Some day our mountain might look like this picture

![zppqgqud6dw41|351x499]and our little blue truck will be coming back from the smelter with this type of load…

but I’ll be pushing up daisies, no" probably a tree.

Some day our mountain might look like this picture

I hope I’m sufficiently diversified among “the winners” over the next few years. The sector will do well, so I’ll be riding the wave … ![]()

Shareholders are aware management is looking to put high-grade gold into production most efficiently to maximize profits quickly. The old adage “it takes money to make money” applies. Once cashflow begins is when we’ll see share price appreciation and oversized outside investor growth.

An active JV, perhaps for the LDM, or smaller selected open pits on the ADL, or even the PN, would be a definite plus. I think production would have to be in full gear first, to warrant that kind of attention.

My working theory is MC will not be in a profitable position until the price per MDMN share is anywhere from 6 to 8 cents (my recollection as to prices when he bought in).

Recall estimates, made in Jan 2016, of 664 KOz of gold in the top 200 meters of the Merlin 1 and Fortuna veins.

On the Merlin vein alone (not shown above), projected gold production was estimated at 5,000 Oz in 2016 and 25,000 Oz/yr thereafter for 2017. I surmise the Fortuna Mine was suggested as a better, higher value and more productive target by Dr. Sillitoe. There are only an estimated 4M shares reported in the public float! These are the 5% of the original CDCH shares which became the vehicle for creating the 100M authorized shares of the Auryn Mining Corporation. There are only 70M shares in the OS count, most of which are held by insiders and are severely restricted from trading. Consider the grades are at least as high as on the Merlin 1 (only 1st 200 meters used in original estimates), and I’d guess deeper than 200 meters, grades at the DL vein are even better … How fast and high do you suppose AUMC shares could rise with only 4M shares freely trading? How long will it take production to reach the 1st 25K OZs? How long to payback the interest free production loan? I’m sure there would be an accompanying interest in MDMN speculative trading awaiting disbursement. After MDMN shares (at 6 to 8 cents) are distributed and freely trading as AUMC shares, the expected conversion would be in the $12-$16 range at conversion! Perhaps MDMN trading anywhere from 3 to 4 cents would be OK for the conversion to make everyone whole in AUMC. ![]()

Personally I would like to see MDMN shares trading around .10 - .12 before conversion and it is not far off if AUMC strikes some kind of a deal/JV. For heavens sake this stupid shiba coin (air fart) went from .0001 to .42 and MDMN owning a certain percentage of a mountain that should have a WCD and won’t reach .10 - .12? I am thinking higher than that.

I think MDMN traded as high as about .19 way back - and they nothing close to what they have now, which is being on the doorstep of production and maybe a major getting interested in those telescoping mesothermals we seem to have found (se Brecciaboy’s explanation above).

But a fraction of the true O/S shares documented. Just keeping it real

Thanks for the reminder - what was the “alleged” O/S back then? Do you remember?

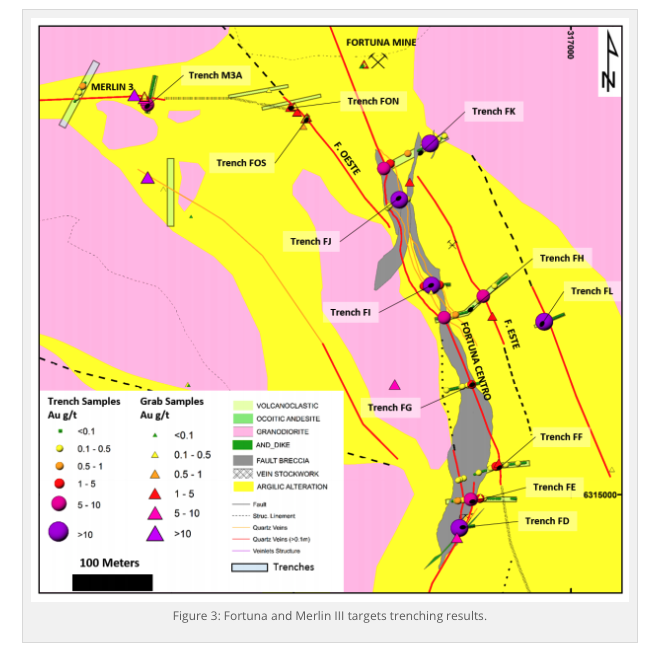

It’s kind of interesting how Usual Suspect posts a picture of the Bingham Mine open pit porphyry operation and shortly thereafter EZ posts a plot map of the trenching results showing the massive expanse of argillic alteration (the yellow stuff) surrounding the grayish colored “fault breccia” present at the plateau surface surrounding the Fortuna Centro Vein (now called the DL2 Vein).

When you have a porphyry deposit like that at Bingham, what you typically had at surface, prior to the excavation, is exactly what EZ posted i.e. veins, fault breccias and argillic alteration full of clays called illite, smectite and kaolinite. The overall process starts in a massive area of “plutonic” rock known as a “batholith”. The extremely high pressures and temperatures found at depth, cause the rock at the top of the batholith to expand causing the formation of an outpouching on the top known as an “apophysis”.

This bleb elongates upwards with increasing pressures and becomes a “porphyry stock”. These can be up to 3 Km in height. There is a lot of tectonic activity involved in the formation of porphyries and the associated veins, fault breccias, mantos, etc. When two tectonic plates rub against each other large cracks between the masses form called “faults”. If the opposing rock surfaces get ground into gravel then these “fault breccias” (pictured in gray) will form. The spaces between the gravel particles provide a wonderful way for metal-bearing hydrothermal fluids and gases to work their way to the surface. The smaller cracks that are formed can become metal-bearing “veins”. These extremely hot hydrothermal fluids will “alter” the host rock and often cause “argillic alteration” at surface and convert the host rocks into a variety of clays.

The ”porphyry stock” is the structure/chimney through which these ultra-hot and highly pressurized hydrothermal fluids will transit in their way towards the surface. In the case of porphyry structures, if there is molybdenum present (as molybdenite), its melting point is so high that it is the first metal to convert to a solid way down deep as these fluids cool and solidify. Later the copper and gold will solidify higher up in the structure often within faults or veins.

When Auryn’s geoscientists were doing their “ridge crest sampling” on the southern downslope off of the ADL plateau, they discovered a 3.6 Km (north to south) by 1.2 Km (east to west) massive area of high-grade moly and copper which they referred to as the “moly anomaly” and the “copper anomaly”. Moly is kind of different. It is pretty much ONLY mined out of copper-moly porphyries. All porphyries are massive, but of the 4 or 5 different classifications of porphyries, the copper-moly porphyries are the most massive.

The hottest part of these structures during their formation is the porphyry stock itself. The moly doesn’t migrate very far from the porphyry stock. It solidifies too quickly. With moly being found AT SURFACE on the southern downslope off of the plateau, this suggests that the centralized “porphyry stock” (the hot spot) was in close proximity thereto. As you get increasing distances from the porphyry stock, the temperature will decline and different types of “alteration” will occur to the host rocks. The moly will hang out with potassium feldspar/orthoclase in the “potassic alteration” zone. With increasing distances from the heat source, you’ll run into types of alteration known as phyllic alteration and near surface you’ll run into propylitic alteration and the argillic alteration we see at the ADL plateau-right where it is supposed to be. The fit of the findings to what is known as the “Sillitoe Porphyry Model”, named after Auryn’s own Richard Sillitoe, is beyond compelling. Everything is where it should be.

I have no clue as to what is going on behind the scenes in regards to any negotiations on the Pegaso Nero porphyry area. At the time of the Auryn-hosted “informational meeting” in Las Vegas several years ago, Maurizio had the permission of Freeport McMoRann (FMX) to use their name as a party of interest. They are the 5th largest mining firm on the planet. He mentioned that there were two other majors kicking the tires at the PN, and that BOTH OF THESE WERE LARGER THAN FREEPORT. Since then, everything went quiet on the Pegaso Nero front. My question is, have the recent stellar findings above the PN where Auryn is developing the DL2 Vein, DERISKED the PN project enough to get a major miner to accept Maurizio’s terms in exploring this deposit. Porphyry deposits are the most highly sought after deposit type in mining. They are GIGANTIC but of moderate grade. The average grade of gold being mined in a copper-gold porphyry is 1 gpt gold. The average copper grade being mined is 0.6% copper.

You might recall that at the DL2 Vein, there was pretty much no copper found near surface which is the norm. Near surface copper tends to get oxidized and dissolved in acids resulting from the oxidation of pyrite and it ends up piling up in SUPERGENE ENRICHMENT ZONES at the location of the historic water table often in the form of a bluish-colored “BORNITE” version of very high-grade copper. All of a sudden at level 3, that of the Antonino Adit, bluish-colored BORNITE was ubiquitous and the copper assays came back at a very robust 4.5% copper.

The first time we saw all of this bornite is when Maurizio hustled up the mountain and did an interview in front of the cameras. For some reason, the audio was removed shortly after the interview was posted. A similar occurrence happened when Richard Sillitoe spent 4 and a half days on site at the ADL. His report was immediately labeled “top secret” and remained an “in house report”.

I personally would have thought that a deal would have been cut by now between Auryn and a major to explore and develop the PN deposit. To get a deposit like this into production takes a very long lead time and it seems to me that it might be a good idea to get that clock starting to tick ONCE THE PROJECT HAS BEEN DERISKED ENOUGH SO THAT A MAJOR MIGHT MEET MAURIZIO’S TERMS WHICH ARE NO DOUBT VERY DEMANDING.

Yes, a little strange. This mine is actually in US’s back yard. I know this because we were both at one of the last annual meetings held by CDCH, not far from the mine. ![]()

Kennecott Copper Mine, located in Bingham Canyon, is the largest open-pit mine in North America. It is known as the “Biggest Pit in the World,” because it is the largest man-made excavation in the world. It covers about twenty-seven thousand acres, is half a mile deep , and two and a half miles wide.

It’s a copper moly mine. I wonder what an overlay composite on the PN would like. ![]()

![]()

As the deepest open pit mine in the world, the Bingham Canyon mine is quite impressive. The mine has been in production since 1906, so CS was probably right! ![]()

The Bingham Canyon Mine’s annual production rate is estimated at 300,000 tons (272,155 met ton) of copper, more than 10,000 ton (9070 met ton) of molybdenum, and 150 ton (136 met ton) of gold and silver annually.

(Kennecott, https://kidadl.com/facts/bingham-canyon-mine-facts-know-more-about-utah-s-copper-ore)

WOW!

EZ

July can’t come soon enough! 3 months a lot should be happening. If we have a signed mou maybe a signed JV by then. After all our new members need to get paid.

Some here would like to have time pass a little slower as age becomes a factor, lol.

Hi Done Deal,

I think the important takeaway is that nothing was about to happen UNTIL Auryn, firstly, located the DL2 Vein IMMEDIATELY BELOW WHERE THE ARTISANAL MINERS CEASED THEIR MINING OPERATIONS, secondly, their samplings at this location corroborated the off the chart HISTORICAL SHIPPING GRADES of the artisanal miners. Thirdly, they had to complete the Antonino Production Adit in order to get that high-grade ore up to the surface.

Once that was done, all of a sudden, the MEMORANDI OF UNDERSTANDING (MOUs) and TERM SHEETS land from “SEVERAL” industry professionals. These mining professionals needed the project to be DERISKED. Remember that 1-in-1,000 stat from the World Gold Council? Only 1-in-1,000 junior explorers will ever make an economic mineral discovery and successfully get it into production. These industry professionals wanted us shareholders to shoulder those ULTRA-HIGH RISK LEVELS back when they were on the table. Now when those ULTRA-HIGH RISK levels have been mitigated, then they show up for the ULTRA-HIGH REWARD phase.

Those buying the “concentrate” from Auryn/Medinah will make good money from that endeavor. Don’t think for a minute that they haven’t noticed that they could make a heck of a lot more money in the market than in trading the metals. The share price of Medinah, in conjunction with their 24% ownership of the ENTIRE ADL MINING DISTRICT, values the ENTIRE ADL MINING DISTRICT at $20 million. They might spend 10-times that in the first year or two of production. Their problem is the NONCIRCUMVENTION AGREEMENT attached to the NON-DISCLOSURE AGREEMENT they had to sign forbids them from market participation until their deal is disclosed publicly. They obviously hold MATERIAL, NON-PUBLIC INFORMATION.

Now that’s what you call “reading the writing on the wall” - and straight from a person who learned some valuable lessons from the Fruta del Norte - as Brecciaboy said, it was all right there in front of everybody’s eyes, right there on the website, every step of the way, people either could not or would not put the pieces together!

Could Auryn be the next Aurelian or even better? We have the Gold over 130 g/t , Gold price at almost 2000 oz, Copper porphyry, Mesothermal veins, silver, infrastructure, and a great new addition of deal cutters. Exciting times ahead!

I think Brecciaboy commented (way back) that the ADL is on the same geologic trend as the Fruta del Norte? If not, I think for sure there are other mines to the north of the ADL that are on trend.

I think it is highly unlikely the ADL will ever be open pitted given its proximity to Santiago. Just too close to shred a hilltop. I sure the folks in Lampa would sharpen their pitchforks as well. I’m expecting continued underground mining in this Mining Play.

What I would like to see: Dividends. Simple cash dividends. There’s gonna have to be a lot of meaningful production to repay our 0% interest benefactor first. But my shares remain in the sock drawer waiting for this event. I’d say we are 3 more years out before this happens. I’m either wrong or realistic.

Also, fun fact, I finally completed my divorce. She got the house, I kept my brokerage accounts. ![]()

Soooo AUMC would be trading at a billion market cap? Quite the colossal leap from a shoe string project with no proven resources let alone reserves, two false positive claims of hitting the DL Vein, no formal assays, no mine plan ect ect ect…to a $1B+ market cap company, within the 15 largest mining co’s in the world…

This is exactly why I give guys like BB flack…not only has he been wrong for 20 years (as in never once has there been an accurate prediction over two decades) but the shamelss optimism doesn’t benefit anyone as it sets unrealistic expectations which inevitably lead to poor investment decisions.

Then how would you explain the air fart Shiba? in todays world realistic means squat.