Starting off an active year!

The mountain is buzzing…

11 Likes

Happy New Year folks!

It looks like 2026 may actually be the year Auryn/Medinah finally achieves some form of production. To what extent that long-anticipated and oft-misunderstood/miscalculated milestone impacts the value of the severely diluted positions of shareholders will be…um…interesting.

Regardless, the debate on this board in the coming months will be very fascinating.

13 Likes

Fascinating is an understatement, but welcome back.

3 Likes

Hi Cabezon and HR,

Happy New Year to all of the Auryn/Medinah shareholders. In reading the content of the TMP investment forum over the last several months, I think the one concept that isn’t getting enough play is what the transitioning to becoming a “GOLD PRODUCER” really means in the overall scheme of things in this particular sector. In a nutshell, it is everything. There is no event in the corporate development of a junior miner with anywhere near as much importance as successfully transitioning into PRODUCTION. With the price of gold so strong, in this sector right now, you’re either a GOLD PRODUCER that can DIRECTLY access these high gold prices or you’re not. A junior explorer/developer that’s busy trying to raise money in order to commence Phase 1 of a 3 phase diamond drilling campaign is, by definition , at least several years away from PRODUCTION and the ability to DIRECTLY access the past incremental increases in the price of gold. The upwards move in the price of gold has already occurred. It’s not like these juniors need to hope and pray that the POG goes up in the future. The GOLD PRODUCERS are literally printing money right now.

A lot of the share prices and market caps of the GOLD PRODUCERS have already tripled or quadrupled. What opportunists like me are currently looking for are the “ABOUT TO BECOME PRODUCERS”, like an “Auryn/Medinah”, whose share price is currently stagnant, and that nobody has ever heard of before. The shareholders of Auryn/Medinah have been through a lot, but at least they have obtained a front row seat in a junior miner transitioning into PRODUCTION. I feel like the upcoming share price reaction to Auryn going into production is extremely PREDICTABLE. In the industry, it’s referred to as a “MARKET RE-RATE”, and it is the norm.

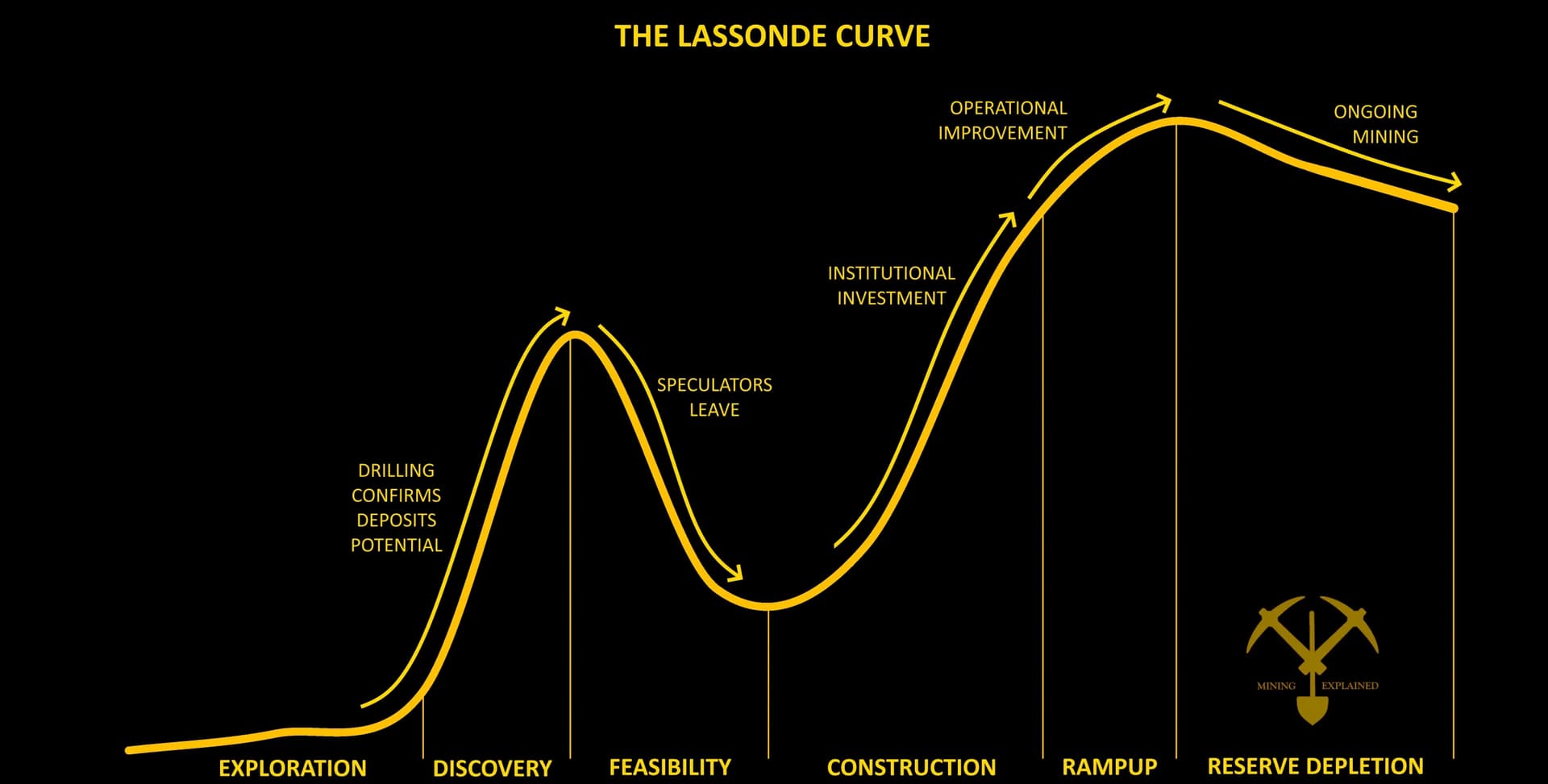

“THE LASSONDE CURVE” is the result of the careful study of the share price patterns of the junior explorers/developers that,throughout history, were fortunate enough to make it into PRODUCTION. It clearly shows how the share prices of the “JUNIOR PRODUCERS” tend to go nuts as they transitioned from the “CONSTRUCTION PHASE” into PRODUCTION. This occurred when gold was trading at “AVERAGE LEVELS” throughout history. We don’t have a graph of the share price performance of the new “JUNIOR GOLD PRODUCERS” that just so happened to go into PRODUCTION when the prices of the 3 metals they were producing (gold, copper, and silver) were ALL trading at or near their ALL-TIME highs. We’re in uncharted waters in this respect. Nor do we have historical graphs depicting the share price performance of young “JUNIOR GOLD PRODUCERS” that went into production with only 70 million shares issue and outstanding and a “float” of less than 10 million shares. Again, we’re in uncharted waters in this regard. Don’t forget also that Auryn has maintained their 100% ownership of the entire ADL Mining District. “PERCENTAGE OWNERSHIP DILUTION” is that other form of “DILUTION” that investors need to worry about in addition to share structure “DILUTION”.

The de minimis “float” of readily sellable securities suggest to me that when the expected “MARKET RE-RATING” does occur, it might happen very quickly for Auryn/Medinah. The lack of a “float” of readily sellable securities in the past, has actually, believe it or not, been a net negative for Auryn. Those aware of an upcoming “MARKET RE-RATING”, that wanted to establish a meaningful “long position” in Auryn, couldn’t do so without chasing the share price upwards BEFORE THE RE-RATING WAS EARNED. Once PRODUCTION commences, then it’s a fairly straightforward process, with some guidance provided by management, to calculate an appropriate share price/market cap based on things like EARNINGS PER SHARE and average “EPS MULTIPLES”. VISIBILITY of an appropriate share price is a very good thing.

What I think shareholders and prospective investors alike will appreciate the most is the level of ENHANCED VISIBILITY provided by being in PRODUCTION. The junior mineral explorers/developers are notoriously difficult to value prior to being in PRODUCTION. All they ever seem to do is spend money and dilute their share structures and percentage ownership to death. I think the most important financial metrics for the JUNIOR PRODUCERS is how many shares did you have issued and outstanding and in your “float” on the first day of PRODUCTION. This is what is going to determine the all-important EARNINGS PER SHARE and the magnitude of your “MARKET RE-RATE”.

Recall two of the salient statistics provided by the World Gold Council. The first is that only about 1-in-1,000 mineral prospects will ever be put into PRODUCTION. The GOLD PRODUCERS represent a very exclusive “fraternity”. The second statistic is that for the owner of that lucky 1-in-1,000 corporation, it now takes an average of in between 17 and 24 years from the commencement of exploration efforts to the first day of production. You can now appreciate why a healthy “MARKET RE-RATE” is the norm for the new JUNIOR GOLD PRODUCERS that have already conquered those odds and spent that time. The “barriers to entry” into the GOLD PRODUCERS fraternity is significant and the “MARKET RE-RATE” is proportionate to the “barriers to entry”.

One of the junior miner analysts that is posting the best results for investment recommendations is “Lobo Tiggre”. If you go to the 29-minute mark of the recent interview linked to below, by Kitco News, you’ll hear him explain the “SUBSTANTIAL RE-RATES” associated with finding a junior miner in the “PRE-PRODUCTION SWEETSPOT” (having entered into the “construction phase”) and the importance of understanding “THE LASSONDE CURVE”. He stresses how “PREDICTABLE” this “MARKET RE-RATE” is in an otherwise very complex industry. Rick Rule recently did a joint interview with Lobo and he too agreed with Lobo’s obsession with finding juniors just when they enter into the pre-production “construction phase”, again because of the “PREDICTABILITY” of a significant “MARKET RE-RATE”. Again, Happy New Year to all.

8 Likes

Here’s a summary of what is about to take place on-site:

THE COMMISSIONING OF A FROTH FLOTATION PLANT

AI Overview

Froth Flotation Process - 911Metallurgist

Commissioning a froth flotation plant involves detailed planning, mechanical installation (ensuring level tanks and aligned components), pre-operational checks, and phased startup with careful reagent tuning, water balance, and performance monitoring, moving from test runs to full production to optimize recovery and concentrate quality by adjusting pulp density, pH, and chemical dosages for the specific ore.

-

Preparation & Installation

Site Prep: Clear land, build foundations, install buildings, and deliver machinery.

Mechanical Setup: Install tanks sequentially (head, middle, tail), ensuring they are perfectly level and aligned using surveying tools. Install stirring/scraping mechanisms, piping, and electrical systems.

Equipment Checks: Verify all components, including pumps, motors, and control systems, are installed correctly and functioning. -

Pre-Commissioning & Dry Testing

System Flushing: Flush tanks and lines with water to remove debris.

Mechanical Tests: Run agitators, scrapers, and pumps without pulp to check for vibration, noise, and proper operation.

Control Systems: Test level controls, flow meters, and automated systems. -

Wet Commissioning (Phased Startup)

Water Balance: Introduce water to achieve correct pulp density and flow rates.

Pulp Introduction (Test Feed): Start with a known, representative ore feed, possibly from a grinding circuit, at controlled flow rates.

Chemical Dosing: Introduce reagents (frothers, collectors, pH modifiers) incrementally, starting conservatively.

Start Flotation: Run the circuit, observing bubble formation, froth characteristics, and concentrate/tailings quality. -

Optimization & Performance Tuning

Adjust Parameters: Fine-tune pulp density, pH, reagent dosages (collectors, frothers, activators like CuSO4), and air flow.

Monitor & Analyze: Use microscopy and lab analysis to examine pulp, concentrate, and tailings for mineral recovery and grade.

Optimize Circuit: Adjust cell configurations (e.g., rougher, cleaner stages) and contact times for maximum efficiency.

Gradual Increase: Slowly ramp up feed rates from test levels (e.g., 3-5 kg/hr for pilot) to designed capacity (e.g., 750 tonnes/hr). -

Final Handover & Training

Documentation: Finalize operating manuals, P&IDs, and maintenance procedures.

Operator Training: Train staff on routine operations, troubleshooting, and safety protocols.

8 Likes

I think we’re due a 4th Quarter update from management - will be interesting to see what THEY have to say!

5 Likes

The Lassonde Curve has proven to be one of the stalwarts when it comes to investing in miners. Its pretty intuitive but equally reliable. As the chart indicates, the share prices of mining co’s start to take off during the construction phase. I’ve referenced PPX on this board, only for the sake of comparing a company at a very similar stage of development. It has followed the Lassonde Curve pretty well, appreciateing in price 7-10x as they knock on the door of completing construction of their 350tpd CIL.

AUMC has not followed the curve. Some may argue this is because the company is not actively “marketing” but, candidly, that’s just BS. Maurizio and his team are at all of the same conferences, meeting with all of the same investors, etc, etc. I would argue that the stagnant performance is tied to the anomaly of AUMC and its road to production.

Yes, for those who significantly added to their position post the massive dilutive event and reverse stock split a decade ago, AUMC has a very tight float (amazing what reverse splits can do) and yes, the ownership and float is extremely tight (because Maurizio owns most of the company). Having 70M shares outstanding is somewhat unique, as was the journey to get to this point. The anomaly is pretty clear. The reason why it can take 17 to 24 years to reach production is because most miners follow the Lassonde Curve>> Exploration, Discovery, Feasability, and then Construction. The reason why AUMC is not applicable to the Lassonde Curve is b/c it skipped all of the usual steps pre-construction.

For this reason I find it very odd that anyone uses this industry standard benchmark when it comes to analyzing AUMC. Its also the reason why AUMC’s share price hasn’t followed that trajectory nor will it fall into any of the other comparative buckets when it comes to valuation (P/Es, etc.) . I’m not bringing this up to be negative, quite the opposite.

AUMC broke many molds to get to this point and I’m eager to see Maurizio bring this project into production so that the conversation on this board can be rooted in empirical results vs ridiculous speculation. Having only 70M shares outstanding should be advantageous for those who averaged down to offset the dilution. However, its VERY important to understand that any reference to the Lassonde Curve, or 1-1000, or P/Es of 30x will have no utility when it comes to predicting price targets. You don’t get to follow the Lassonde Curve by cutting to the front of the line. AUMC also won’t attract “institutional investment”, a critical variable post construction, until disclosure/transparency and proper financial accounting are addressed. Food for thought.

This bootstrap operation is not a typical operation. Annotations on the lassonde curve are highly subjective.

3 Likes

We are in 100% agreement (worth noting given the rarity of this phenomenon).

1 Like

The publishing of financial statements by the company will have very minimal effect on institutional investment, the main reason being there will be no resourse or reserves reported. Liabilities will be relatively minimal and will be under control cash flow-wise. People who want to know the liabilities can consult the latest financials anyway. The company has no mineral resource or reserves, in accordance with either Canadian or US standards, and they will not for the foreseeable future, precisely because they have not drilled one thousand holes. They will therefore not report them ….. unless and until a major gets involved with the PGN and proves it out via drilling. Get that …*. MDMN/AUMC are an anomoly. Payment of dividends will attract retail investors, to a point - institutional investors, who generally require resources/reserves, in my opinion will stay away, which is fine by me. Good, more for me.

1 Like

I agree with what you are saying mrbubba, except for one very minor detail. They have done some drilling, much more than was reported in this AI summary shown below, but the major points summarized are all about the future. MDMN/AUMC is indeed a nonstandard anomaly, will not have MREs and reserves to report, and will run on their reported free cash flow (FCF) as they run pay dirt through the mill. PPS will run higher because of the points you and many other Shareholders so soundly pointed to. I pay little attention to non shareholders and those merely living in the past:

AI SUMMARY:

• Mineralization Intersected: Medinah successfully intersected mineralized breccia in 14 out of 18 holes drilled in the Gordon Breccia target.

• High-Grade Intervals: Notable individual drill hole results from that period included:

◦ Hole L99-08: 6.49 g/t Au (gold), 39.1 g/t Ag (silver), and 0.63% Cu (copper) across a 32 m core length.

◦ Hole L00-12: 2.23 g/t Au, 16.16 g/t Ag, and 0.55% Cu across a 25 m core length.

Expansion Potential: Later exploration work by partner AURYN Mining Chile, SpA (who optioned the property in 2014) uncovered “bonanza” gold grades and evidence of larger copper and gold porphyry structures, suggesting a much larger mineralized system than initially defined by the early drilling.

EZ

5 Likes

Here’s a crazy thought. Since the pps of AUMC is most likely going to affect the ratio of the AUMC shares distribution to MDMN shareholders (since AUMC shares will likely be sold to pay off the remaining mdmn debt) MC probably would want to be promoting the estimated value of the stockpile. If he ends up not doing that before the shares need to be liquidated, chalk up another W for Baldy. Sad but true. Lets hope the stockpile is NOT 95% barren rock and MC actually does what a responsible owner of a publicly traded company should do, which is to promote the value of the assets to the benefit of the shareholder base!

Novel concept right?

2 Likes

Ummm ……. there are regulations as to what you can put on financial statements. You need to learn that they exist, obviously you do not know that. You might be surprised to know that I’ve worked on the financials of at least one of the majors whose name has been bandied about here. FYI - Institutions are very unlikely to invest in a company that does not list actual reserves - they could be sued for negligence. You need to get it through your thick skull that this is an anomalous investment - they have not and will not drill 1,000 holes to make you (and few other ding-dongs) happy. Other portions of the property could be drilled pursuant to a JV later on, but not these veins. Don’t need it - we KNOW where these veins are and where they go. Learn it, live it.

MC is spending all this money ….. and for exactly WHAT do you think? A vacation property or something? HEADLINE NEWS: MC is gonna exploit this property (these veins) for gold ….. and silver (becoming more and more relevant, by the day) …… and copper. MC is smarter than you ….. by a LONG shot. Embrace the suck - you were exactly WRONG that these people could not do it on their own and that it will never pay dividends (uttered as recently as 10/23/2025). The sane people around here won’t forget - and the reason is ……. you made yourself somewhat ……. unforgettable.

Despite what you say, somehow, some way, Luciano Bocanegro, did a “preliminary resource estimate” using all of the historical data available and his own sampling efforts. He reported 866,000 ounces of gold IN JUST THE TOP PORTIONS OF THE MERLIN 1 VEIN (CAREN MINE) AND THE DL2 VEIN. This guy knows his stuff, he worked on a nearby mine with similar geology. But, you know better, right? I guess you think he’s just stupid too, right?

Auryn’s own rather exhaustive trenching program identified over 5,000 lineal-meters of veins that made it all of the way to the surface. Auryn knows exactly where these veins are located and THEY’RE ALL NAMED.

I trust MC has a plan to publish Auryn’s production in such a manner that retail investors (I know a few I can spread the word to) will move in and make the share price rise. Won’t take that much. Connect the dots. That will happen, because MC does not want to screw HIMSELF - and the suggestion by somebody that he would not do so because he can just rely on his ownership interest in the end of Auryn is just plain …… IDIOTIC.

I know, you would like for us all to simply relinquish investments because we do not deserve to be able to receive dividends when 1,000 holes have not been drilled, as it’s just not fair. Ain’t gonna happen.

Have a nice day.

6 Likes

Bubbles. This is exactly the point I’m making. AUMC is an anomaly and any attempt to refer to the Lassonde Curve or sector valuation benchmarks is a fool’s errand. You and I are in complete agreement. To be clear, resources/reserves are not part of the financials that we are discusing. When I say that Maurizio needs to provide transparency to attract institutional investors I’m pointing towards full diclosure of laibilities. You don’t even know the terms of the debt financing and then there’s a massive, off balance sheet, liability to a related party. To become investable, AUMC needs to provide the details of these types of items, amongst many other. You may be comfortable, holding onto a retail dominated penny stock for the next decade but I can assure you the majority of folks around here would prefer to graduate, uplist, and morph into a legitimate company.

Its pretty clear that you are placing all of your marbles on the hope that dividends will come to save the day. Nothing else matters. That is your perrogative but, I can assure you, Maurizio is planning to allocate any and all profits (assuming they occur) back into the mountain. This is how micro cap miners grow into small to medium size producers. You simply can’t expect the market cap to grow to $250m+ on a continous boot strap, chase the vein operation. I would encourage you to consider a “fall back plan,” an alternate analysis of your investment if the dividends don’t magically appear. There are benefits to building a plant and then defining a resource. There are also major drawbacks, primarily around risk metrics. Maurizio is looking to build a legitimate company. He does not want to wither away in penny stock land with a bunch of elderly stock speculators.

Again, you seem to be very emotional and defensive of this investment. Your posts and the points you are attempting to make are becoming increasingly garbled and difficult to follow. I’m simply encouraging you to consider the potential, however large or small, that AUMC may not become the only micro cap mining co in the hisotry of micro cap mining co’s that decides NOT to pursue a dividend strategy to appease the fractional owners of said company.

In lieu of massive dividends, AUMC will need to pursue the boring old tactics of all of the other publicly traded companies (transparency, full reporting of financials, quarterly earnings calls, exploration, defining resources, etc.) if shareholders are looking for a respectable return on their investment.

You are currently invested in a $100 million market cap company that is doing NONE of the above. This is not sustainable over the long-term. Predictiions of a “3 to 5 bagger” imply a company trading at a half a billion dollars. Spend some time reviewing company’s supporting that valuation and what is expected of them from a reporting, disclosure, and financial guidance standpoint. A flurry of pictures on Twitter doesn’t cut it.

While you may not understand this reality, Maurizio does (although he seems to be very slow in moving in the right direction. This would/should be a good thing and I assume this will fall into place once production begins. If not, there will be issues. Grades, ASIC, profits/loss, ounces produced, attempts at forward guidance, are all necessary not “nice to have.”

Alternatively he may lean on you to “spread the word to some of your retail investors” to move the share price. Wait, wasn’t that the strategy of the past two decades??

1 Like

I do not expect MC to distribute all income to shareholders - I fully expect him to hold some back for expansion.

But, pull out your crayons and draw a picture of this:

Consistent Production > Consistent dividends > Share Price Appreciation > Easier to get loans for expansion.

It will happen.

It’s not hard.

I do not expect MC to distribute all income to shareholders - I fully expect him to hold some back for expansion.

But, you said there will NEVER be dividends.

4 Likes

Get aboard the other train, lol. While most posts on TMP (overall) adhered to known facts, statements made here in the past 24-48 hours are head spinning. Authors of previous statements not only denied the possibility of dividends, but also slammed MC, his motives and the decisions he makes.

Compared to the usual negative spins, now I’m hearing different tunes & opinions about Auryn to the positive side — perspectives rarely shared in the past. That can only mean all those reasonable opinions based on extensive knowledge of the mining world were on the right track all along.

3 Likes

Yes, AUMC is very thinly traded, but this chart looks like a winner - and there are actual events backing it up:

1 Like

You are right about the chart.

I don’t hold any AURYN shares at the moment, and have thought about accumulating over the past year or less.

I knew that the committed believers would increase the stock price.

The reason I did not buy shares was that with previous ridiculous LOW volumes, a bid for 10,000 shares might get you 10-20 shares for a cost that was less than the commission. (a losing proposition)

I’ve invested in gold/silver shares, many that have tripled (or more) in value.

I could see the share price continue to rise on the current increase volume, but ~4,000 shares @$1.35 is only $5,400.

Once there are shares to buy, i.e. float of ~7,000 + 16,000 (converted shares) the $ traded amount should become at least 4-5 times as much. That is when you can make a decent amount on your purchase.

Jaded, I believe you may be subconsciously biased in the interpretation of your readings. The same folks who have been predicting imminent dividends for the past twenty years are simply reiterating those predictions.

Yes, yes, yes!!!

Dividend machine.

And by the way, this is what brecciaboy and the Les rumors have been saying for a LONG time, much to the consternation of some who desire a quick, thoughtless exit.

In February of 2016 Bubba was equally optimistic. I guess there isn’t a statute of limitations on “I told you so.” Back in those days the focus was on the Merlin, as BB described in November of 2015:

With big grades at Merlin 2-5 the NPV of the 15% stake is going to go parabolic. Who knows how many sets of Merlin Veins are up there in an area with that many hectares? If you consider the Fortuna Vein as Merlin 6 (the easternmost of the 6) we already know that there were 7 different vertical stages of development there over a 30 year period averaging 64 gpt gold.

While the focus has shifted to whatever new shiny object that could perpetuate the dialogue over the past decades, calls for immient dividends and hyperbolic grades has remained as a steady constant. The shifts came gradual with previous analysis, mine plans and untold riches swept under the carpet to make way for new shiny objects. No accountability, no explanations, but a continous pivot to prolong an investement thesis.

Fortunately, this time is different in that Maurzio has managed to slug his way into building a plant. While the capital structure, ownership percentages, and share prices are no longer recognziable to any of the legacy investors, AUMC is finally knocking on the door of small scale production and, with success, an opportunity to prove up the resource. Not surpisingly, instead of humble gratification of reaching this point, many can’t help but fall back on the same mindset that got them into this investment quagmire: “imminent dividends, I told you this was going to be easy, I told you we didn’t need to drill out a resource, management always delivers, etc, etc.” It’s almost as though twenty years of struggles, lost opportunity costs, and immeasurable financial losses never happened. And so, they cycle repeats.

However this time, the “story” will need to be supported by empirical results. I think its fair to assume that people are sick of predicting the grades of the mountain based on what a bunch of mules and artisenal miners dug out of rock 50 years ago. No, I don’t believe that a project of this scale can support dividends but I am hoping that the grades and cost structure allow for a gradual expansion of the resources through reinvestmet.

My primary focus would be on a successful commissioning of the plant and reaching profitablity without any major hiccups over the next six months. After reaching this point, managing/scaling the actual mining to ensure perpetual feedstock will be paramout. If the stockpile is meant to be a buffer there needs to be proper assaying to better understand grades. One can only hope that all of these steps, results and outcomes are properly disclosed to investors so that they can assess the value of their investment.

Production is the great equalizer. The skeptics were proven to be right so long ago that its beyond the bounds of relevancy. I wish Maurizio success and, for the sake of the faithful shareholders, nobody is interested in getting this far to learn that the Emperor has no clothes. With execution and a little luck there should be enough free cash flows to “drill baby drill” and gain a better understanding of this mythical mountain.

1 Like

No, but good try at deflecting. Note that I said “most” posts. And I wasn’t looking that far back, either. That said, anyone hoping for dividends from AUMC were right about that part. And there is a big difference between optimistic excitement, and malicious attacks, intolerance of others whose words you disagree with, or misleading info. Slanted opinions stated as if a fact can be unnerving, too.

I’m just saying I’m glad the persistent negativity appears to be over now, or at least diminishing (I hope). If so, congratulations with your newly appointed role on TMP. How refreshing to read objective posts without the bashings. And there are several very worthy contributors here who don’t imagine this a competition. Respect is a two-way street for each & every one of us. ![]()

5 Likes