October 2024 – Shareholder Update

Oct 22, 2024

AURYN Mining Corporation Shareholder Update

AURYN Mining Corporation (OTC: AUMC) is committed to keeping our shareholders informed with the most current updates on our progress and strategic initiatives. As we step into the third quarter of 2024, we wish to share significant developments and our forward-looking approach to our mining and exploration activities.

Fortuna Operations

During this quarter, our operations at the Fortuna site have made considerable progress:

- Mining Camp Construction: The construction of our new mining camp at Fortuna is currently 60% complete, and we expect to finalize it within the next three weeks.

- Antonino Tunnel Operations: Our focus has been on preparing the Antonino Tunnel for optimal production and accumulating ore for future processing.

Mining Plan Developments

Our team has submitted a renewal application for our exploitation permit to the Chilean Mining Authority (SERNAGEOMIN) under the Small Mining Producers statute, allowing an exploitation rate of up to 1,000 tons per month – adequate for operations at Antonino. In parallel, our exploration team is identifying additional areas for future extraction to ensure simultaneous monthly ore production comparable to Antonino, thus creating a stable supply to support our Flotation Plant operations.

To further understand the potential of our site, our team is planning a comprehensive exploration effort. This will involve correlating data with nearby mining districts such as BRONCE PETORCA (to the north) and LA FLORIDA (to the south), specifically targeting regions at 1,550 meters below the Antonino level.

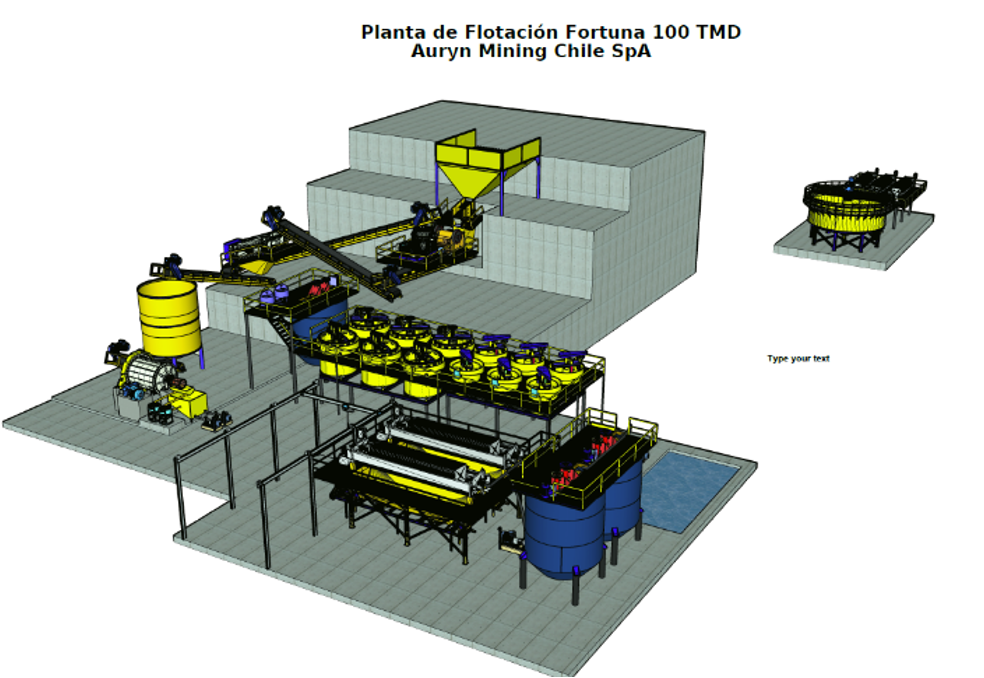

Flotation Plant Developments

We are making substantial progress in the development of our flotation plant, which will have a processing capacity of 100 tons per day. Current developments include:

- Topography: A detailed topographic survey covering 1 km² has been completed for the planned location of the flotation plant.

- Hydrogeology: Hydrogeological studies indicate access to at least 1 liter/second of water, which is twice the amount needed for operations. The region’s Mediterranean climate supports natural aquifer recharge.

- Energy Supply: We are negotiating with an energy provider to ensure a sustainable energy supply, prioritizing renewable sources at a cost below the regional average.

- Water Management: A 100% water recirculation system will be implemented to minimize consumption, with an estimated recovery efficiency of 80%, considering losses due to evaporation.

- Technical File: The technical dossier for obtaining the necessary permits is nearing completion, ensuring compliance with all legal and technical requirements.

- Equipment Procurement: Initial orders have been placed for key equipment, including crushers and a mill, to ensure timely delivery.

- Geochemical Laboratory: The necessary equipment has been selected to establish an on-site geochemical laboratory, which will be operational before year-end. This lab will facilitate same-day analyses, crucial for exploration and future production control.

Based on our progress, we anticipate that the flotation plant will be operational with all necessary permits by the third quarter of 2025.

Collaborating with Universities

AURYN continues its partnership with the University of San Sebastian. During this quarter, we are launching new research projects, including developing a regulatory requirements matrix for operations at Lipangue to create a quality control system for small-scale mining producers. We are also advancing the conceptual development of a low-cost filtering and utilization system for water from the Antonino Tunnel.

Future Updates

For further details and to stay up-to-date with AURYN Mining Corporation’s activities, please visit our website and subscribe to email notifications.