So the property is tied up for 5 years until Dec. 12, 2023.

It would be nice to know what ‘expenses’ they’ve incurred on the property date. It’s been 28 months !

So the property is tied up for 5 years until Dec. 12, 2023.

It would be nice to know what ‘expenses’ they’ve incurred on the property date. It’s been 28 months !

Yes, but in the same (see December 2018 update link) Shareholder update it states, “We continue to work on the Larissa and Merlin claims and are finishing the chimneys and exit routes. Once approval has been given, we will make a new cut on level 3 to intercept the high-grade ore vein uncovered in a new tunnel found between levels 2 and 3. “

And

“… look forward to the possibilities for 2019, including advancement of the Hochschild JV, drilling activities on the mountain, and possible production from the Lampa / Lo Amarillo and Larissa / Merlin targets.”

I don’t think these goals have been abandoned, but from all appearance have been slowed down considerably. The announcement of some production from the Fortuna may allow some progress to be made towards production on the Larissa/Merlin targets. I’m always open to pleasant surprises being announced in future quarters. I’m not holding my breath, however, given the questions remaining to be answered on how/who is financing this.

Hi EZ,

I think that the development that might come out of left field for Medinah/Auryn shareholders will be related to the Pegaso Nero and its copper possibilities. Maurizio told us a long time ago that he envisioned multiple simultaneous JVs at the ADL but that he wanted to keep in house the high-grade gold possibilities. The last we heard about the PN, Freeport had given Maurizio permission to use their name as a potential partner of interest. Maurizio also stated that two majors “even larger than Freeport” had shown interest. Deals on a scale like that are extremely slow in getting put together but the recent move in the price of copper to 10-year highs and nearly all-time highs might expedite deal making on large projects like this. I see copper up 2% yesterday and yet another 1.7% this morning to $4.19 per pound. Here’s a link to a recent interview with the BHP President of minerals for the Americas:

I think we need to keep in mind just how desperate the majors are for new properties and Mineral Reserves/Mineral Resources (MR/MR) on their balance sheets. We are at a 32-year low in new mineral discoveries and a 31-year low in the number of ounces of MR/MR on the balance sheets of the majors. The DEMAND for new discoveries is thus huge but there’s no SUPPLY. With copper breaking out to the upside, the DEMAND will go up even more. The build out for all of this new Green New Deal-related increase in Electric Vehicles (EVs) and the need for charging stations to service them will result in the copper price continuing to take off. This in turn will augment the DEMAND for new copper discoveries at a time when the SUPPLY is next to nil. Deal making might be very rapid because each new deal results in a lower SUPPLY of discoveries.

The build out for large copper projects is so slow that the majors could miss out on a bull run in copper if they don’t hustle. I’m hoping that Auryn’s near-term gold successes will increase their bargaining position for the Pegaso Nero. Theoretically, Auryn might be able to self-fund some PN development in order to enhance the value of the property prior to doing a deal. At the informational meeting in Las Vegas, Maurizio conceded that the PN was too big for Auryn to attack. He threw out some numbers as to what the negotiations might look like for a deal at the PN and what it might take to acquire a 51% stake. These weren’t anything like the LDM numbers.

For the majors, having a large number of viable projects in the pipeline is not a good idea, it is existential. It’s all about timing. It now takes an estimated 26 years from the commencement of exploration efforts to putting a large discovery into production. The majors that have painted themselves into a corner with a lack of MR/MR don’t have time to do their own exploring. Fingers crossed!!!

"He threw out some numbers as to what the negotiations might look like for a deal at the PN and what it might take to acquire a 51% stake."

Brecciaboy, for those of us that were not there, can you try to remember and tell us what Maurizio said? The theoretical numbers and potential structure would be nice to know - at least what Maurizio might have had in mind at the time.

To add to mrbuba’s question about theoretical numbers at Pegaso Nero I couldn’t find any info about copper on Auryn’s website as it relates to the amount of copper at Pegaso Nero. Would someone be kind enough to point to a website that references the extent of copper at Pegaso Nero. Thanks !!

Throwing in my .2 cents  – if we start consistently pulling out 40 tons per day of 25+ grams AU per ton, I don’t think we are going to stay at $0.002 for long. Eventually word will spread that this little “ragtag group of miners” has a major discovery. The property is vast, the location is great, and this is not an isolated vein that just happens to be there with nothing else around it.

– if we start consistently pulling out 40 tons per day of 25+ grams AU per ton, I don’t think we are going to stay at $0.002 for long. Eventually word will spread that this little “ragtag group of miners” has a major discovery. The property is vast, the location is great, and this is not an isolated vein that just happens to be there with nothing else around it.

Definition drilling was never done to my knowledge so the best info would be a possible extrapolation of the area size x sample avg.

It takes a LOT of drilling even to define an INFERRED grade & tonnage.

Rod

Feb 3, 2016

February 03, 2016 @ 09:12

Highlights

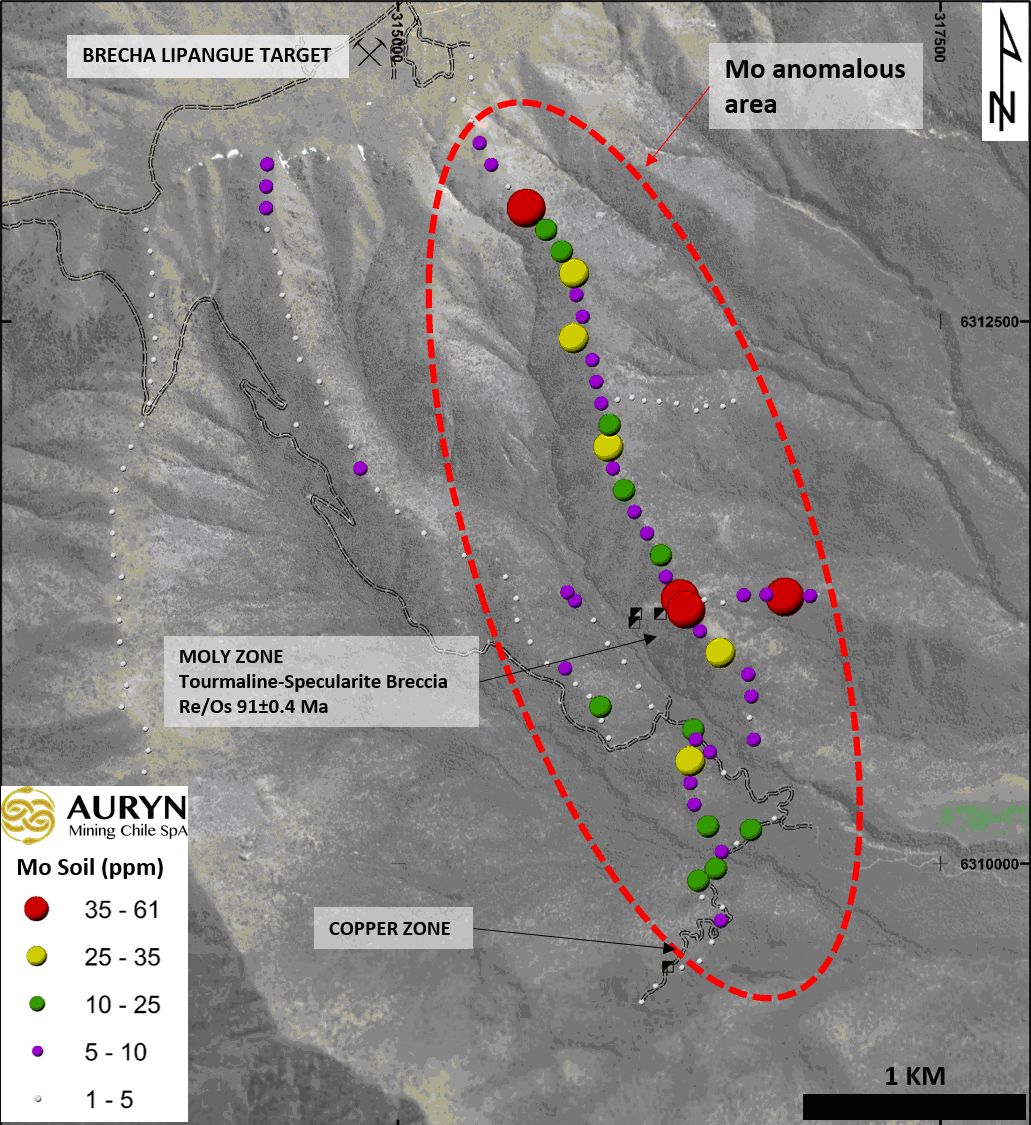

AURYN Mining Chile SpA (“AURYN” or “the Company” or “AMC”) is pleased to announce results from the first phase of soil geochemistry sampling program on the Pegaso Nero Moly-Copper area, located within the Altos de Lipangue project, in the Cretaceous-aged belt of central Chile.

The soil geochemistry program detected an important Mo – Cu anomaly surrounded by Pb, Zn and As anomalies. Inside the area containing high molybdenum values on soil samples, it was recognized a hydrothermal breccia with tourmaline – specularite and associated copper oxides.

Mineralization observed at Pegaso Nero target is related to a very well defined structural controlled alteration system that has only been partially explored by AURYN. This system hosts an important number of outcrops of hydrothermal tourmaline – specularite breccia with molybdenum, copper and gold mineralization.

A total of one hundred and thirty-six soil samples were completed at the Pegaso Nero prospect. A large molybdenum anomalous area was detected, with extension almost 3.6 by 1.2 kilometers and still open to the east. Moreover, there are two sectors with strong Cu-Mo mineralization identified to date within the molybdenum anomaly area, named the Moly Zone and the Copper Zone, where Copper is located 2 km south of the Moly zone. (See Figure1)

The previous rock sampling detected highly mineralized Mo-Cu±Au breccia, in this campaign the rock sampling was extended with preliminary results of 1.2% Cu, 860 ppm Mo and 0.12 g/t Au in the hydrothermal breccia.

Furthermore, one sample of molybdenite from the breccia was sent to the ALS laboratory in Quebec, Canada, for Re/Os dating, the result was 91 ± 0.4 Ma , which is the age of several known Copper, Gold and Molybdenum porphyry deposits in Chile, such as Andacollo, Dos Amigos, Johana and Frontera.

The extensive molybdenum anomaly, the presence of hydrothermal breccia, the high Copper – Molybdenum results on that breccia and the age of the mineralization, are showing to AURYN Mining Chile team that is in front of a new Porphyry Copper system and this new discovery is opening the cretaceous porphyry belt to the south of Llahuin and Andacollo porphyries on the IV region in Chile.

AURYN is planning for this summer, an extensive exploration program at the Pegaso Nero prospect, aimed at testing for extensions to the anomalies, which will include systematic additional geochemical sampling in the known prospects, reconnaissance of the surrounding areas and IP lines to detect undergrown distribution.

Figure 1: Soil sampling results at Pegaso Nero target.

Thanks Rod, much appreciated !!! With molybdenum selling for about 3x the price of copper this porphyry system may just be worth a few bucks.

Rod,

Thanks for showing the image of where Auryn grabbed and analyzed 136 samples. Here’s an image of what that same area of the PN looked like earlier this year.

Hi MrB,

Basically Maurizio laid out a hypothetical. He said let’s say that a major offers us $40 million for a one-fourth stake in the PN. Then let’s say that they have good results and want to acquire a bigger %. The next quarter would obviously cost them a lot more since the risk has been mitigated quite a it. He mentioned that they would probably want to acquire 51% but that they wouldn’t be successful in that endeavor. My take away was that Maurizio wanted to maintain control of the PN. He was pretty clear that the PN was too big for Auryn/Medinah to solo develop.

He was apparently given permission to use Freeport McMoRan’s name as a party of interest but he mentioned that there were two “even larger” majors that had shown interest but he didn’t have permission to use their names. He was very clear in stating that there were no guarantees that any of these 3 would ink a deal. With the price of copper breaking out to the upside, I can only intuit that interest levels in an asset like this would increase. He was very professional in connoting the fact that this industry is not meant for widows and orphans. It’s very risky and it takes forever to develop a property. He even asked that anybody present that intended on disseminating the information presented at this “informational meeting” would please attach a copy of their “boilerplate” statement addressing risks in this sector and forward looking statements.

For me, the key takeaway was the implied enormous size of this asset. 3.6 Km (north to south) by 1.2 Km (east to west) is a very large sampling space. This is especially true when the hyperspectral satellite imaging survey depicted a 7 Km swath of east to west oriented alteration indicating “about a dozen” intrusives.

Is there anyone here with “overlay skills” who is willing to apply them to the image easymillion has supplied above, overlaying it with an approximate outline of the area brecciaboy has described?

– madmen

For me, the exciting part of the PN story is the implied size. The plateau is located at 2,000 meters in elevation. The north-south extent of this copper-moly zone is 3,600 meters down the southern downslope off of the plateau. This has to be getting close to sea level dependent upon the angle of the southern downslope off of the plateau. The 136 separate samples represent a lot of sampling on this particular ridge crest. These grades were found right at SURFACE. These aren’t trenching results or drill hole results. On a ridge crest, the surface soil is usually gone due to erosion from rain and snow melt. The bedrock can be found right at surface.

High copper and moly grades found at surface at very low elevation levels speaks to potential ECONOMICS and year-round mining if the grades hold up. The tourmaline-specularite breccias present there are interesting because just east of us up high in the Andes is the massive Rio Blanco-Los Bronces tourmaline breccia deposit. It features 15 monster breccias. “Breccias” suggest very high levels of explosivity which is a good thing. When the ore-bearing super-hot hydrothermal fluids and gases exsolve out of a magma chamber there can be a lot of crash, boom, bang. These breccias tend to occur in clusters of breccias. Just offshore from the ADL at the same latitude as Los Bronces, lies the San Fernandez Ridge. Geoscientists feel that the subduction of this ridge under the South American Continental Plate is responsible for the massive Los Bronces tourmaline-specularite breccias to the east of the ADL. The theory is that it’s the angle of the subducting tectonic plate that favored massive copper deposit formation in this area and at this latitude. Just north of the PN tourmaline-specularite breccia is our “Gordon breccia”. In the words of Auryn’s geoscientist, Luciano Bocanegra, the Gordon bx “vectors towards” the PN potential deposit. He’s written extensively on the “vectoring” process in geology.

This area needs a ton of exploration/development work but especially from a potential size and proximity to surface point of view, the preliminary results are more than exciting. Don Singer did a huge study including pretty much every known porphyry deposit known to man. The copper-moly type of porphyry deposit, along with its associated breccias and skarns, are not only the behemoths of these already elephantine-sized deposits they are also the ones found closest to the surface. Maurizio’s friend, Dick Sillitoe, authored a study back in I believe it was 1974, showing that the very top of the average porphyry deposit is buried in between 1.5 and 4 Km below the current surface. At the PN, we have good grades of both copper and moly right at surface. Over the years, a lot of geologists have visited the ADL while working with Medinah, Nuoco and Auryn. One made the comment that he had only seen the types of copper and moly grades found right at surface at the PN in some of the famous deposits found in Colorado like the Henderson deposit. Moly is pretty much only mined from copper-moly porphyries.

The 91 million year age of the PN’s tourmaline-specularite breccia derived from RE-Os dating which matches that of the famous Andacollo deposit to the north of the ADL near La Serena is very, very interesting. This is a copper-gold porphyry deposit that has striking similarities to the ADL. The gold grades are too high at both areas to fit the models. You’ve got a centralized porphyry area with high grade gold emanating out 5 Km from the porphyry area.

Here is a link to some articles on the Donoso tourmaline breccia to our east at Los Bronces and other tourmaline breccia deposits.

http://geode.colorado.edu/~skewes/pdf/skewes_holmgren_stern2003.pdf

https://biblioteca.sernageomin.cl/opac/DataFiles/KingR_et_al.pdf

Great reads, all… thanks for the continued insights. Now here’s my “wake up sweating in the middle of the night” question that’s been dogging me for years:

“Is the ADL potentially TOO close to Santiago for an open pit copper / moly play?”

I can see the underground gold mining playing out, but the porphyry itself I have questions and concerns on the permitting.

$0.002 for your thoughts…

A Great Question…

Baldy;

I was looking up info on the Preferred Shares & found the post below. I don’t quite understand the bolded part. Any explanation you can give me ?

Thanks,

Rod

P.S. I assume that these 5,000 preferred shares (once held by the Day brothers) are now the ones that are held by AURYN Holdings -Maurizio Cordova (was 500,000 before share consolidation) . Do you know if that’s correct ?

Baldy – Dec 28, 2015

A portion of a response to my questions directed to the Days re: CDCH. FYI

"The terms of the 500,000 preferred shares are such that one share is entitled to 1,000 votes and is convertible at a rate of 1 to 100. However, all conversions shall be effectuated at a purchase price of $.10 per share (i.e. the conversion of 1 share of preferred into 100 shares of common would cost the individual completing the conversion $10). In the event that the market price of the CDCH shares is above $.10, the conversion may be completed on a cashless basis.

Hi Rod.

The cashless exerciese simply means that they don’t have to put up any money to secure the shares. Unlike a warrant or option where, in most instances, you have pay to exercise or convert the shares. This brings money into the company treasury.

As it relates to the status of the preferrreds or any insight, generallly, into the cap structure of AUMC or MDMN, I have no clue. This was one of the primary reasons why I exited both positions.

We can all get excited about what may or may not be happening on the mountain BUT, investing in anything where you don’t know what you own (how many shares outstanding, accrued liabilities, dilution, etc) is worse than placing it all on red (where you at least have a 47.4% change of being right).

The preferred shares are clearly documented in the annual disclosure documents found on the OTC website.

500,000 preferred shares were issued:

In early 2017, Auryn announced a cash call, which based upon the Company’s 5% holdings, required a further investment of $300,000 in order to maintain the Company’s 5% holdings in Auryn. At the Company’s Annual Shareholder Meeting, held on June 5, 2017, the Company approved an offer from Auryn Holding Corp (“Auryn Holding”), a separate but related entity to Auryn, to loan funds to the Company for purposes of satisfying Auryn’s cash call, in the amount of $300,000, pursuant to a no-interest loan, and in consideration of such loan, 500,000 shares of preferred voting stock of Cerro, which carry with them 1000-for-1 voting rights, would be delivered to Auryn Holding, and new management would be appointed: Raul Del Solar and Gary Goodin as directors. As of July 2017, George Young resigned as a director in preparation for the management change, and Jose Manuel Borquez Yunga gave notice of his pending resignation, subject to the closing of the loan and related terms with Auryn Holding, including the appointment of new management as set forth above (the “Closing”). Such resignation was effective November 10, 2017, the date of the Closing, resulting in a change of control of the Company…On August 13, 2018, FINRA approved the name change of the Company to AURYN Mining Corporation, as well as a 1 for 100 reverse stock split of the Company’s authorized shares and its issued and outstanding shares.

When the 100:1 reverse split was done these became 5000 preferred shares. They continue to be in the hands of Auryn Holdings (Maurizio Cordova) as documented in several tables in the Disclosure document. See the table in Section 7 for example: where it is disclosed Auryn Holdings holds 100% of the existing 5000 preferred shares which carry 1000:1 voting rights.

Otherwise, Marizio owns 26.46M common shares or 38% of the total 70M. Amparo Quijano Claro owns another 16M or 23%, nearly the same amount as what Medinah owns. These three shareholders (M, A, and MDMN) account for 85% of the common shares.

So, if my math in my head is correct, I own over 5% with 4.3M shares (today’s value is $11,500). This can’t be right - I’m sure there are regulars on here that own way more shares than me.

You’re referring to MDMN. Cornhusker is referring to AUMC.

All these 4 letter words!