I did a little digging to see when and where this fraud started. I find it interesting that in 2012 MDMN became a reporting company by filing the 15c-211. At that time the accountant went back as far as 2009 up to June 30, 2012 to provide updated financials. In the lawyers letter Under Guidelines it specifically states Scott Jensen was responsible for the preparations of unaudited financial statements for twelve months ended 12/31/09, 12/31/10, 12/31/11 and 6 months ended 6/31/12. It also states The number of shares of the issuers common stock and preferred stock outstanding as of each relevant dates was obtained from the transfer agent. It further states that the Counsel confirms that the undersigned has met with the officers of the company and majority of of the Directors to review the information published by the issuer through the OTC Disclosure.

After saying that it makes me wonder where things slipped through the cracks especially if this fraud started in 2010, why it was not discovered at that time we became a reporting OTC stock!

Totally agree with your totally agree. Been saying this for a while now. Whether he has actively involved or not is irrelevant. It happened on his watch. The fact he overseas the investigation as to whether he acted correctly evidences a clear appearance of impropriety at a minimum and more likely a direct conflict of interest. As an attorney he should know better and resign to avoid the appearance of impropriety and/or conflict of interest. Right now it’s like the fox guarding the hen house. We don’t know whether we will get a truthful investigation.

I fully agree with the above statement, also. Illegitimate shares sold into the run-ups is very likely what led to much of the continued depression of the PPS over several years. A buyback of these shares on the open market is what is needed in order to return them to the treasury for cancellation. It should be noted that more than 150M shares have traded since August 2016. Perhaps the 57M shares being returned had restrictions and were never traded. It is also possible that these were recently purchased at depressed prices foreseeing a bargaining chip to avoid a prolonged but losing legal fight. The primary reason for 0.025 being the threshold for return may be to present a valuation for the total returned package (67M) of “street shares” at $1.675M by the cooperating individual. This may make a “hard number threshold valuation” of all remaining “illegal street shares” remaining to be recovered being presented to the court. Anyone care to do the math on that?

Focusing on the current events, never even thought about the previous attorney certification and accountant info. I think MDMN, if they haven’t already, needs to look into filing a complaint against Mr. Hackney with the Florida Attorney registration committee. Lawyer Complaints and Discipline – The Florida Bar And filing a complaint with any disciplinary commission for the accountant Mr. Jensen. They both verified the accuracy of the information in their filed statements over the years and they are wrong. Whether they made an honest mistake or intentionally used the wrong numbers, the error would fall under malpractice, either way. Both Mr. Jenson and Mr. Hackney should have malpractice insurance. And, although most malpractice cases have a two year statute of limitations to file, the limitations period is tolled until such time as the principal (ie: MDMN) knew or reasonably should have known of the malpractice. MDMN didn’t discovery the discrepencies until early 2016. MDMN still should be able to make a claim.

In most instances, filing a malpractice claim will result in the malpractice carrier settling the case quickly. Legal/accountant malpractices cases do not usually go to a trial, but settlement for the full amount of the policy coverage. Could be a way MDMN secures some funds relatively quickly to help with the more expensive litigation.

Someone with Kevin’s ear should contact him and run this information past him.

I agree, but first I believe MDMN needs to discover if the transfer agent was giving out the current numbers to all parties involved and if then it was someone else manipulating those numbers to the Lawyer, Accountant, and BOD. My guess is that the TA was not complicit and they had and gave out the correct numbers therefore the lawyer, Accountant, and BOD should be held liable, but you never know until you complete the discovery process if the TA was directly invloved . JMO

Karl, just to restate information given in October:

it was stated at the informational meeting that all share counts that came from the TA were e-mailed to Les, and that everyone else got the numbers from Les via e-mails in which he had edited the TA numbers. And further, it was stated that Les had presented documents to the TA, examples of which were stated to be in hand, where Les had forged BOD signatures authorizing the shares issued.

Further it was stated that it was when Gary demanded and received an e-mail from the TA directly that it was discovered that the numbers Les was distributing and the numbers the TA had did not agree. And it was when Gary discovered this that Les was confronted in person at the meeting that was occurring at that time in Florida, I think. And further, it was stated, that at least initially, in person, Les “admitted” to changing the numbers (although I’m sure Les would deny such at this point).

Assuming the above to still be the official information, obviously one wonders how the TA could not have noticed that the MDMN financials and the numbers given by the TA did not match. Did they never look at the MDMN financials? Good question. No answer given to date.

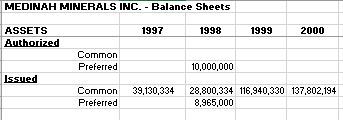

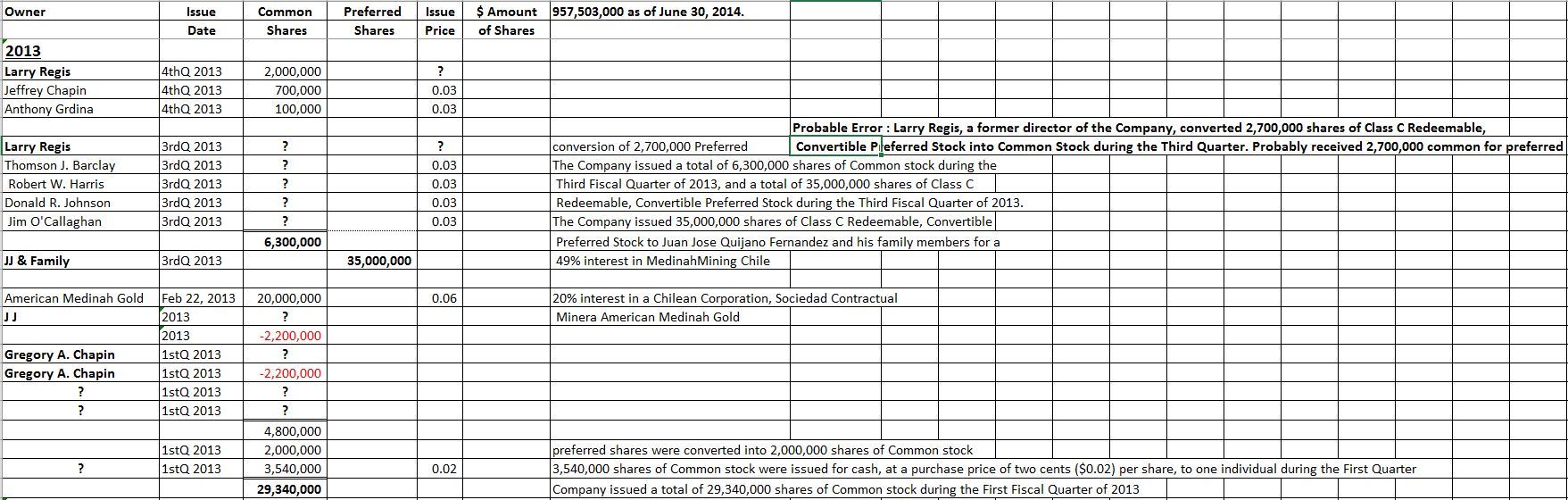

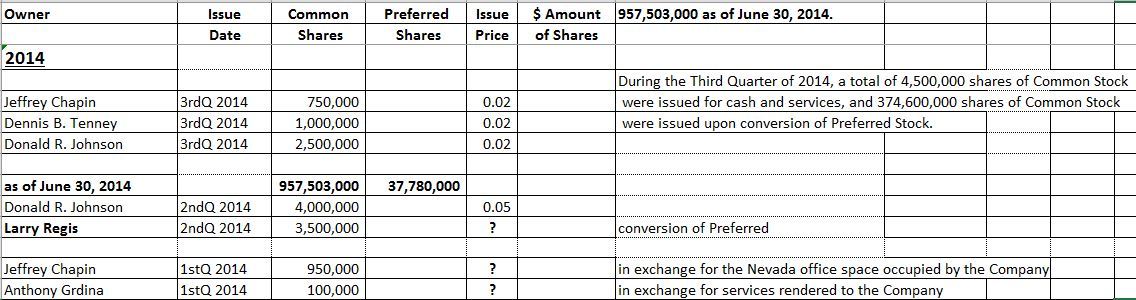

Here’s what I have from the historical records I kept from 1997 on. Much of the information is missing, as scant (or no) reporting was done on share issuance in the early years. IF YOU HAVE MISSING INFORMATION (from OTC filings, etc.) PLEASE INCLUDE THIS.