Lack of capital to do so makes more sense to me. That’s why I think they have said production profits will supplement the exercise price.

Hypothetically, suppose they only have $100 million to invest in this project. Putting that into the option leaves them in a similar position as MDMN, all land no capital. Then they need to go out and raise funds. Instead they use their capital to prove the property, flip the porphyry and eventually take out MDMN.

::: once again, these are my opinions and not necessarily those of management of any of the involved companies :::

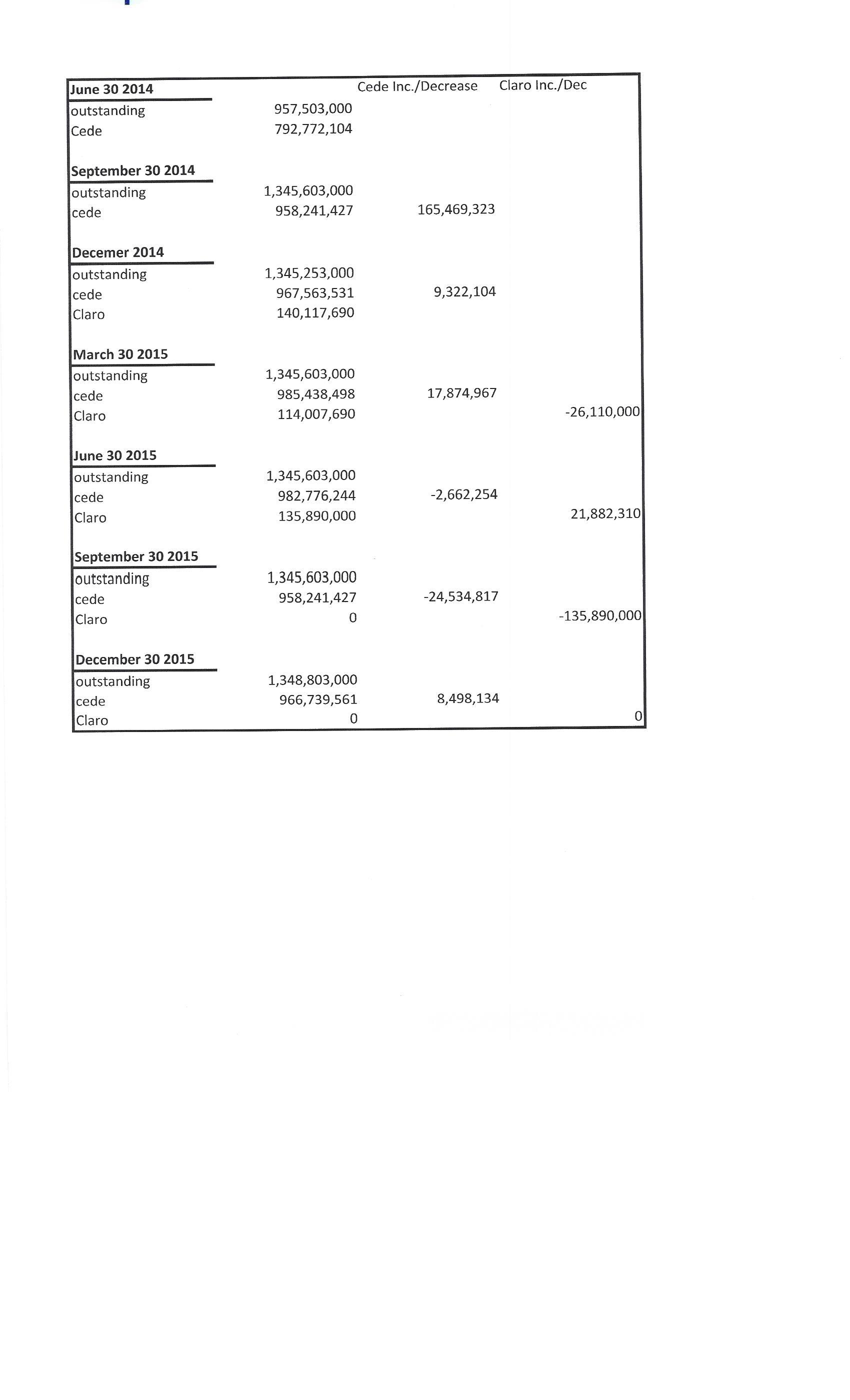

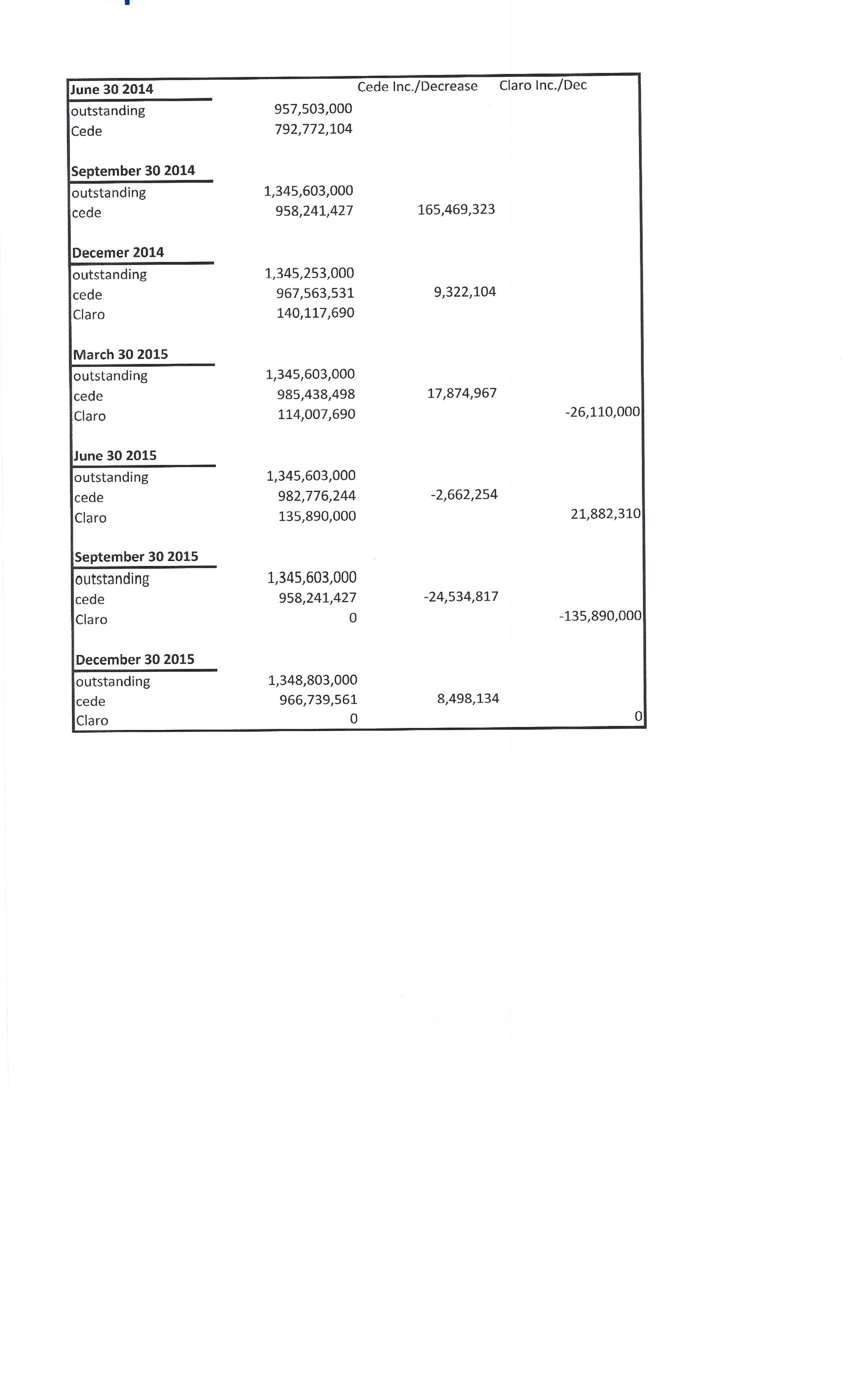

Been doing some DD on MDMN’s share structure and I must admit it is confusing. I have attached a pic of the results below. I tracked it back to the quarter before Juan converted his preferred to common. What is interesting in somewhere between June 30, 2014 and September 2014, the o/s went up 388,100,000, so if Juan got 350 million, who got the other 38 million?

Also, notice the continual rise in shares deposited with CEDE. Now if Auryn was buying in 150 million in the open market when the stock was soaring, and they, according to legend, demanded it be in cert form, there is no way that they could have pulled 150 million out of Cede.

Claro is another head scratcher, we all know that, but his total for Q1 2015 decreased 26 million and increased in the 2nd quarter 2015 by 21.8 million than boom, under 5%.

Also, look at the Cede totals, they are all over the place, going up, going down and then up. Something is fishy

The point I am making about the JJ conversion and this 38 million, was two fold, who got 38 million, but more importantly I find it odd, that as soon as the conversion hit, 165 million shares were deposited into CEDE (i.e. free trading stock).

35 million of the preferred went to JJ, Claro and friends for the 49% Medinah Chile that MDMN did not own and there was about 3 M preferred still outstanding on a loan conversion.

It’s quite simple- he’s the lowest cost option. And he’s hardly a “firm”, rather a sole prop working out of his house. I would have rather they found an inexpensive practitioner without prior sanctions, but given how minimal our compliance requirements are, I don’t think anyone really cares. Look on the bright side- it is always fun playing “find the typos” every quarter!

Haven’t finished it yet. You’re too fast.

Haven’t finished it yet. You’re too fast.