Good morning EZ. Not looking for a following. There are a half a dozen blind optimists like yourself, following the “analysis” of one guy who is so far off the mark that I find it worthy to point out the (seemingly) obvious flaws in his analysis. A vocal minority who seems to be emotionally charged when facts (the “dark side”) run counter to their little tea party. Always attacking the messenger b/c they are too ill equipped to challenge the message.

Baldy,

I hit the link on your recent post labeled “PRICE EARNINGS RATIO” written in blue. It showed the most recent NYU study for P/E ratios in various sectors. Under the “METALS AND MINING” line-item they listed the P/E ratios based on 3 subtypes: Current, Trailing, and Forward. The numbers are 92, 54, and 29.82. Two years ago that 29.82 figure was 30.1. Under the “PRECIOUS METALS” category, the corresponding numbers are 119, 26.8. and 16. The arithmetic average of those 6 numbers is 56.

For some reason, you chose to present your case by citing the “16” figure and omitting the other 5. Why not just present the data in its entirety and leave it at that? You chose Barrick as being the miner most representative of Auryn of all of the miners you could have cited. Why? It has one of the absolutely lowest P/Es of all miners and its production profile is going backwards.

Individual miners that can show the most robust GROWTH PROFILE are going to be rewarded by “the market” with the highest P/E ratio. Investors want to sense GROWTH POTENTIAL and they want to sense that next quarter’s production and earnings figures are likely to be higher than this quarter’s numbers.

Let’s go back to “THE LASSONDE CURVE”. The Lassonde Curve looks like a forward-leaning capital “N”. The spot on the curve where the production growth and value starts going parabolic is exactly where Auryn is right now, just prior to proving to the world that they are indeed “in production” and not only in production, but in production at a time in which the 3 metals being sold are all trading at or near their all-time highs. Investors are looking for “new producers” whose share price has not already tripled or quadrupled.

Anybody with the ability to fog a mirror could confirm that it will take Auryn at least 10 to 20 years to mine out their 7 Main Veins at plant throughput rates of in between 100 TPD and 300 TPD. Anybody could study the cumulative GIS Database of all of the work done on the ADL to date and come up with the conclusion that there is, at a minimum, at least 1 to 2 million ounces of gold equivalent present. You don’t need to take 10 years off in order to fully drill out all of the veins, the Pegaso Nero, and the LDM and spend hundreds of millions of dollars by selling billions of shares in order to make these conclusions. There will be plenty of time to do lots of drilling and pay for it not by selling shares and destroying the tight share structure but by reinvesting the profits while servicing any debt.

It is “the market” that will act as the arbiter of what P/E ratio to assign; it’s not you nor is it me.

7 Likes

Precious Metals is the space we are working with here. If you want to reference Metals and Mining we’ll have to get into a discusison on how lithium miners and AUMC aren’t really comparable and why the M&M P/E is specifically inflated b/c of those types of names being included in that sector.

I’m almost tempted to give you a few minutes to erase your comments on averaging the trailing P/E numbers. It’s still early enough in the morning and, if you truly believe that trailing P/Es are relevant, especially in commodities, it would demonstrate a complete lack of knowledge on some pretty basic valuation concepts.

I did provide the data and link to the actual “recent study at the Stern School vs. the one you keep referencing.” I didn’t cite the other “5 numbers” b/c they have literally nothing to do with the sector’s actual forward P/E which is 16. To be crystal clear, AUMC doesn’t have trailing nor current earnings/PE so the forward P/E is, by definition, the only metric to consider.

To summarize: your 30.1 P/E is from the Metals and Mining Sector (not precious metals) and its from two years ago (!) and you’re still trying to lean on an argument for a higher P/E by averaging the trailing P/Es of both the M&M and PM sectors. Excellent pivot.

This type of loose interpreation of aged metrics is EXACTLY what got you into this situation. I’m simply calling you out on sloppy diligence.

Here it is in a nutshell. Along with whacky valuation assumptions there is a belief that the market is finally going to align with your fascination of this asset in the absence of boring old industry standards (resources, mine plans, etc.). You may end up being right on the asset but NOBODY is going to assign a valuation to a company based on the data currently available.

Playing with valuation metrics to suit your narrative while claiming that any idiot and eventually the market can just assume there are millions of ounces, feels very much like bulletin board antics. Not a billion $ market cap ($14 per share), which is equally absurd for all of the obvious reasons. Its a diservice.

1 Like

Anybody who can fog a mirror can also use AI.

While the Lassonde Curve can provide a useful high-level framework for understanding investor psychology in the mining sector, applying it to Auryn Mining is likely overly simplistic and potentially misleading. The Lassonde Curve was primarily developed around the traditional lifecycle of a mining company progressing through sequential stages of discovery, resource delineation, feasibility studies, financing, construction, and ultimately production. AUMC does not fit neatly into that conventional model.

Rather than advancing through a standard, multi-year development pathway centered around formal engineering studies and large-scale mine construction, AUMC appears to be pursuing a far more hybrid and opportunistic strategy. The company is attempting to leverage historical mining data, trench sampling, underground workings, and high-grade vein identification — including the DL2 structure — while simultaneously constructing a relatively small processing plant intended to validate the mining thesis operationally. In effect, the company is attempting to generate real-world mining and processing data before completing many of the traditional milestones that the Lassonde Curve assumes occur first.

This creates a significant limitation in using the Lassonde Curve as a predictive tool for future stock price behavior. The framework assumes that valuation compression naturally occurs during long periods of feasibility work, permitting, and financing, where companies often consume capital without generating operating results. However, in AUMC’s case, the key valuation inflection points may depend less on traditional study milestones and more on practical operational execution — specifically whether the company can successfully complete the plant, demonstrate recoveries, reconcile mined grades with expectations, and generate cash flow. Those are highly company-specific operational outcomes that the Lassonde Curve does not meaningfully account for.

Additionally, the curve itself is not a law of market behavior; it is ultimately a generalized observation about investor sentiment patterns across prior mining cycles. Relying on it too heavily risks reducing a highly nuanced and asset-specific situation into an overly formulaic narrative. In practice, small-cap mining stocks often deviate materially from the “classic” Lassonde progression due to factors such as commodity price cycles, financing environments, jurisdictional risks, management credibility, retail speculation, promotional activity, and operational execution. In AUMC’s case, where the company is attempting to bridge exploration and early production simultaneously, those deviations could be even more pronounced.

More importantly, the market is unlikely to reward AUMC simply because it has theoretically reached a certain stage on a conceptual curve. The stock will ultimately be driven by whether management can prove that the geological thesis translates into repeatable and economic mining results. If operational validation is successful, the stock could rerate much faster than a traditional Lassonde model would imply. Conversely, if recoveries, throughput, grades, or execution disappoint, the stock could materially underperform regardless of where it ostensibly sits on the curve.

For those reasons, while the Lassonde Curve may provide some broad context regarding mining-sector sentiment cycles, relying on it in the case of AUMC risks oversimplifying what is fundamentally a highly idiosyncratic and execution-driven situation.

1 Like

Thanks Baldy for showing us how to prompt AI to make an argument for your thesis. Powerful stuff.

You can simply put the exact opposite query in and get a counter argument. You’ve proved nothing.

3 Likes

![]() We should all know the Suggested guidelines for use of AI replies in posts

We should all know the Suggested guidelines for use of AI replies in posts

1 Like

Let’s see what you come up with. My prompt was simply asking if the Lassonde Curve was a useful analysis given AUMC’s state of development. Does that have some sort of bias baked in or do you just not like the fact that AI reinforces what I have been saying? Then again, its just common sense.

2 Likes

Baldy,

Your ego here is overpowering your message here. Your response fails to tell us your personal story with this stock and why you are so compelled to counter any positive post with a denigrating counter attack. Your most truthful sounding answer as to why you spend so much time here is that it was for entertainment. It no longer serves a relevant purpose except to promote your oversized ego.

I have a moniker that came about because I initially fell for the Les trap and loved the story behind the Alto. Untold riches hidden within the mountain. You did also, and have held unbridled resentment ever since. It shows in every one of your counter attacks. You bragged endlessly how smart you were to ditch the stock when you did and take the loss. Problem is you never got over it!

My moniker was a proclamation that I finally met my goal of attaining a million shares of MDMN. It was easy and I became known as “easymillion” which I foolishly compiled at great expense in my retirement account. Yes, I was a Rainbow Chaser as were many at that time. Bummer! I’ve grown over it, and fortunately had a sizeable position in CDCH which is now held as AUMC shares. I think you mentioned you have some shares of MDMN somewhere so that you have a legitimate reason for spending so much time and effort here. I thank you for educating all shareholders and prospective shareholders that you are so much wiser and successful than anyone else here these many years.

Just wanted to let you know I still have my millions of shares here, safely tucked away. Amazingly, I have become more optimistic than ever that with continued persistence I may yet do better than breaking even. I may even turn a profit from this stock! Time will tell. It’s an interesting story of persistence and possibilities that continues to unfold.

Having realized for many years this is a longshot speculative stock I don’t follow it blindly. It’s been many years since I have advocated this stock as an active trading stock. I think that day is coming. When it does, I’m sure I can count on you to proclaim you’ve been realistically awaiting that day. Afterall, you are the greatest and smartest of anyone here.

EM

7 Likes

We are at about the 12 week mark for the floatation plant testing phase. They should be about done testing it and ready to start production. But are they?

7 Likes

Final operating permits for the flotation plant and tailings facility remain pending. Permitting timelines were impacted by a cybersecurity incident affecting the regulator’s systems, and Auryn has maintained close coordination with SERNAGEOMIN throughout this period. All technical inquiries and information requests have been fully addressed. The Company expects to receive both operating permits in Q1 2026 and will issue an official announcement upon receipt.

https://aurynminingcorp.com/january-2026-shareholder-update/

AI: “The SERNAGEOMIN cybersecurity incident in December 2025 severely worsened an already backlogged permitting environment in Chile, delaying processing timelines for multiple mining operations. The temporary shutdown of internal electronic platforms forced the regulator to utilize manual workarounds, triggering widespread delays. Multiple mining operations across Chile faced backlogs and project delays due to the widespread nature of the SERNAGEOMIN cybersecurity incident. The SERNAGEOMIN system freeze disproportionately hit junior or mid-tier operations looking to enter active production or expand current capacity.”

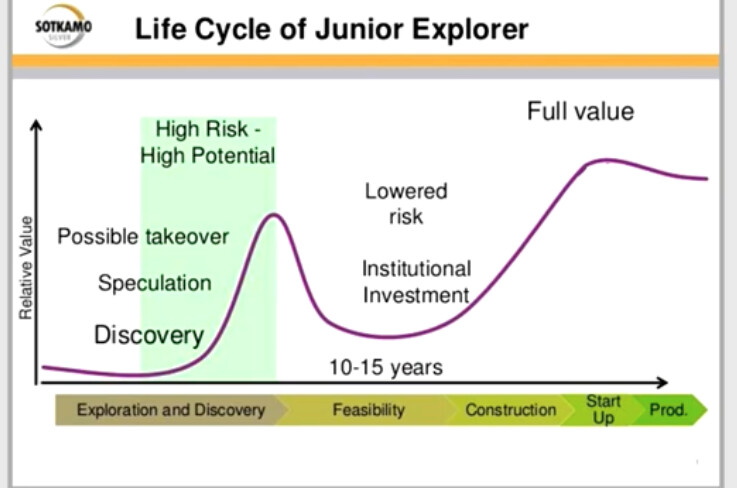

I found this graph from Barry Holmes of particular interest to recent discussions of time delays for explorers to reach production and full value.:

For a bootstrap operation such as Auryn, a 15 year delay or longer, although rare, may not be unexpected. In a bootstrap operation many of the parameters that contribute to the construction of a typical Lassonde curve are lacking. Instead, Auryn is an anomaly using a lower-cost underground development, directly mining the hi grade veins, rather than expensive surface drilling to prove out the ore body. Auryn has mostly avoided the massive share dilution typical of junior miners. It will be a cash-flow-per-share metric that can spike far more aggressively than a heavily diluted, traditionally funded institutional miner.

EM

2 Likes

Hi EZ,

I believe those 2 permits landed a month or so ago and were announced on “X”.

2 Likes

EZ. More fluff. Thanks for the history lesson. If you want to dismiss my counterpoints as ego driven or motivated by some ulterior motive that is your prerogative. If you are able to rebut my points of view instead of avoiding them even better. I’m simply challenging the P/E of 30 and Lassonde Curve references that have “plagued” this board for years. I’m sorry you feel that any post that doesn’t embrace the unrealistic euphoria narrative is somehow driven by a personal vendetta vs grounded analysis. You and others insecurity in entering a healthy debate on the merits of this investment speaks for itself. I’m thankful for the return of the likes of MGold. I usually don’t agree with him but at least he’s objective enough to engage in a worthwhile discussion.

1 Like

Baldy, your posts remind me of Liam Hardy’s Reverse Lassande Curve on Linkedin that some call a FUBAR Cycle This is what you pound into the history of this stock every time you post! Actually, I agree with many of your comments about the Lassonde Curve. As Liam Hardy Says:

The most commonly referenced ‘Life Cycle Assessment’ of publicly traded junior mining companies is often credited to veteran minerals investor Pierre Lassonde, who introduced the ‘Lassonde Curve’ in 1990. Anyone in the industry will tell you that investing in a listed vehicle today is nothing like it was in the ’90s, and this model is now sadly obsolete and outdated.

Wes Roberts comments, “Junior exploration is very very high risk, anecdotally only one in 1400 mineral discoveries ever result in a producing mine.” So I do give some validy to this often repeated statistic, that you so admirally relish. It is your constant mantra here.

I have a very substantial paper loss that I don’t constantly moan about day after day. I have moved on from my disappointment in this one stock by necessity. I don’t have the choices available to me that you have because my circumstances are quite different. My reality is I have lost nothing as my potential investment is still intact in a retirement account where it makes no sense to write off a tax loss of the magnitude shareholders have encountered. Looking at my portfolio this morning, I have moved on and find satisfaction in my successful 10X+ profit in HYMC, 470% gain in SKE, 440% gain in KGC, 268% gain in WPM, 260% gain in LUGDF, 249% gain in AEM, 220% gain in HL, 220% gain in PAAS, 217% gain in HCHDF, and 179% gain in NEM. I have many high percentage gains in many, but not all of my more speculative stocks as well. I have more core holdings than I mention above. Other more traditional investments that I feel are good investments make the larger base of my portfolio. My judgements are sound and I have no need to blindly follow anyone, including you John.

There’s an interesting alternative to the traditional Lassonde curve that I mentioned tangentially in my earlier post. Holmes is exploring share price and exploration financing. The traditional Lassonde curve is an old theory applicable to many situations based on expectations of potential. Early buyers are often takin by the hype in an early discovery phase of a mining stock.. Once upon a time you were one of those as an early buyer of MDMN. John, you ended up taking a very substantial loss way back then and have never taken responsibility for a bad investment decision. You fail to mention that these days in your history here.

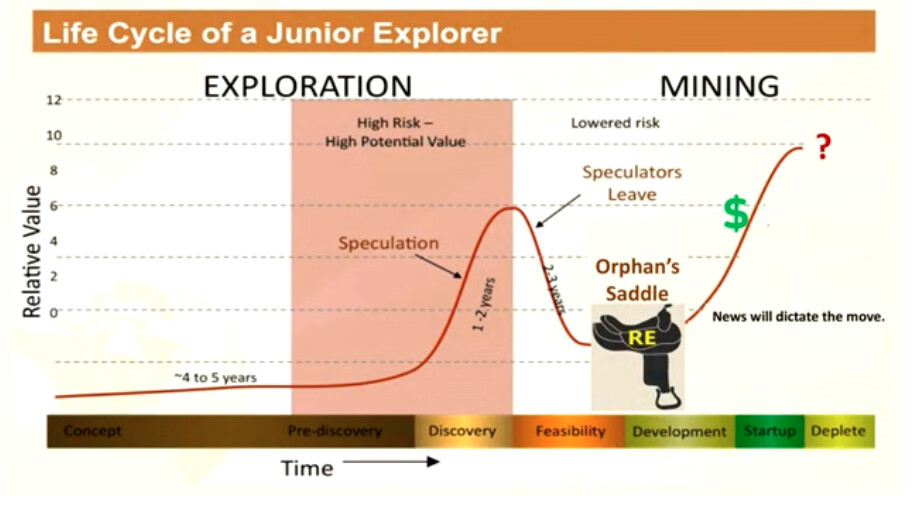

So what relevance does that have to shareholders today? The area we have been transitioning through is what Holmes neatly called the orphan period of uncertainty, or in the following chart the Orphan’s Saddle. Again, the chart of particular interest I’m referring to is from Barry Holmes. It is from a presentation on explorers to reach production and full value.: ![]()

I think we are in the very early stages of the orphan’s saddle. We have yet to have confirmation of the completion of the successful commissioning of our floatation plant. Next shareholders will be seeing what grades are being processed and what recovery rates from various head grades can be obtained. There will be a mixing or ores to determine a steady run rate from ore already mined. There are permits to be obtained and expansion of operations to 3000 TPM. Shareholders will hear of initial FCF and expected payback of debts owed. There will be substantial news flow updating progress that will start to be promotional in nature. Don’t forget there is a Commodity Rotational Event coinciding with a Secular Bull Market in Gold occurring with predictions of POG going much higher for many years. At some point the receivership of MDMN shares will be finalized and a process for a prorata distribution of AUMC shares will follow. The stock will actually start to become a trading stock.

EM

3 Likes

·

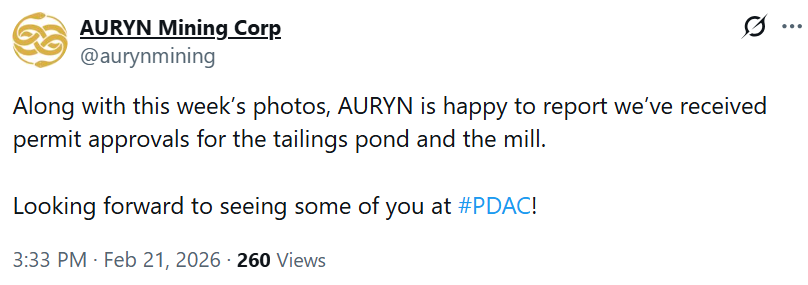

Along with this week’s photos, AURYN is happy to report we’ve received permit approvals for the tailings pond and the mill.

6 Likes

I just saw this on the x link posted by BB: 4/17/2026 “Hear that? Mill commissioning is underway with rock crushing beginning Monday.”

So you are right again Miike. They are at least crushing rock and dialing in optimization parameters. Should be an update on progress forthcoming.

EM

2 Likes

EZ. I’m glad you took another opportunity to walk us through your PA. Not sure how that is relevant but, specific to your “Life Cycle of a Junior Explorer” I would simply echo some of my points on the Lassonde Curve. Holmes’ chart isn’t much more relevant, with the exception of “junior.” It baffles me how some are trying to compare AUMC to these various life cycles. There was no exploration nor feasibility stages so any analysis of what the share price should do at this stage is useless. I’m not trying to say that this is bearish or bullish (even my AI response has plenty of potentially positive distinctions), it’s just not a helpful tool to use in attempting to speculate on what the stock may or may not do in the months and years ahead. In any event, I will applaud your effort to make at least 50% of what you wrote releveant to the topic at hand vs personal ruminations.

1 Like

I just have to repeat myself Baldy. You are definitely the greatest and smartest of anyone here. You have the definitive answer for every investor! ![]()

EM

8 Likes

I thought by now they would have posted an update on the receivership portal on the status of any creditor claims and/or settlements. .

2 Likes

Karl is there anyway to see if any claims have been filed in the Nevada courts? That should be public info, no?