DOES AURYN LIKELY HAVE A 2-PLUS MILLION OUNCE DEPOSIT?

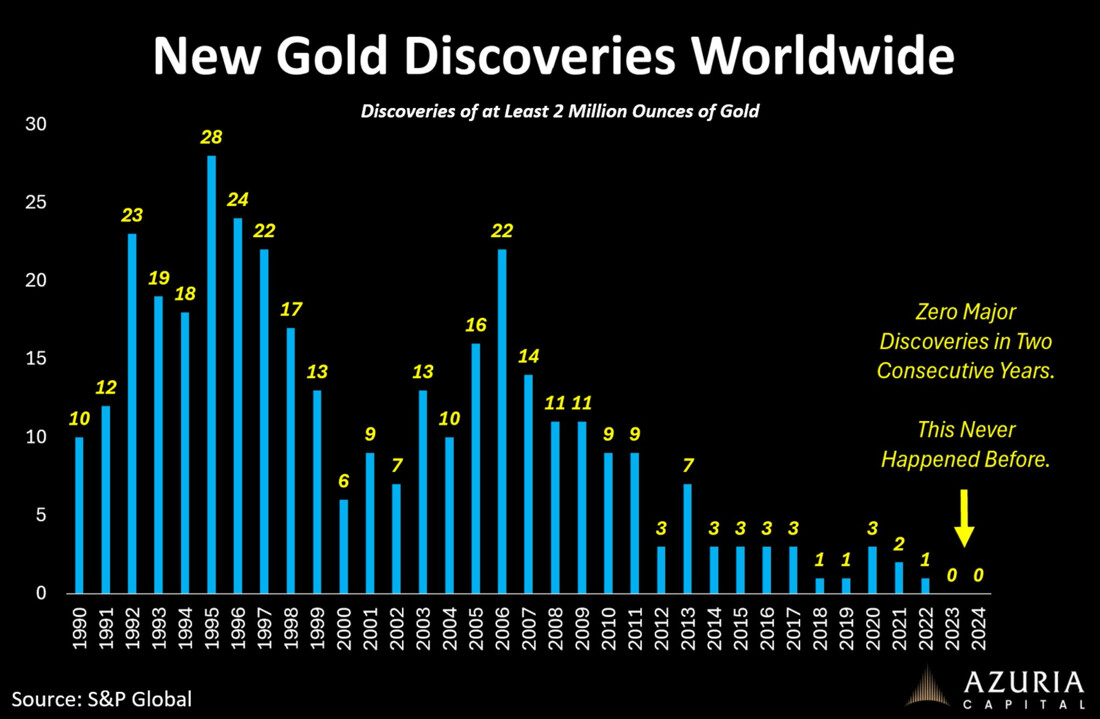

After seeing the chart of how no new 2 million ounce gold deposits have been discovered for a couple of years, the question might come up as to what are the chances that Auryn currently owns a 100% stake in a 2 million ounce deposit at the ADL Mining District. First of all, let me make it 100% clear that for Auryn to be included on a list of miners that have “OFFICIALLY” made a 2 million ounce gold discovery, they would have to sell hundreds of millions of shares in order to raise the money needed to fully drill out the deposit and execute a series of studies including a Preliminary Economic Assessment (PEA), a Pre-Feasibility Study (PFS), and a Bankable Feasibility Study (BFS). This is despite the fact that the deposit is CLEARLY “ECONOMICALLY FEASIBLE”.

Thankfully, Auryn cannot be FORCED to do this by a major miner demanding that the project be “DE-RISKED” prior to them being willing to get involved. Auryn needs neither their money nor their technical expertise to enter into extremely high-grade production at a time in which the price of gold is near $5,000 per ounce. If Auryn were to be compelled to “make the case” that they are indeed sitting on at least a 2 million ounce gold deposit, how might they do this without suffering all of that SHARE STRUCTURE DILUTION?

There are a variety of routes Auryn could take to make this case. Many years ago, they completed an exhaustive trench sampling program on the ADL plateau. They mapped the course of and identified over 5,000-lineal-meters of veins that made it all of the way to the current surface. What they discovered/confirmed was the existence of a geological “VEIN SET” consisting of approximately 7 Main Veins all but one of which (the Merlin 3 Vein) are oriented in parallel striking from NNW to SSE. They successfully traced one of these veins, the Don Luis2 Vein, down to a depth of 700-meters.

In a massive vein deposit like this that has yet to be fully drilled out, there is a very simple means to ROUGHLY ESTIMATE the tonnage of ore present and ROUGHLY ESTIMATE the number of “contained gold ounces” held within that tonnage. What you do is multiply the combined known length of the veins (5,000 meters), by their average width and then multiply that by their known extension to depth. In the case of Auryn’s vein deposit, you’d multiply the 5,000-meter known extent of the “strike” at surface, by an average width of, let’s say 1-meter,and then multiply that total by the 700-meter depth figure. This gives you a “VOLUME” of 3.5 million cubic meters of VEIN MATERIAL.

In order to convert this “VOLUME” figure into “TONNAGE” you need to multiply that 3.5 million cubic meters figure by the “SPECIFIC GRAVITY” (a fancy term for “density”) of granodiorite, which is 2.7 Tonnes per cubic meter. This then gives you a “TOTAL TONNAGE” figure of 9.45 million tonnes of vein material within that “Vein Set”.

Next, you need to estimate the “AVERAGE GRADE” of the vein material itself in order to estimate the number of “CONTAINED GOLD OUNCES” within the vein material. Note that this “AVERAGE GRADE” figure is going to be higher than the “AVERAGE GRADE” of the ore being mined because during mining some of the less well-mineralized rock material surrounding the vein itself will be mined. In making “CONTAINED GOLD OUNCES” estimations, you limit your analysis to vein material within the vein proper.

Estimating the “AVERAGE GRADE” of the ore within the vein material proper necessitates the study of all previously acquired information relating to the grades mined and detected throughout time. This is a complicated topic that deserves attention. I’d start with the fact that the artisanal miners mined a 350-meter stretch of the DL2 Vein’s 1,000-meter surface “strike” down to a depth of about 100-meters. They achieved an “AVERAGE GRADE” of 64 gpt gold from 1940 to 1970. The TONNAGE mined was approximately 2,000 Tonnes i.e. a “mom and pop” type of operation.

They were mining from levels 0, 1, and 2 of the DL2 Vein. The artisanal miners had pretty much zero technology available to enhance their AVERAGE GRADE. About all they could do was VISUALLY SORT the ore and discard what appeared to be nonmineralized ore. Interestingly, their mining operations were so inefficient that many of the “tailings dumps” they left behind for Auryn and Medinah are currently carrying 14 gpt gold grades. These “tailings dumps” sit outside of the portals to the adits leading to level 1 and 2.

Auryn intersected “level 3” of the DL2 Vein in early January of 2023. Level 3 is located about 30-meters below level 2 at approximately the 1,850-meters above sea level elevation. THE AVERAGE GRADES DETECTED AT LEVEL 3 WERE MUCH HIGHER THAN THOSE ENCOUNTERED IN LEVELS 0,1, AND 2 (64 gpt). At the new intersection of level 3 and the DL2 Vein, Auryn executed 2 groupings of channel samples. The first grouping of 4 separate channel samples came in at an AVERAGE GRADE of 164 gpt gold. The second grouping came in at an AVERAGE GRADE of 150 gpt gold.

Auryn sent in a 2,200 pound sample from level 3 to Enami for smelter testing. This significant-sized sample came back with AVERAGE GRADES of 57 gpt gold, 983 gpt silver, and 3.23% copper. This represents a “gold equivalent” AVERAGE GRADE of 70 gpt gold. This was slightly higher than the AVERAGE GRADE achieved by the artisanal miners. After getting these stellar results (the average grade of gold being mined in similar underground “narrow vein” mining worldwide is 4.18 gpt gold), Auryn sent in another batch of samples, this time to the smelter testing facility of the Plenge Lab in Lima, Peru. These results came back with not an average gold grade of 57 gpt gold like the Enami smelter test, but instead an average gold grad of 128 gpt gold. Upon receiving this result, Auryn’s BOD unanimously decided not to do business with Enami but to instead build their own processing plant and bypass Enami and what appeared to be usurious “tolling fees”.

Clearly, the grades at the DL2 Vein have been stellar from the beginning. Recall that the ESTIMATED TONNAGE calculated from just the 7 Main Veins that made it to surface, came in at about 9.45 million Tonnes of vein material. Keep in mind also that one Troy ounce per Tonne equates to 31.1 gpt. Thus, 9.45 million Tonnes of vein ore averaging, let’s say, just 15.5 gpt gold (0.5 ounces per tonne), would represent about 4.7 million ounces of gold just in the veins that made it to surface IF THE VARIOUS OTHER INPUT VARIABLES HOLD UP. Clearly, one could make the case for a much higher AVERAGE GRADE than 0.5 Ounces per Tonne, but I’m not going to make that case.

In addition to the gold contained within the veins that made it all of the way to surface, Auryn also has gold contained within the Pegaso Nero copper/moly porphyry prospect, the LDM stratabound gold/copper deposit, the 24 new “structures/veins/faults” discovered while drifting the Antonino Adit, as well as any yet to be discovered deposits at the ADL Mining District. The amount of precious and nonprecious metals contained within the Pegaso Nero will likely dwarf the ounces contained within the veins that made it to surface but that is going to take a lot of exploration and development work to confirm. The ridge crest sampling program completed at the Pegaso Nero deposit revealed a 1.2 Km by 3.6 Km area with high-grade areas of both gold and moly right at the surface on the southern downslope off of the ADL plateau.

So, does Auryn’s ADL Mining District deserve to be included in the list of discoveries weighing in at over 2 million ounces? My answer is ABSOLUTELY NOT AS OF TODAY BECAUSE, AGAIN, THAT LIST APPLIES ONLY TO FULLY DRILLED OUT DEPOSITS WITH COMPLETED FEASIBILITY STUDIES.

Do I hope that Auryn drops everything and takes 4 years away from production and fully drills out the deposit and then executes those feasibility studies in order to make the “OFFICIAL” list? Absolutely not. The prices of the metals being mined are at or near their all-time highs TODAY. At times like these, you do everything in your power to get any HIGH-GRADE, NEAR SURFACE,EARLY PRODUCTION OPPORTUNITIES into production. Auryn was blessed with many of these; many deposits have none. Later, if Auryn wanted to “make the list”, they could do the drilling and studies using the profits from production instead of the proceeds from selling an enormous amount of shares.

As an investor, I don’t want to trade in an extremely tight share structure (70 million shares outstanding) and a microscopically low number of shares in the “float” (about 7 million shares) for a spot on an “OFFICIAL LIST”. In my mind, the ADL Mining District EASILY qualifies (or will qualify) to be on the “LIST”. As an investor, I need to check off on “boxes”. One of my “boxes” is: does this deposit easily have at least 2 to 3 million gold equivalent ounces. I’ve already checked off on that box without undergoing massive levels of SHARE STRUCTURE DILUTION. Do I need to know the EXACT number of ounces of MR/MR that are in the ground? Absolutely not.

About 5 years ago, Auryn’s Professional Geoscientist, Luciano Bocanegra, did a “Preliminary Resource Estimate” of the number of gold ounces present in just the upper extent of 2 of Auryn’s 7 Main Veins. The number came in at 686,000 gold ounces. This did not include the much higher grades found at level 3 of the DL2 Vein.

In estimating the number of “CONTAINED GOLD OUNCES” in a mineral deposit, there is the concept of a “cut-off grade” that is critical to appreciate. The “cut-off grade” is roughly the grade of ore that results in the miner breaking even on a mining project. Thus, ore with a grade BELOW the “cut-off grade” DOES NOT count towards the number of “contained gold ounces” in a deposit.

When Bocanegra made his “preliminary resource estimate”, the price of gold was around $1,500 per ounce. Since then, the price has moved to about $5,000 per ounce. The “cut-off grade” for economic viability has DROPPED tremendously since Bocanegra’s calculation. This means that a lot of ounces previously slightly below the old cut-off grade are now easily “Economic” and need to be counted. That 686,000 gold ounce figure might be 50 to 100% higher today then back then.

Since Bocanegra did his calculation, Auryn has made significant advances in the “development” of the vein system, especially at level 3. Although they did not involve diamond drilling, these advances have markedly increased the number of “contained gold ounces”. The drifting of horizontal adits is basically an extra wide drill hole oriented horizontally instead of vertically. They both help outline a 3-dimensional “block model” of the mineral deposit. In combination, Medinah and Auryn have completed a total of 31 diamond drill holes to date.

Auryn just completed a 66-meter vertical “raise” from level 3 up to the “old workings” in levels 1 and 2. This has the potential to add significantly to the “contained gold ounces” count. In 2 separate quarterly updates, Auryn cited that they were busy blocking out new ounces of MINERAL RESERVES/MINERAL RESOURCES (MR/MR). As of yet they have not updated the shareholders on the current estimation of “contained gold ounces”.

WHAT DOES IT MEAN WHEN YOU ARE ADVANCING INTO EXTREMELY HIGH-GRADE PRODUCTION AT A TIME IN WHICH THERE HAVE BEEN NO NEW GOLD DISCOVERIES AND THE PRICES OF THE 3 METALS BEING MINED AND SOLD ARE AT OR NEAR THEIR ALL-TIME HIGHS?

The best way to irrefutably confirm a new gold “DISCOVERY” is to put it into PRODUCTION. Many new “DISCOVERIES” will never make it into PRODUCTION or they might currently be a half dozen years from commencing PRODUCTION. The problem is that the metals prices are going nuts TODAY. The lack of new discoveries is going to put upward pressure on gold prices for some time to come. Gold mines represent “depleting assets”. With time, the miners have found themselves going deeper and deeper in search of lower and lower grade ore. Many of the majors have curtailed their own exploration budgets because of the low chances for success and they rely more and more on the junior miners for not only new discoveries but also for doing what is necessary to advance the project into production and thereby “DE-RISK” it.

When a junior advances a project into PRODUCTION, this means that almost all of the RISK has already been mitigated. The remaining RISK usually centers around OPERATIONAL RISKS which are always present. A thoroughly “DERISKED” project already in production at a time in which the metals prices are breaking out to the upside and there are not many other new “discoveries” available to compete with them, are worth a lot of money. The majors MUST constantly replace the ounces they annually produce by either expensively drilling out new ounces and executing the necessary studies or by taking out junior miners with viable discoveries especially if they have already been “DE-RISKED” and are already in PRODUCTION.

Although the high-grade gold veins and the cash flow they are about to generate is going to be wonderful for Auryn and Medinah shareholders, the “elephant in the room”, in my opinion, is still the Pegaso Nero copper/moly porphyry prospect. Without any fanfare, Auryn just added Robert Mayne-Nicholl to their team. He recently ran 2 of the top 7 or 8 producing mines of all time i.e. Los Pelambres and Collahuasi, both in Chile. These are both “world class”, Tier 1 porphyry projects.

In this sector, there is a saying that the category known as “NEW PRODUCERS” is almost always empty. A “NEW PRODUCER” either gets rapidly taken out by a major or a mid-tier or it rapidly advances into becoming a “mid-tier” producer. The most recent gigantic success story in this sector was probably “Great Bear Mining”. They executed a drill program and before they blocked out even one ounce of “OFFICIAL MR/MR”, Kinross took them out for about $2 billion. Their property will be in PRODUCTION probably by 2030.