You’re looking for resources not reserves, We need a NI 43-101 report which will take some time. Near-term production may be a quicker boost to our share price. At the risk of being the wet rag, everybody here needs to prepare themselves for many months before we see fundamental news that will serve as a catalyst for this stock.

Yes, I’m looking to add to my position but not really feeling the urgency at this point. I can’t find many precious metals stocks that haven’t doubled, tripled, our quadrupled, year to date BUT Medinah will have it’s day. This has become a “sock drawer” investment that will surprise and exceed expectations when you least expect it. Until then, enjoy your summer break.

Thanks John for confirming what I thought that we are still aways from NI-4301 reports being completed. But just to clarify, a NI-4301 includes reporting on both mineral resources and reserves, and other reports etc. Ahem , LOL.

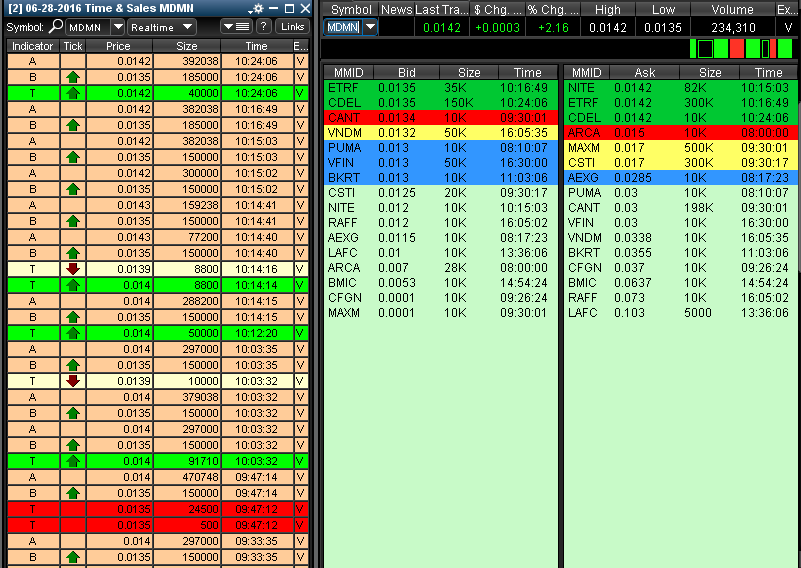

And worthy of note is , despite the SP, I am delighted that almost 1 million CDCH shares were traded today. WHOOOEEEE

Just playing with you John , we will get there also in good time.

It is exciting that we are finally in a very good position and just waiting for the imminent next good news .

I am just waiting for the eventual confirmation of the WCD designation.

Should be self-evident to many here that any talk of a N1-4301 is rather moot at this point in time.

It situations with high grade near surface gold deposits that show obvious signs of continuity, one simply mines it. A Chilean/Peruvian company has no reason to waste time and money on Canadian style resource reports that involve lots of drilling and endless studies. The mine’s profitability is obvious. The permit restriction of 5000 tons/month is the limiting factor; not the size or quality of the deposit. The mining experts have already designed the mine, funds have been committed and mine preparation has begun. They may be able to follow a similar approach for the Fortuna.

When drilling starts on the low grade Pegaso Nero target or other locations on the Alto, it will then be time to be taking about resource reports etc. again. One exception to this is the Gordon Breccia which has had already enough drilling to consider a NI-4301. However, it appears that Auryn has decided that the Gordon isn’t worth pursing at this time at least compared to the potentially more attractive Pegaso Nero that likely is much larger with better near surface geometry to contemplate a large scale mine than the steeply plunging Gordon Breccia.

Can you provide an example of a miner that is being rewarded for an “obvious” yet unconfirmed deposit (formal resource)? I can appreciate Doc’s frustration that his “perceived value” is never discounted in the share price and I understand that you believe the profitability is “obvious” but in the real world these factors need to be quantified before value is assigned in the markets.

MDMN is a bit of an exception at this point b/c their initial funding is being covered. Unlike the past two decades, they no longer need Les pumping the stock so that capital could be raised at higher prices (less dilution). So, I would agree, there’s going to be less of a focus defining the resource. Small, near-term production, is the gameplan for the immediate future which will then self-fund the drilling to finally define the resource. The resource will also be defined as the mountain is mined. At this point, Masglas WILL be interested in maximizing the “perceived” value of the mountain as they go out to raise capital (to minimize dilution).

Getting into production at a run rate of 15, 20, or even 30koz isn’t going to be the silver bullet for our share price. There are dozens of companies producing at the level with sub $20M market caps. The share price will react when the size of the resource/life-of-mine is determined. IMO

You might recall that Auryn also drilled the Gordon and also did independent verification of the previous Gordon drill results. Stating “Not even close to support a 43-101” is just plan goofy. I suppose you actually mean/commenting on is whether there is enough information to state whether they have delineated a resource or not. My answer to that is that it is a moot point. They have passed on the Gordon breccia for now in favor of more promising targets.

Yes that is what I meant. Which is exactly the same thing as what is needed to support a 43-101. Not even close. I wouldn’t call the Gordon a “moot” point unless you don’t understand the meaning of “moot.”

It is often costly and difficult with an underground vein style deposit to try and define long term reserves in the same manner as you can do with a low grade large open pit. It is not untypical for underground mines to only have defined mine lives of 5 to 7 years because of this, sometimes shorter. Look at Volcan’s mine lives as an example.

Gold Resource Corp, an example I am quite familiar with, operated for several years without any formal reserves and regularly was criticized for it from the financial community. GORO sort of considered itself anti-wall street and thumbed their nose at the criticism. Eventually they capitulated because shareholders complained about the same thing. They eventually drilled farther ahead and came up with a 3 year reserve estimate. And it just keeps moving out by 1 year each year that goes by - i.e. remains at roughly 3 years out. It is just too costly and complex for them to try and drill all over the place where they have no intention of mining in the short term. Wall Street and shareholders seem, at least most, seem to have accepted the compromise, mostly.

On the other hand, Auryn is talking about an open pit over by Fortuna. And to do an open pit design you need to at least have some decent definition of the ore body you are chasing in terms of extent and depth.

Ultimately the answer, though, comes from the May 16 Auryn Update:

As we progress toward full scale production AURYN will provide updates regarding costs, mine life, and reserves.

We’ll hear something, mid-next year or so probably. There is no doubt it will be less than a complete accounting of the mountain when we first hear something.

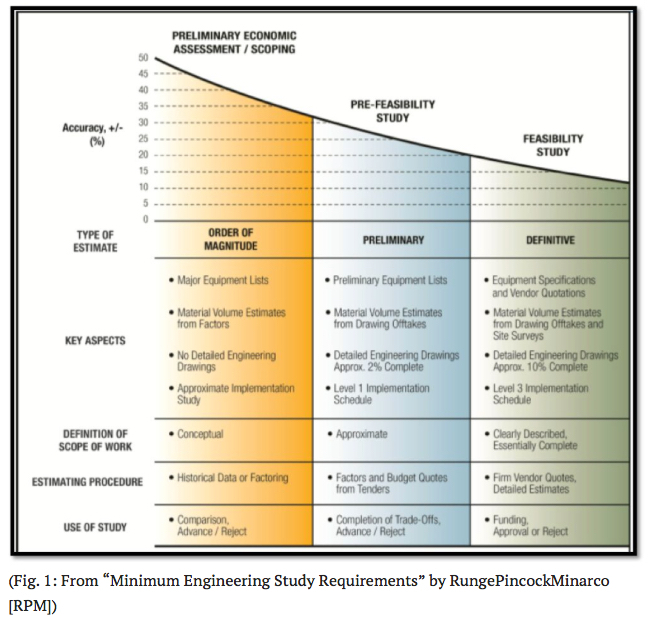

NI 43-101 covers a variety of disclosures. Here we examine the sequence of three engineering studies used to assess, with increasing detail and accuracy, the potential value of a mineral property.

The three studies are:

The Preliminary Economic Assessment (PEA)

The Prefeasibility Study (PFS)

The Feasibility Study (FS).

As illustrated in the chart below, the studies are conducted in the sequence listed. No set scope exists for any of the study levels.

These studies are not new. They have a long history as the engineering basis for the orderly development of mining and other capital intensive projects. The study series spans the gap between exploration and construction. Fundamental to the practice of mine development is the principle that rigorous engineering breeds project success. The corollary is true as well: weak or sloppy engineering leads to project failure.

NI 43-101 codified the traditional study contents and added requirements for public disclosure, plus oversight by a “Qualified Person.”

Generally the PEA (often termed “scoping study” outside the coverage of NI 43-101) takes less time and costs less than the PFS or the FS, mostly because less drilling, lab work, and engineering are required. A PEA might require from several weeks to a year to complete and cost from $100,000 to $2.5 million. A more detailed PEA might reduce or even, in very special circumstances, eliminate the need for a PFS. The findings are suitable for either rejecting the project or approving funding for the PFS. They are not adequate for full project approval. Estimate accuracy is no better than ±40%.

The purpose of the PFS is to evaluate all the available options for mining, processing, and infrastructure in order to fix the plan to be evaluated in the Feasibility Study. The Pre-feasibility study is the first stage with enough financial resolution to determine and declare mineral reserves. Like the PEA, the PFS provides sufficient information only for project rejection or approval of the next study phase—the FS. The PFS might take six months to two years to complete and will cost from about $500,000 up to $10 million or more for a major, multi-billion dollar capital project. Estimate accuracy is no better than ±25%.

The FS describes and evaluates the complete project to be built. The design work is sufficient to support cost estimates at ±15% accuracy and is the proper vehicle for approval to construct. The time required to complete the study will range from at least one year to as many as five years; and, it will cost between $1 million and $50 million for large capital projects in remote, inaccessible areas.

Some noteworthy aspects of NI 43-101 studies are:

• All three studies must follow the same cumbersome NI 43-101 Table of Contents.

• Studies must be sanctioned by one or more “qualified persons” (QP).

• The study report, or an extensive executive summary of the report, must be posted on the SEDAR[1] web site for public access.

POSTED ON AUGUST 14, 2015 BY TIM OLIVER

CATEGORY STORIES,

The March 1 and 23, 2014, issues of EI contain a two-part series titled “Top Ten Signs of a Bogus NI 43-101 Report.” This is worth a read. http://blog.ceo.ca

The PEA, PFS, FS sequence is is the wall street / finance friendly process that a company typically follows in order to move a deposit down the risk slope and up the financial-resources-available slope. Basically it is the proven process by which to identify a deposit, determine it is production worthy, and then get the resources required to put it into production. It is not a legally required process. Some companies like Gold Resource Corp have never produced a single one of those reports but have been in production for nearly 10 years.

We know this sequence is not going to apply to a portion, perhaps a significant portion, of the ADL complex. Why? Because Auryn has already made a production decision and is implementing it with their own capital for the Caren / Merlin 1 vein, and is going to do so again, according to their updates, with the Fortuna and other Merlin veins. These reports do not bring any value to Auryn at that point so why spend the money to create them beyond whatever they have already done internally to make their production decision?

This self-funding approach provides them money to continue exploration without having to raise it from the markets. And it could enable even larger production moves, such as the LDM perhaps, in time, if it makes sense, without having to follow the above process. Although, I think one could speculate safely that if / when they get to considering putting the P.Nero porphyry (or another) into production then they would be talking about a need for hundreds of millions of $$$ and then the traditional process would be more likely to apply. But that is not a 2016 or 2017 issue. Or, if they were intending to go public they would probably need to generate some type of formal reports in order to demonstrate to wall street in formal known ways what they have identified / proven to date. Else, why bother?

Not having to follow the traditional path can be good and bad. It’s good in that self-funding avoids dilution, debt, etc. But it makes for a more ambiguous path forward. What is going to happen besides ‘production’ and increasing production? How do the shareholders benefit? These are the questions Auryn will be answering in the months ahead. Right now they are just trying to establish the basics of trust via openness, communications, and execution to plan. One should expect the next level of questions like the above to be addressed by Auryn at the AGM, imo.

Absolutely … AURYN has already determined a portion is suitable for early exploitation and moving it forward rapidly. All else will fall into place sequentially in due time. A question however … concerning the LDM … when is that portion of the various potential project targets planned to move forward to production? The LDM was of great interest well before the most recent target discoveries. Perhaps some answers will be forthcoming during the SHM presentation. AURYN is moving forward with the areas having the quickest return and least expenditure first.