TORONTO, ONTARIO (Dec 19, 2018) - Inventus Mining Corp. (TSX VENTURE: IVS) (“Inventus” or the “Company”) announces it has received the remaining assays for its recent drill program at the 100% owned Pardo Paleoplacer Gold Project (“Pardo”) near Sudbury, Ontario. A total of 35 holes at the 007 Zone were completed including 7 step out holes (see Figure 1), which are reported below. Holes 29 and 34 did not encounter significant values, and hole 35 was not completed. All holes were drilled vertically. Intercept lengths are true thickness. Gold grades are determined by fire assay and gravimetric methods; see note on

Technical Information.

The objective of this drill program was to provide drill data for the next phase of bulk sampling and demonstrate continuity of the mineralized conglomerate. The first 28 closely spaced drill holes (released on Nov 22, 2018) delineated a volume of approximately 6,000 tonnes of mineralized material (see the 007 Bulk Sample Outline on Figure 1).

Step out holes 31, 32 and 33 have all demonstrated that the mineralized boulder conglomerate reef extends towards the north under shallow cover. These new holes combined with previous drilling supports our interpretation that a highly enriched mineralized boulder conglomerate reef extends for 350 m North from the 007 Zone.

Mechanical Sorting Yields Gold-Rich Concentrates at Karratha; Egina Terrace Gravel Returns Positive Gold Result

VANCOUVER, British Columbia, Dec. 20, 2018 (GLOBE NEWSWIRE) – Novo Resources Corp. (“ Novo ” or the “ Company ”) (TSX-V: NVO; OTCQX: NSRPF) is pleased to announce gold-rich assay results from concentrates generated by mechanical sorting trials conducted on four bulk samples from its Karratha gold project and encouraging gold recovery from its first terrace gravel bulk sample at Egina.

In order to test the potential viability of mechanical rock sorting as a means of concentrating gold from conglomerates at Novo’s Karratha gold project, four bulk samples were collected, crushed, screened and tested using a TOMRA mechanical rock sorter ( for further details, please refer to the Company’s news release dated November 19, 2018 ). High-grade assays from sorted rock concentrates provide a first indication that this technique is effective at upgrading gold into small volume concentrates (Table 1, below).

Thanks Easy. I was going to post the same news release. Ore sorting is the game changer for these companies like Inventus, Novo and other Pilbara junior explorers. The Pilbara companies will be following Novo’s lead and leveraging from their growing pains. I’ve seen some crazy numbers being thrown around about how the ore sorting increases Novo’s gold production at a fraction of the AISC. Still too early to tell, but the next 12 months will be very telling for Novo and all the Pilbara plays as they all start proving up their conglomerate properties through bulk sampling and ore sorting.

So true! Pre-shipment ore sorting is proving to make many projects economically feasible. I can only imagine how using ore concentrating techniques on ore mined from the Caren and Fortuna claims would be a real game changer.

You want your head to spin with numbers?..this interview with Bob Moriarty (an unabashed Novo Resources and Pilbara bull since 2009)

Dissecting Novo’s sample at Egina:

The thing about the Egina deposit is that it is an alluvial deposit that time and tide has worn down into “lag gravel” and dirt at surface as opposed to hard rock. So the extraction costs are minimal and they measure in cubic meters as opposed to metric tonnes.

In Novo’s sample, 95 cu meters was tested and it returned 107.88 gm which equates to 1.14 gm per cu meter. Divide that by 31.1 (grams in a troy oz) to get .03665 oz per cu meter. A square kilometer has 1 million cu meters so multiplying by 1 million equates to 36,665 oz per square kilometer. Novo’s Egina tenements total 948 square kilometers. 948 * 36,665 = 34,750,000 oz. At $1200/oz, that equates to $41.7 billion.

I’m only extrapolating those numbers to demonstrate a very VERY rough potential upside…for only 1 of Novo’s properties. But this is where Bob Moriarty has been saying that Novo will be a 10 to 100 bagger even at current prices. Obviously the grades will vary in each cubic meter, but Quentin Hennigh felt that the bulk sample was representative of the property. Going forward we can use the results of this first sample as the benchmark to measure future samples. Even if it is only 1/2 of the grade, that is still eye-popping.

The other thing is the minimal extraction costs. At today’s gold price, the sample equates to $41.48 revenue per cubic meter. According to Keith Barron (of Fruta del Norte fame), the cost to process 1 cu meter of alluvial material in the US is $10. In Australia, it costs approximately $20 per cu meter. With those rough numbers, that equates to over $20 profit per cu meter. So the deposit appears to be economical.

The key will be the 50k bulk sample they have planned to start in March/April 2019. They will take samples from all over the property with the intention of coming up with a resource estimate so they can apply for bulk mining. If that 50k bulk sample confirms the results from today’s sample as being representative of the property at large, then this should light a fire under Novo.

And if Novo takes off, then usually the other Pilbara companies follow suit in sympathy.

Not sure that technology would be applicable at the Caren/Fortuna. Not an alluvial style deposit so no expectation that you could sort rock size to include/exclude sizes to concentrate the gold. The placer style deposits at the base of the mountain is another story but of course we don’t even know the status/plans for those claims if any.

Listened to the presentation etc. Very interesting.

My take on it is they really need to define an area that has a much higher gold grade/thickness than the average background concentration found in the deposit.

The reason is mostly due to mine design/permitting. I can’t imagine they would ever be allowed to strip dozens/hundreds of square kilometers of an area for their mine.

Rather a much more limited area that is particularly rich would fly especially initially.

The mechanical sorting part of the equation really does look good so cost to mine all of this does look quite low.

Yeah, they need to find a concentration of gold within the property. Obviously it’s very early, but if they take bulk samples all over the property, they’re bound to find such an area. I’m wondering if they can narrow down areas through magnetic surveys or geochemistry. However, my layman’s understanding is that magnetic surveys are more applicable to hard rock deposits where there is a concentration of gold that creates an anomalous footprint that can be detected. Obviously they can’t drill lag gravel, so targeted bulk samples seems to be their only option. They really have to think outside the box with this alluvial property.

The key here will be permitting and keeping the extraction costs low.

That’s the video posted as part of the Denver Gold Forum 2017 which started the conglomerate gold rush. Great PR. Sent the stock prices soaring. It was this video that got many here involved. I think Les must have produced it

But then Novo couldn’t follow through with figuring out how to arrive at an average grade for the conglomerate. And so we’ve sat for a year.

Now Novo / QH. is all excited about the alluvial gravels in the Egina area where supposedly the gold has been washed out of the conglomerates into the gravels. And they just reported their first bulk sample of those gravels a few days ago.

As an experienced Gold Rush watcher, it seems to me there seems likely there will be a large variation in grades in any extensive areas of gravels. Water does not flow evenly across ground for long unless it’s a very hard surface. QH’s biggest issue is finding a way to define a big enough resource to get to full mining permits. And yet because of the nature of the deposit he has to take a very large sample to arrive at some type of average grade. It seems to be a chicken / egg thing with Australian mining legal permitting process.

At any rate, I think they have permits for a 50,000 tonne bulk sample in the Egina area which they hope will be enough to lead to full mining permits. This sampling is intended to be started next April / May time frame as apparently it is too hot to work much until then in that part of Australia.

If you want to learn to speak Australian and hear what the locals are saying about the Egina play and the conglomerates, I suggest the HotCopper forum. You’ll find it’s painfully similar to reading TMP during the worst of times as stock prices have fallen so much. All the very same complaints about lack of transparency, stock manipulation, crappy management etc. And some of it could actually be true as we have learned. And occasionally there is the interesting local report of someone visiting the area and seeing what is physically going on. And again, there is that bizarre Australian dialect … mates

Thanks for that link…I think! Kinda reminds of IHUB I guess but I’m sure there probably is some good posters in there somewhere. If I lived in W.A., I would have my own jackhammer and metal detector and would be out in the middle of the night having a blast!

My final conclusion on the Pilbara is that it is indeed the real deal…or at least the portions of at or near surface. This is probably a contrarian view mostly because so many people got burned that they haven’t followed developments very closely over the last 12 months. It is clear that share price declines really hurt rational thinking.

Artemis

Pacton

Novo

Royal Nickel

Inventus (Palo-placer Canada)

2019 Stocks. I’m hoping for a pop with Artemis when they get government approval near term for the new gold mining circuit then perhaps move some of that into any of the others that lag.

I think the Pilbara deposit will be a big winner in 2019 if the price of gold can do even a half decent run to attract some investors and 1 or 2 of the various mining players there actually accomplish something.

Thanks! I read through that. I’m recommending NOVO to anyone who will listen for 2019/2020.(Artemis/Pacton are worthy related plays.) Everything looks good to me. Hard to imagine there will be many more(if any) plays like this going forward. Almost everything at/near surface has been discovered. Deposits at depth in general will likely be not particularly profitable or exploited due to the capital/operating costs involved(not to mention all the other types of risks a mining company faces) besides those directly adjacent to existing mines. (FYI…Kirkland is looking pretty strong these days, got to believe they will acquire more of NOVO.)

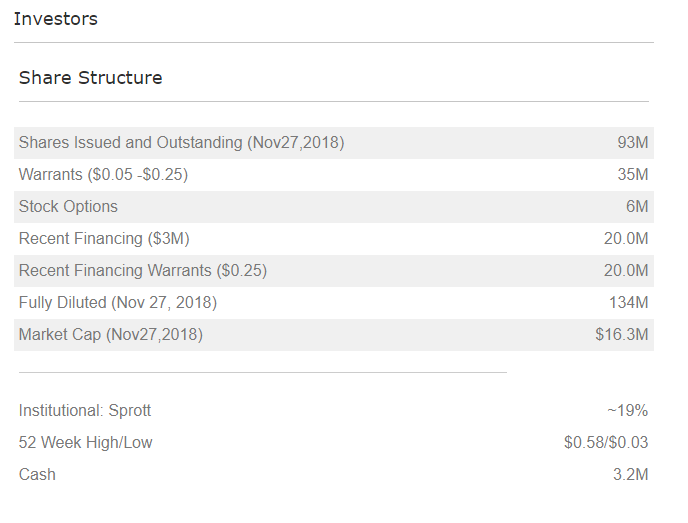

I’m looking into another interesting low-priced Canadian junior explorer - Sokomon Iron Corp (SIC.V) with projects based in Newfoundland and Labrador. Anyone familiar with this one? The stock spiked from around .05 to almost .60 in late July on the heels of an announced $3 million private placement by Eric Sprott at .15.

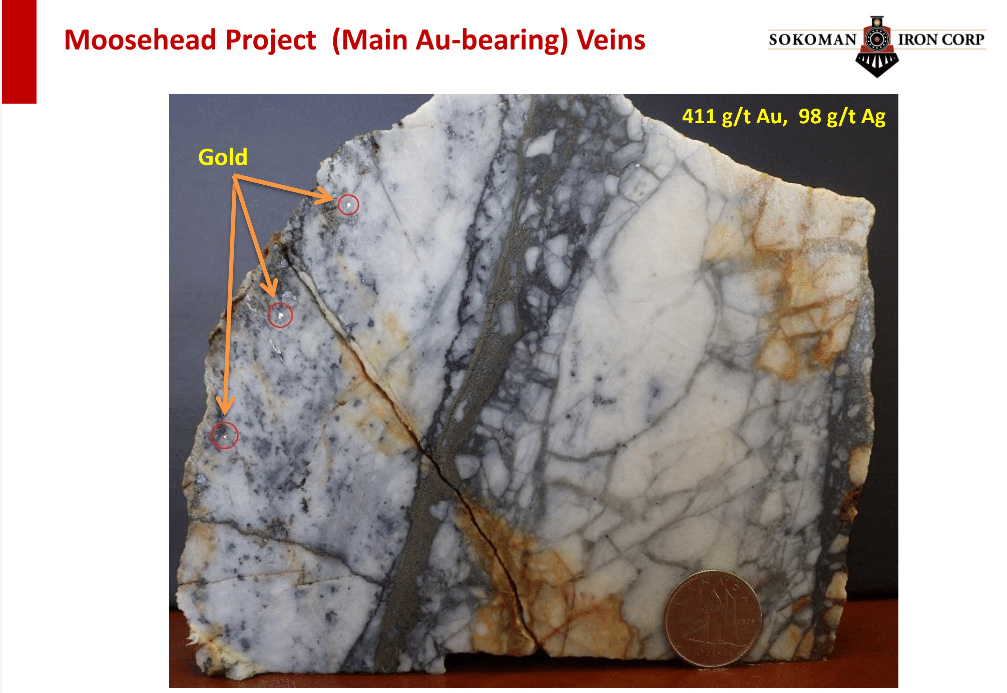

Looking at some of the drill results in 2018, and I can see why Sprott threw them some cash. There are some real high grade intercepts from their flagship Moosehead property:

Moosehead Project

5.10 meters @ 124.20 g/t, incl 1.10 m of 550.30 g/t Au with visible gold,

.60 meters @ 199.99 g/t Au, and .50 m @ 970.69 g/t Au

11.90 meters @ 44.96 g/t Au, incl 1.35 m of 385.85 g/t Au

2.28 meters @ 42.36 g/t Au

442 g/t Au from boulders

1.53 meters @ 170 g/t Au

There are more assays expected in a couple of weeks, so that might be a short-term catalyst.

Also, because they are not located in the mountains, they are able to drill all year round (they will be drilling on top of a frozen lake in Phase III in February. Additionally, the trans-Canadian highway intersects their property, so they have excellent access to infrastructure.

I’d taken a quick look at them, as there was lots of chatter about them on CEO.CA, first thing I noticed was the nice intercepts and the 2nd was Eric was throwing more into the pot. Definitely on my radar