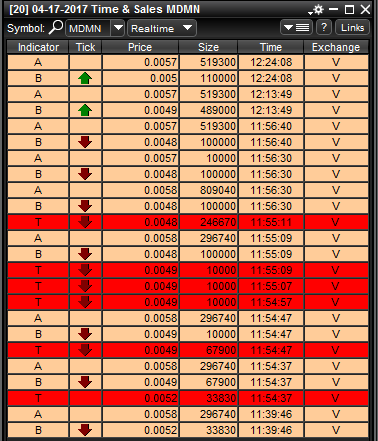

I can’t say AURYN is particularly concerned about MDMN’s current PPS, and why should they be? There is a reason that MDMN with 28% equity in AURYN was granted a $2 million interest free loan for two years. AURYN will be successful. The two year time frame is highly significant for MDMN shareholders, IMO.

Considering the number of detailed announcements AURYN has made in the past I do wonder if we are in a “quiet period” before some major announcements. I also wonder if additional permitting has been secured. AURYN completed an environmental and water monitoring survey a year ago at the Caren-Merlin-Fortuna area. Was this made in anticipation of surface exploitation using a Falcon gravimetric system? It was not so long ago that AURYN stirred much investor interest and speculation with excerpts of announcements making statements such as:

Of particular note are the extraordinary gold assays returned from the Merlin 1 vein, the first vein to be trenched, samples and assayed of five (5) parallel veins that outcrop to surface.

AURYN has focused its efforts on the Merlin Au-Cu±Ag high grade gold veins. Using a team of three (3) geologists and three (3) assistants, they have conducted geological mapping on the property on a 1:10,000 scale representing approximately 15% of the concessions. Over 1.5 km of trenching and over 200 samples of the 25 trenches and adits has been completed to expose the high grade gold in quartz veins that outcrop to surface. Gold assays have returned grades up to 66.5g/t gold with a weighted average of 26.9g/t gold on a diluted basis over widths of ~1.35 meter, adding high anomalies in Cu, Pb and Zn. These grades are better than expected. Currently the Merlin 2 vein is being mapped and trenches dug on 50 to 80 m intervals.

The mineralization in Mina Caren presents a mineralogical zonation in the vertical extension, with Carbonate/quartz replacement textures dominated in the upper level (1900 m RL) to quartz crystalline + sulfides textures in lower levels (1840 m RL).

These variations suggest the preservation of an entire epithermal system in the Caren sector, and demonstrate that the system is still open to the SSE direction, supported by geochemistry results anomalous in grab samples.

The mineralization at Fortuna target is represented by several parallel veins with NS to NNW trending.

Announcements by AURYN have included many well written progress reports, mapping, survey results, and expert personnel brought on board. There is one in particular made last June that still has me puzzled:

AURYN Mining Chile is planning to start production at the Caren Mine once mine preparation is completed, and we obtain the necessary validation from the Chilean mining authorities that the mine is designed according to the laws and regulations pertinent to the permits held by Auryn. The Peruvian experts hired specifically by AURYN have designed the engineering project and mining layout. According to the current exploitation license, the maximum tonnage allowed by regulation is 5000 tons per month. AURYN’s engineers plan to ramp up production to achieve this level of production during the next 6 to 8 months, with a cut-off grade of 15 g/t gold.

Metallurgical tests conducted at laboratories in Perú returned an average gold recovery greater than 90%. Test conditions confirmed the best recovery method entails use of a Falcon gravimetric system processing previously concentrated ore.

Granted, there were unanticipated obstacles that were finally overcome delaying the 1st shipment for 6 months. Anticipated production levels were not ramped up within the announced time frame. If information is now being withheld it could be for strategic/JV negotiating purposes, or possibly because we are in a quiet period in anticipation of making our F-1 application, IMO. I’ll give AURYN the benefit of the doubt for now. AURYN is in the driver’s seat. Is the best recovery method using the Falcon system that increases ore concentration 100X now being used but not reported? (This is the system that allowed AURYN in that same June notification to state, “These results make us confident that we can produce a total of 5,000 troy ounces of gold before year-end 2016, and over 25,000 troy ounces in 2017.”) Is this why AURYN is confident of attaining an initial listing on the OTCQB® tier? Is there anything that will ramp up value for AURYN’s IPO quicker than production results and the unfolding of the economic value assigned to the exploitable deposits?