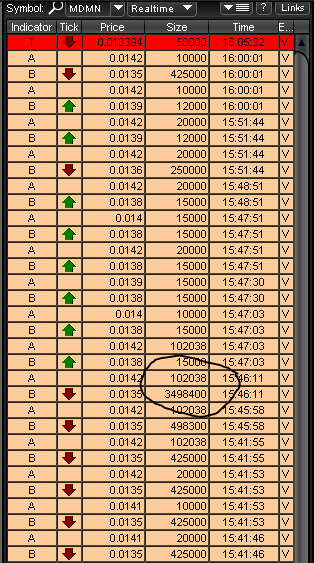

Did anyone else see that 3 million share bid show up and was immediately jumped @.0135? Or was it my l2?

Great BID almost 50k let’s see if this is a start of things to come. Progress by Auryn setting up for production continues. AGM 3 months lets go!!!

I remember when I was a child riding in the car to visit my grandparents. It was only a couple of hours drive. For a 7 year-old that’s a very long time.

The highway portion seemed particularly slow . . . like it went on forever and time stopped. The last 15 minutes on the highway seemed twice as long as the first 90 minutes. However once we got off the highway and into the local streets in their neighborhood the pace and excitement quickened.

I think we’re getting to the end of the highway with respect to MDMN. We’re not there yet, but I suspect we’re close.

11 Likes

Auryn contracts with liderman to handle security as the ADL moves into production.

http://www.liderman.com.pe/noticias/nuestro-ingreso-a-chile-4/

Link was from FB

3 Likes

Nice. Note that they are based in Lima Peru and just in Jan 2016 bought out another firm in Chile as an expansion to their business into Chile.

Quite a long list of clients with some names familiar even to Americanos. And the Peru connections continue.

4 Likes

Do you hire a security firm if you’re just going to be doing a little exploring?

10 Likes

Indeed MDMN/Auryn have changed their way of communication. I found a comment someone made on Facebook and MDMN’s reply.

Rick Carle: I’m delighted we’re being kept informed,helps with the wait

Like · Reply · 1 · 1 hr

Medinah Minerals, Inc.

Medinah Minerals, Inc. Thank you. We’ll do the best we can to keep everyone updated. New management, new company, new way of communicating. We realize we need to earn your trust back.

Like · Reply · 48 mins

9 Likes

reverse the letters in Carle’  …nice they’re so responsive. Should be useful if questions arise in the future

…nice they’re so responsive. Should be useful if questions arise in the future

1 Like

I think the recent discussion on the role of blocking out MR/MR as it pertains to the market’s valuation of Medinah specifically needs to be customized a little more for Medinah and especially Masglas, a private corporation. The key is what are Maurizio Cordova’s near and long term goals and how does blocking out MR/MR rank as a priority. Does allocating capital strictly to block out MR/MR at the ADL or for cranking out a 43-101 make sense to him. After all it’s his money and he’s steering the ship which is a PRIVATE entity? A PRIVATE entity with the intent of going PUBLIC on, for example, the TSX or TSE, has to crank out an NI 43-101 compliant F-1 Technical Report as a listing requirement.

Maurizio/Masglas is currently wrestling with about a dozen deposits at various stages of development. We need to keep in mind that the process of blocking out MR/MR still occurs when you go into production. The question arises does he want to attract major miners into the ADL project NOW or does he want to fly solo during the current phases which are famous for possible parabolic growth in NPV should the production growth profile at the Merlin Mine or the grades encountered surprise the investing public. What might a couple of long intersections into the Cu/Mo porphyry at the PN do in regards to how much a major would pay for an “X” percentage stake in the action? Another question that arises has to do with the type of investors Maurizio is trying to attract. What is the relative importance to them as it pertains to early cash flow versus MR/MR?

Part of the issue is that in the current mining sector, especially in regards to copper, the market is NOT rewarding MR/MR very generously so many mining firms blessed with deposits with near surface early production opportunities will allocate capital more towards early exploitation than blocking out MR/MR for the sake of blocking out MR/MR in order to attract investors. If you’re only going to get awarded $5 to $15 per ounce of gold equivalent reserves why spend dozens of millions of dollars over several years specifically to block out MR/MR? The other issue is do you have high grade near surface early production opportunities (“low hanging fruit”) to focus your capital allocation on while the macro market is readjusting how it treats MR/MR.

Any prospective major can look at the GIS database collected to date at the ADL and conclude that tonnage and MR/MR are NOT going to be much of an issue at the end of the day for this deposit. They won’t have the comfort level associated with knowing for a fact that perhaps there are 8.674 million ounces of gold equivalent in the proven and probable categories blocked out in perhaps 400 drill holes but do they need that level of certainty over and above knowing that MR/MR is not an issue in order to pull the trigger on a deal if MC wants to do a deal now? Sophisticated mining investors might even respect proper capital allocation during the phases of mining cycles in which MR/MR just doesn’t earn rewards proportionate to costs.

When mining was on a tear back when the POG was $1,900, CEOs were leveraging to the hilt to acquire MR/MR with questionable economics behind them. Those same CEOs are now gone or deleveraging their balance sheets by selling these assets and taking huge writedowns. MR/MR is still the gold standard in this industry for comparing deposits but if I were running a private company I’d swap cash flow and money in the bank for numbers on a 43-101 any day especially if tonnage is clearly not an issue to any prospective investors.

Any upcoming drilling near the Caren/Merlin Mine or near the planned open pit at the Fortuna/Merlin 3/Fortuna Oeste might be more designed to guide exploitation efforts and/or pit optimization studies rather than strictly blocking out MR/MR. At the PN, however, I could envision Mauricio going after a couple of long intersections into the Cu/Mo porphyry in order to alleviate any anxiety regarding its existence.

Depending upon how long you foresee Medinah being around, I’m not sure MR/MR issues are even going to play much of a role. It takes a lot of money and time to block out MR/MR. In Medinah’s lifespan, from a valuation point of view, I would think that cash flow from the early gold production opportunities would trump anticipated MR/MR figures well down the road.

I think we’re fortunate that the early production opportunities relate primarily to GOLD (with possible copper/silver byproduct credits) and not primarily to COPPER in this post-Brexit vote era of uncertainty. The question now is what is a holding company with 1.35 billion shares O/S run by Gomez, Goodin, Solar and Maurizio with a 25% stake in AMC and a 36.25% stake in Nuoco worth.

Admittedly, from the point of view of a brand new mining investor just coming onto the scene, if Medinah had a gazillion ounces of MR/MR formally blocked out it would be easier to attract and maintain that investor’s attention. MR/MR is the language this mining industry speaks. But the entire universe speaks cash flow, profitability, share repurchases and cash dividends when they become a reality. What I personally would like is irrefutable proof of the existence of a clear pathway to a very, very long term sequence (long mine life) of progressively larger cash dividends. This way if the market mysteriously continues to refuse to budge when presented with positive news at least I can take that dividend cash and buy more ridiculously priced shares and thereby expose progressively larger shareholdings to progressively larger cash dividends over time.

4 Likes

Did you see the new FB cover?

5 Likes

Very happy to see Medinah on the same page as Auryn/Masglas for public view

2 Likes

Look at this client list of who they represent

1 Like

I hope they’ll put the Medinah logo up there.

1 Like

Why? (a) we have nothing to protect (b) it means we forked out money needlessly. No more dilution is my motto

Let them prove value too the property ,then someones going to want our 25% stake

What kind of vehicle will they be moving concentrate in?

Test conditions confirmed the best recovery method entails use of a Falcon gravimetric system processing previously concentrated ore.

Will they be concentrating 15 g/t ore? I doubt it. Likely this ore will be shipped directly to the refinery to get cash flow going. But it looks to me as though they intend to use a gravimetric concentrator once they obtain permits and begin open pit mining on the Fortuna.

If they choose the Falcon SB Concentrator for coarse and fine precious metal recovery within a grinding circuit the concentrate could warrant something other than a 20-50 ton dump truck. Just noting the initial cutoff grade on the Caren mine:

AURYN’s engineers plan to ramp up production to achieve this level of production during the next 6 to 8 months, with a cut-off grade of 15 g/t gold.

Metallurgical tests conducted at laboratories in Perú returned an average gold recovery greater than 90%. Test conditions confirmed the best recovery method entails use of a Falcon gravimetric system processing previously concentrated ore.

and for Sepro’s Falcon SB Gravity Concentrator:

The target mineral will usually be in extremely low concentration (grams per tonne) and a very high upgrade is desired (up to 10,000x).

Surface gold sampling in the Fortuna area was not extremely high. The above use description of a concentrator appears to be most suitable to the planned open pit. It can process up to 400 t/h! AURYN has shown itself to be a short term and long term planner. I would expect early exploitation cash flow numbers to jump very quickly once the open pit Fortuna mine becomes operational.

1 Like