Fadein, I think you and I have been around here for about the same amount of time and we are both on the same page on seeing this through. I first bought because of the mountain and that hasn’t change so lets get through December and get by the shenanigans, just maybe it will pay of for us both and everyone else that put up with this monster of an investment. Investment, that has a new meaning, or is it just another challenge in my life that I took on and never gave up on.

2 Likes

Per his post (above), Brecciaboy was buying a few weeks back. Is something gonna happen soon? Maybe he’s averaging down? I know I did. MDMN is at near record lows - I guess it’s a good time to buy anyway?

Do I recall information from some source saying we’d be producing in November, 2017? I do recall that MDMN was permitted to produce 5,000 tons per day as of January, 2016. Has that tonnage been increased? Hmmmm …

1 Like

I hope they are drilling or doing something, what happened to the Dr. Richard Sillitoe and Dr. Raymond Jannas report ?

Easy to guess that further exploration is predicated on a JV or positive cash flow from the Caren. Quite possible that neither condition has been met yet so Auryn maybe simply sitting on the report for now.

It is good time to add with full gold production to start shortly while Medinah share prices are at a low. From yesterday, it appears somebody is trying to dump at least 5 million shares so I suspect it will be a buyer’s market today and a Black Friday/Cyber Monday sort of day for Medinah shoppers!

Maurizio said production will start in November, didn’t he? Was he wrong? Sure would be nice to find out.

If he was right, it seems like those who are buying at these discount prices are making a good decision, as some junior exploration stocks go through the roof without so much as a single hole. A recent example is GGI - the stock ran from .08 to 5.27 currently trading 4.80 with no revenue and no cash in hand (yes, I know their outstanding is a fraction of ours …).

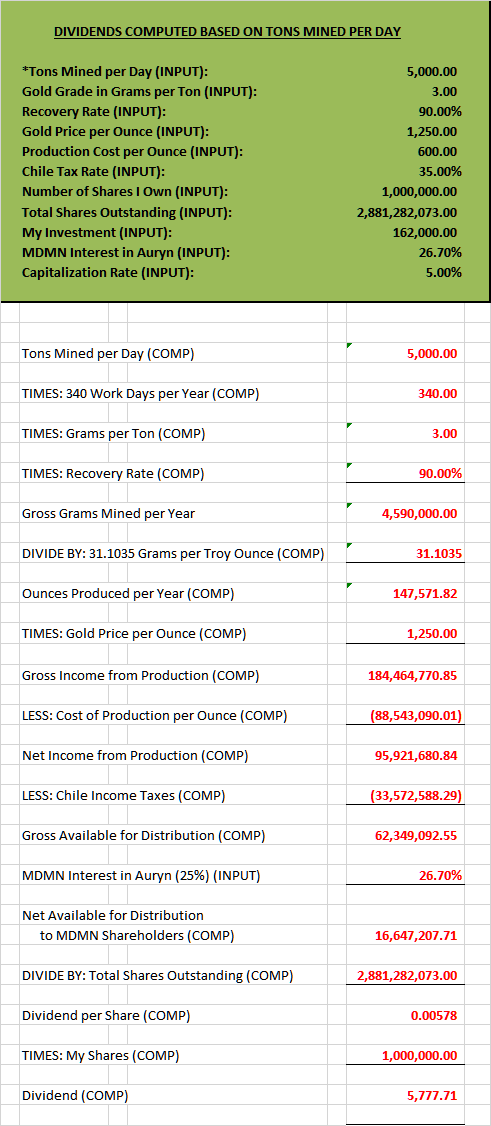

Can any of you GEOs help me with the following computation? Are there any steps I’m missing? I’m trying to get an idea as to how much income we could be generating at production of a specific number of tons per day in production.

Actually he stated, “We believe that we could begin to ramp up production in November.”

1 Like

3 grams per tonne is too low. They wouldn’t bother at the level. I think about 50 is probably a better number to plug in. Also, I believe the initial allowed mining rate is 5000 tons per MONTH.

Yeah, Taff, I have to chuckle. Why would we get off the roller coaster at this point…right? Why not ride it out, even if it’s to the bottom. I mean, what’s to lose other than our minds, which we clearly have already lost (speaking for myself). I can sit back and wait it out…and maybe, just maybe, it will pay off. As far as ‘investment’ goes, I think we’ve added yet a new meaning to the word in Webster’s which reads: “A challenge in Taff’s life (i.e., also know as Taff’s Law) that he took on and never gave up on because he - like many others - couldn’t discern the faint line separating obsession with persistence.”

4 Likes

Thanks very much!

Good point Fadein, about loosing our minds of course  .

.

2 Likes

Mike, If those are the numbers you think we’d be working with, we’d be netting about $50M/ yr. I have to think they’ve been working on much greater expanded permitting than 5,000 t/m (which is only for the Caren). I would think they have been working on permitting of some kind to get the Fortuna off the ground, also. So much depends on how this IPO rolls out. If Baldy is right and they have no institutional backers and just do a reverse into CDCH or something, it will take years to move this anywhere. If they go large with a traditional IPO, “presell” 50M “treasury” shares to banks and promoters at $1 share we’ll be off to the races. Preferred shares would retain control among the 100M current share structure.

Only if Auryn can answer these questions  we wouldn’t have to speculate anymore.

we wouldn’t have to speculate anymore.

Auryn’s own estimate is still shown on Slide 14 of their ADL presentation on their website: http://aurynmining.com/altos-de-lipangue/

There is an estimate there also for Fortuna: 19.5 g/t

However, if you look the grades given in the sampling of the various adits of the Caren (see slide 10 and their various PRs on grades), it’s clear you don’t get to the bonanza grades until you get 100m or 150m below ground. Above that it varies obviously but the surface grades on the Merlin1 were often between 1 g/t to 10 g/t in the far south. In other words, the bonanza grades are only available by underground mining. Mineable surface / open pit grades and amounts are still very undetermined and require more surface / drilling work to be sure.

In addition, the bonanza veins are narrow, in some places very narrow, even if they do cross the entire mountain. So the question becomes how much barren rock do you have to mine out to get that < 1m of bonanza grade ore? That has to do with how much money to you spend to get how much gold in return. Additionally it speaks to how fast you can mine ore tonnes on a low budget mine.

These things together make the picture a little undefined. Obviously Auryn still thinks underground mining the Caren is going to be profitable or they wouldn’t be working to put the thing into production as they again recently reiterated. But how easy it is and how long it is profitable is probably not certain to anyone yet.

I agree with MG in the long term. Copper is the game. But they have to define lots of copper tonnes and good copper grade before anyone cares. That requires money and time (multiple years). Gold mining is just a financing mechanism for that exploration with possible upside if they get lucky and find enough gold with grade within 100 - 150m of surface to support an open pit.

2 Likes

Good news for us both, doesn’t sound like we are alone

Looking at their last January update, they talk about a modeled grade of 15 grams/ton gold equivalent for the high grades veins. The bonanza grades veins they didn’t define. Presumably they will go after the bonanza grades first blasting upward from the Larissa tunnel(the production adit that directly connects to loading area outside) to the Level 2 adit. I seem to recall that they thought they could intersect the bonanza grades found in Level 2 in an extension of the Larissa tunnel. I would think that the construction of the chimneys was used to connect Level 2 with Larissa tunnel and hopefully they were able to better define the bonanza grades in the process. I suspect they have their hands full with just the Caren with the Fortuna, LDM to be worked on later.

To clarify my “rough estimate” using Mike’s "guesstimate I did a very quick back of the envelope with little or no basis on old numbers other than 5,000 tons per month permit averaging 50 grams per ton in Mike’s guessimate. It had little or nothing to do with the older conservative Bocanegra conservative report on sampling (slide 14) prior to the Larissa adit and work presently under progress.

The math went like this: 12 months x 5,000 tons x 50 grams/tons = 3,000,000 grams in the 1st year, or 97 K OZ AU. Assuming about $600 per OZ net for this high grade quick production is where my “magical” $50M/ yr for 1st full year exploitation came from. (figures edited thanks to JDS) It is a simple WAG based on far less than is actually known.

If bulk sampling permits have been obtained for a few of the higher 10g/ton surface areas sampled on the Fortuna are obtained and a crusher and Falcon gravimetric system are used in the next couple of years, where would that put this? The Falcon concentrates 100 fold when properly processed, very economical to transport to ENAMI for final processing. Consider this nothing more than a WAG, and don’t base anything on what I have said here in the way of speculative investment advice or anything more than a pipedream that keeps me happy on my current paper loss. Thanks for letting my dreams entertain a few here. It is not even close to what was being presented in early 2016 before we ran into some very major setbacks on many fronts that are only now being slowly resolved. If things progress sucessfully, I expect there will be open pit areas with onsite processing of the lower grade ore areas.

recall:

“We have conducted metallurgical test runs at recognized laboratories in Chile and Peru. These have resulted in an average gold recovery of over 90% from concentrated ore obtained by a gravimetric Falcon system. Based on this, AURYN expects to produce a total of 5,000 troy ounces of gold in 2016 and over 25,000 troy ounces in 2017.”

Acquisition of Altos de Lipangue Mining Claims | AURYN Mining Corporation

All the big money, if it ever comes to fruition is based on what are believed to be the vast deposits of copper that may be contained beneath the ADL that have not yet been defined in any acceptable fashion. As CHG stated, “That requires money and time (multiple years).” Any near term gold production is the major financing mechanism for work to continue, and apparently that has been AURYN’s plan for quite some time.

My daydream that has been dismissed here repeatedly is just that , but has been stated before and goes something like this:

The number and price of free trading IPO shares would be priced by an Investment Bank, which I’m sure AURYN has contacts with. Ideally, dividends or a buyout of Medinah’s and Cerro’s shares would occur well after AURYN becomes fully reporting and climbs from the OTCQB tier and moves to the OTCQX tier sometime later. Once on the OTCQX they would automatically have access to the international markets which I believe is AURYN’s eventual goal. AURYN is cautious, methodical and plans carefully for long-term success, IMO.

Alternatively, under a similar arrangement, the share structure is kept at the original 100M shares (keeping it simple – 70% AURYN, 30% MDMN and CDCH. As an example, after determining a valuation for the assets of the company, an offer of 50M shares for the initial public offering of only treasury shares that are created and sold could be made to various institutional and individual investors for $1 each. Immediate cash for accelerated exploitation and exploration.

Check your zeros and decimal points. should be 3,000,000 grams per year and 97,000 ounces.

Thanks JDS (I edited my post to reflect your correction) - misplaced commas thankfully still result in about $50M in 1st full year of production if $600 net per OZ AU and substantial very high gold content encountered in adits 3 through 2.

Why are we still at.005 ? incredible, if these numbers will be real, and that’s just a start and just the gold, imagine with the copper and all the other minerals.