THE PRIMARY GOAL OF ANY JUNIOR MINER IS TO NOT ONLY PUT A MINERAL PROSPECT INTO PRODUCTION BUT TO DO SO WITH AS FEW SHARES ISSUED AND OUTSTANDING AT THE TIME AS POSSIBLE

The goal is really pretty simple. If you get a project into production, the share price is going to get a nice bump upwards known as a “MARKET RE-RATE”. If you put a project into production when your number of shares outstanding is really tiny, then you’re going to get a really generous “MARKET RE-RATE”.

Is massive share structure dilution in the junior mining sector an inevitability or can it be circumvented under the right set of circumstances? It is true that most successful junior miners end up needing to massively damage their share structures by selling boatloads of shares in order to raise the money needed to fully drill out a deposit, execute a series of more and more in-depth studies known as a Preliminary Economic Assessment, a Pre-Feasibility study, a Bankable Feasibility Study, and then block out NI 43-101 compliant MINERAL RESERVES/MINERAL RESOURCES (MR/MR). All of this is often done, just to gain the attention of a major miner hopefully interested in entering into a joint venture strategic alliance relationship.

The question becomes, is this “standard approach” an ABSOLUTE NECESSITY or is it possible for a junior miner to take a different route to getting into production WITHOUT all of that share structure damage, so that SHAREHOLDER REWARDS can be maximized. If there is indeed a possibility for bypassing the damages associated with taking the “standard approach”, what circumstances need to be present to pull it off?

The truth is that it is almost an ABSOLUTE NECESSITY to take the “STANDARD APPROACH” UNLESS the junior miner can string together a long list of accomplishments that collectively render it as not being an ABSOLUTE NECESSITY, but good luck trying to line up that many stars all at one moment in time. Here’s the problem:

-

Most junior miners need either the technical expertise or the superior financial wherewithal of a major miner to even start the journey from exploration to development to production. Since the major miner has all of the cards, it will mandate that the junior miner and its shareholders shoulder all of the RISK throughout the journey. The job of the management team of the major miner is to force the junior miner to “DE-RISK” the project from the point of view of the major miner and its shareholders.

-

Almost all juniors are therefore FORCED to take the same “TRADITIONAL APPROACH” through the exploration and development stages UNLESS they can somehow remove their dependence upon getting a major miner involved. If they can’t lessen this dependence upon a major miner, then the result will lead to the need to sell hundreds of millions of shares at near zero share price levels in order to fund the preliminary stages of exploration like geochemical sampling, baseline environmental permitting, surveying and gridding, mapping, trenching, IP/IR, aeromags, satellite surveys, etc. From the point of view of a major miner, these are the components of the “DE-RISKING” process i.e. the removal of “GEOLOGICAL UNCERTAINTY” by the junior miner on behalf of the major miner.

-

If a junior miner gets lucky in these exploration/development endeavors, then they might identify some drill targets. This is typically followed by the need to sell yet another boatload of shares to fund several phases of diamond drilling. If the deposit is of a “disseminated” variety wherein the sought after metals are spread out broadly in tiny increments that would need to be open-pitted, then there is no way to avoid massive amounts of drilling and the completion of feasibility studies. This is because it is the drill results that allow the “kriging” process that leads to the most efficient open pit design. If the mineral deposit is a “disseminated” deposit in need of an open-pitting approach, then it is “GAME OVER” for the junior miner as far as being able to circumvent massive levels of SHARE STRUCTURE DILUTION. Only VEIN DEPOSITS, with a much lesser need for diamond drilling, qualify for even a shot at circumventing dilution.

If, on the other hand, the target is a “VEIN SET” deposit, especially one THAT HAS PREVIOUSLY BEEN IN PRODUCTION, then the need for extensive amounts of diamond drilling likely will not be there. It’s not that there’s anything wrong with a lessened level of “GEOLOGIC UNCERTAINTY” associated with drill results, it’s just the associated share structure dilution.

If a junior miner is relying on a major or mid-tier miner for their technical expertise or their superior financial wherewithal, then forget about it, YOU NEED TO SELL TONS OF SHARES AND DO THE DRILLING AND THE STUDIES IN ORDER TO “DE-RISK” THE MAJOR MINER. For the shareholders of the major miners, they like this reality. For the shareholders of the junior miners, not so much. In essence, there are 2 categories of junior miners, those that need a major miner and those that don’t.

-

If the target is a vein deposit that has previously been in production and it already has a vast network of adits, drifts, raises, and ventilation chimneys that you can simply walk into and take channel samples from, then you might just get lucky and be able to avoid selling all of those shares and diluting the share structure. Intra-adit “channel samples” are nice because they consist of a larger “sample size”. Drilling is nice because you can cover a greater area especially with “disseminated” deposits. With either modality, the goal is to develop a 3-dimensional “block model” of the deposit and to thereby lessen “GEOLOGIC UNCERTAINTY”.

-

If you have a previously mined vein deposit with all of those developmental improvements already in place AND you have a CEO willing to advance all of the cash needed to go all of the way into production, then thank your lucky stars because you have a definite shot at going into production with a tiny number of shares outstanding compared to those taking the “standard approach” and therefore the ability to generate extremely robust levels of EARNINGS PER SHARE. Once again, we need to keep in mind that the ULTIMATE GOAL for any junior miner is TO GET INTO PRODUCTION WITH AS FEW SHARES ISSUED AND OUTSTANDING AS POSSIBLE.

-

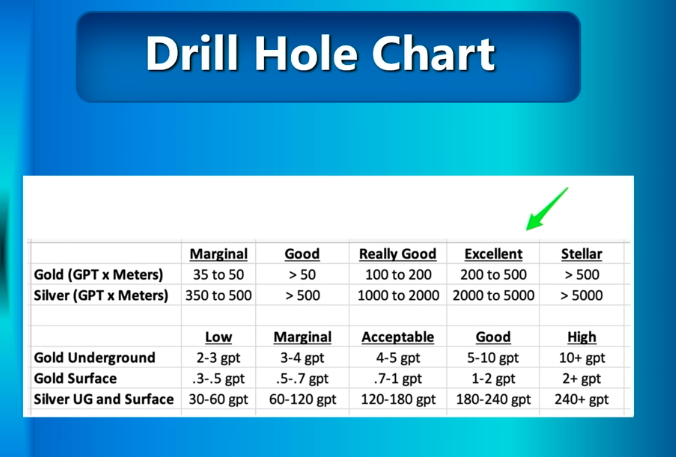

Thankfully, the veins contained within “VEIN SETS” like those that Auryn has, tend to be somewhat “homogenous” in nature. The individual veins within the “VEIN SET” tend to have similar grades, widths, gangue components, patterns of constriction and dilatation, etc. If you can gather a lot of geological information from one vein within a “VEIN SET” because of prior production efforts, then you can roughly extrapolate the findings to the other component veins. For example, both the Merlin 1 Vein and the DL2 Vein feature extremely high “bonanza” gold grades (>100 gpt) at the 1,850 meters above sea level elevation. Until proven otherwise, there’s a pretty good chance that Auryn’s other 5 “Main Veins” might have similar grades at similar elevations.

-

Any junior miner able to bypass the need to enter into a JV relationship with a major miner, still needs to be able to raise funds in order to construct its own ore processing facility. Auryn was fortunate enough to enter into a debt facility arrangement with an institutional investor so that this critical “box” could be checked off on.

-

The key component for Auryn was the willingness of the CEO to advance all of the funds necessary to explore and develop the property WHILE CHARGING ZERO INTEREST. Junior explorer/developers do nothing but spend money. Diamond drilling is very expensive as are feasibility studies. Prior to making a bona fide discovery, the share price of a junior explorer is typically next to zero partially because of the distant odds for success. Share structure dilution happens very quickly when share prices are low. A CEO willing to advance the cash needed while charging zero interest and being willing to be paid back AFTER PRODUCTION COMMENCES is an absolute godsend for investors. That tightness in the share structure will tend to last the entire life of the corporation. The CEO received no share compensation even though he could have easily sold himself ultra-cheap shares in order to fund development. This is noteworthy. Part of the reason the CEO was willing to advance the cash is that he was already the owner of 62% of the common shares. He would be the biggest victim of any share structure dilution. In order to pull off this “coup”, it sure makes it easier if management has a lot of “skin in the game” and their financial incentives are closely aligned with the smaller shareholders.

-

The main reason for the very expensive series of feasibility studies is to determine if the project is “ECONOMICALLY FEASIBLE”. When the price of the 3 metals being mined are trading at or near their all-time highs, and the vein grades are exceedingly high, then the “ECONOMIC FEASIBILITY” was never in question. This results in a lesser need for “feasibility studies” although certain geological information is needed to create the mine plan. Diamond drilling programs as well as the series of feasibility studies are not only ultra-expensive, they take a long time to carry out. When you have near surface, high-grade, EARLY PRODUCTION OPPORTUNITIES and the prices of the metals being mined and sold are at or near all-time highs, the last thing you want to do is take 4 years out of production and do the drilling and studies when you already know that the project is easily “ECONOMICALLY FEASIBLE” today.

-

A key concept at play is “GEOLOGICAL CERTAINTY”. Both the CEO willing to cut all of those checks and the institutional investors that cut a $4 million check for the ore processing facility, needed to arrive at a comfort level in regard to “GEOLOGICAL CERTAINTY”. They didn’t need to be “DE-RISKED” to the same extent that a mining major would have demanded. They both know that they will be paid back promptly. They’re not that interested in “OFFICIAL” NI-43-101 COMPLIANT MR/MR. The offtake partner, probably Glencore, is not going to ask Auryn how many “OFFICIAL” ounces of MR/MR they have on the books prior to handing them a check for a truckload of float concentrate. “OFFICIAL” NI 43-101 COMPLIANT OUNCES OF MR/MR are indeed nice to use as a “screening tool” for investors trying to compare the prognosis for the success of 2 different mining investments in which both miners are mining a “DISSEMINATED” open pit deposit. One of the more disappointing aspects of blocking out NI 43-101 COMPLIANT MINERAL RESERVES/MINERAL RESOURCES is that it often costs more to block out “in situ” ounces in the ground than an acquirer is willing to pay for each ounce in the ground. But if you are totally dependent upon a major miner, then you do what you have to do.

SO, WHAT’S THE BIG DEAL ABOUT GOING INTO HIGH-GRADE PRODUCTION WITH A TINY NUMBER OF SHARES OUTSTANDING?

The key is that existing shareholders don’t need to share the profits from operations with many other investors. A “JUNIOR PRODUCER” with a tiny number of shares outstanding will generate a much higher EARNINGS PER SHARE versus a different miner generating the same level of profits but with more shares outstanding. The junior miner with the higher level of EPS will also likely trade at not only a higher share price but also at a higher “multiple” of EARNINGS PER SHARE than a “JUNIOR PRODUCER” with a gazillion shares outstanding.

As you can see, in order to pull off a coup like this and bypass all of that share structure dilution, an awful lot of “stars” need to be aligned.

BUT WHAT ABOUT THE “MARKET RE-RATE” EXPECTED WHEN A JUNIOR MINER TRANSITIONS INTO BECOMING A “JUNIOR PRODUCER”

A brand new “junior producer” with an “AVERAGE” number of shares outstanding should expect an “AVERAGE-SIZED RE-RATE” (percentage increase in share price) when it transitions into PRODUCTION. A brand new “junior producer” with a tiny number of shares outstanding that is capable of generating a robust level of EPS, should expect a larger percentage “MARKET RE-RATE”. This is because EPS DIRECTLY determines share price when multiplied by the industry-standard “multiple”.

However, don’t expect “the market” to pay any homage to a junior miner with a tiny number of shares outstanding UNTIL it goes into PRODUCTION and is capable of generating a superior level of EPS. Until it successfully transitions into PRODUCTION, “the market” will probably treat it as just another junior miner “wannabe” with a miniscule chance of ever going into PRODUCTION. The SHAREHOLDER REWARDS will indeed be enhanced but sometimes they are delayed until PRODUCTION commences. Many investors don’t even look at SHARE STRUCTURE. This is what makes the transitioning into PRODUCTION time period the “sweet spot” for investing in this sector ESPECIALLY IF THE JUNIOR MINER DOING THE TRANSITIONING WAS ABLE TO KEEP ITS NUMBER OF SHARES OUTSTANDING AT A MINIMUM BY CIRCUMVENTING THE “TRADITIONAL APPROACH” TO BUILDING A MINING COMPANY.