1 (Fortuna Centro) as far as having very high grades. That’s why I sense a bit of a drumroll while impatiently waiting for the Caren Mine preliminary results because 2 for 2 in the very high grade category sounds a lot better to me than 1 for 1 especially while trying to estimate what grades might be found in the other 4 main veins. I can’t think of a valid geoscientific reason why one would expect vastly different average grades (either lower or higher) from these various individual veins whose metal bearing hydrothermal fluids probably share a common progenitor magma chamber due to their proximity.

We also know that the whole system of veins averages somewhere around 3 gpt gold AT THE VERY SURFACE as we learned via the aggressive trenching and sampling program conducted by AMC. That average is also very promising for surface trenching results because the underground mines being mined at that same grade level are often hundreds of meters below the surface yet they are ECONOMIC. If the trenching results revealed ZERO gold at the surface then the expectations for high grades in the lower aspects of these veins would be lessened. While sampling the adits at the Caren Mine on the northern downslope off of the plateau we saw almost a linear relationship with gold grades increasing with depth. With “intermediate sulphidation epithermal veins” the gold grades tend to max out in the historic “boiling zone” and the silver, lead and zinc grades take over in importance often from the 300 to 900 meter depth levels.

We know a little bit about the “bonanza grade” samples (I hate that term due to the possibility of a “nugget effect”) taken from a couple of these adits at the Caren Mine in between 100 and 150 meters below the plateau level. “Bonanza” grades are all fine and dandy but we really need to see the “headgrade” or “mill grade” of the ore being shipped as well as some tonnage figures in order to crunch some numbers. This rules out phenomena like the “nugget effect” which in turn “derisks” the project.

Any high grade results attained at the Caren Mine will be somewhat corroborated by the average grades that the Fortuna Centro Vein has already revealed over 30 years of production. The 3 or so gpt average gold grades found at surface within these 6 veins would also be corroborative of something special from a grade point of view because we know that the high grade gold in these intermediate sulphidation epithermal systems are typically found deeper in the “boiling zone” where there was enough energy present to displace the gold from the “thiosulphate” complexes that it travels with in the hydrothermal fluids. These “boiling zones” average about 300 meters in vertical width. We also know that this overall epithermal system has been very well preserved from erosion as all 4 of the typical vertical layers to these veins are still intact.

Perhaps the most significant advance we can make in getting shipping results from the Caren Mine production is a means to FINALLY take pencil to paper and roughly estimate some valuations for Medinah’s 26.8% stake in the Caren Mine production at least from the Larissa adit (“adit 3”). Up until a junior explorer/developer goes into production, the valuation process even for the 1-in-1,000 junior explorer that made a significant discovery that successfully got advanced into production is notoriously difficult. Some ECONOMIC TRANSPARENCY would be a godsend especially keeping in mind Medinah’s corporate governance history and the resultant refusal of most investors to extend Medinah any “credit” towards the validity of their assets. This is the perfect environment for the market cap of a corporation to be totally “disconnected” from the value of its assets. If you think about it, what are the statistical odds for the 1-in-1,000 junior explorer to make a discovery of this scale and successfully putting it into production to have the corporate governance issues recently revealed in Medinah’s past? It defies logic.

Once into production then relatively simple “Net Present Value” (NPV) calculations can be made using “Discounted Cash Flow” (DCF) analyses employing a proper “discount rate” factoring in the time value of money as well as certain risks. Gold producers typically trade at anywhere from 1.3 to 2 times NPV per share. The more difficult estimation would then be to estimate the “production growth profile” as AMC carries out their plan to be producing out of 4 adits simultaneously at the Caren Mine as they outlined at the recent informational meeting.

Another estimation needing to be done has to do with the ramping up in the permitted production rate at these 4 adits as allowed by the Chilean authorities as AMC hopefully proves that they are good stewards of the environment. Further down the road any cash flow from the potential open pit exploitation of the Fortuna/Merlin 3 area and other areas within the overall ADL mining district that are put into production would have to be also factored in.

The “value” of a discovery obviously has a lot to do with grade, tonnage, geopolitical risk, access to POWER and WATER (if in Chile), infrastructural issues, technical competency in the type of deposit being mined, access to capital, etc. The TIMING of the discovery is also critical especially if it occurs during a 25 year low in new discoveries. This is because of the nature of any EXTRACTIVE industry wherein reserves/resources need to be constantly replenished. During times like these, reserves are replenished by ACQUISITION. The amount of bids being received and the size of those bids will be heavily dependent upon the “supply” of ECONOMIC discoveries that are available for purchase at any given time.

If you further refine the targets it is actually the “supply” of high grade, near surface discoveries with favorable infrastructures, within countries with little geopolitical risk, etc. Of course these are the same factors that enhance the ECONOMICS of the deposit. I have absolutely no clue as to what to expect as to the grades being shipped from the Caren Mine to the ENAMI mill or the associated costs. I do sense, however, that there is an awful lot riding on these grades when you keep in CONTEXT the overall AMC/Medinah scenario.

I highly recommend studying the presentation of Brent Cook found at the link below:

If you don’t have the time, a one sentence summary of what he reviewed in detail in a half hour is: “ECONOMIC discoveries made in today’s mining environment are going to be EXTREMELY valuable”. Brent is the premier industry geologist/mining analyst with the ability to sniff out the juniors with discoveries of merit that are going to be taken out by the majors. He made an interesting comment about today’s mining industry. He said that if he can’t currently find any juniors with new discoveries then the majors sure as heck can’t find any.

One point that might help you understand why I say that Medinah is the perfect scenario for the market cap to get totally DISCONNECTED from the value of its mining assets has to do with people like Brent. With the uncertainy raised by Medinah’s corporate governance issues even if a person like Brent studied the discovery and came to the conclusion that it’s the best discovery in a long time he would have trouble in recommending the stock from his own RISK versus REWARD point of view. He’s got a wonderful reputation to preserve and if somehow Medinah’s corporate governance issues could leave him with a black eye then it wouldn’t pan out from his personal risk/reward point of view.

Thankfully, major miners wishing to replenish their reserves wouldn’t have that problem if they were to simply purchase Medinah’s 26.8% stake in AMC and 37.7% stake in the Nuoco properties and structure it as an “asset sale”.

3 Likes

Brecciaboy, your one of the reason, I keep faith with MDMN

Be nice to wake up to some great news from Auryn.

1 Like