Why wouldn’t they be? Has that been questioned?

Doc,

What are your thoughts on Medinah selling shares of AMNP rather than AUMC to pay off debt prior to the share distribution?

1 Like

While we wait for news of the competition of the floatation plant and/or permit approvals, here is a little blast for the past.

https://www.boletinoficialdemineria.cl/?date=02-02-2026&edition=44365&subseccion=7105#

It appears that the Pangue placer claims are once again available to acquire. Some might recall that Juan use to own those and there was some effort made to develop them at one point in time. I believe a couple of things that stood in the way of development was the presence of very large boulders in the dry river bed, the lack of any water to process the gravels assuming you could get to the gravel with all the big boulders in the way, and environmental concerns. I believe these placer style deposits originated from the Altos De Lipangue mother lode so to speak.

Hi JimmyP,

My hope is that Kevin does not find the need to raise money by selling any of Medinah’s “AUMC” shares at less than $5 apiece. Here are some thoughts as to why I suggest this.

“BACK OF THE NAPKIN” EARNINGS PROJECTIONS AND “MARKET RE-RATES” FOR NEW PRODUCERS LIKE AURYN

I sense that people look upon me as being the somewhat “anal” local historian when it comes to all things Medinah and Auryn. I’ve been around for about 30 years and I can still remember how Medinah’s Professional Geoscientist (“P. GEO”) Gordon House, took me under his wing and for some reason accepted my nonstop barrage of geology questions regarding the ADL Mining District. I can still remember his chiding me that the “Gordon/Lipangue Breccia” was not just a “breccia” (gravel-like fragments glued together in a fine groundmass), it actually qualified as a “Maar/Diatreme Breccia” which is basically a “breccia” that showed evidence of a very high level of explosivity, suggesting it was part of a very large, long-lived, hydrothermal system. This particular system ended up being 91 million years old and showed innumerable phases of mineralization.

It should not be lost upon anybody that the famous Andacollo Copper/gold Porphyry to the north of the ADL, also shares this 91 million year old birth date. Throughout history, Chile’s “EARLY CRETACEOUS PORPHYRY BELT” was thought to have its southern terminus up north by Andacollo or perhaps Llahuin. Now it appears that Auryn’s Pegaso Nero porphyry prospect might suggest otherwise.

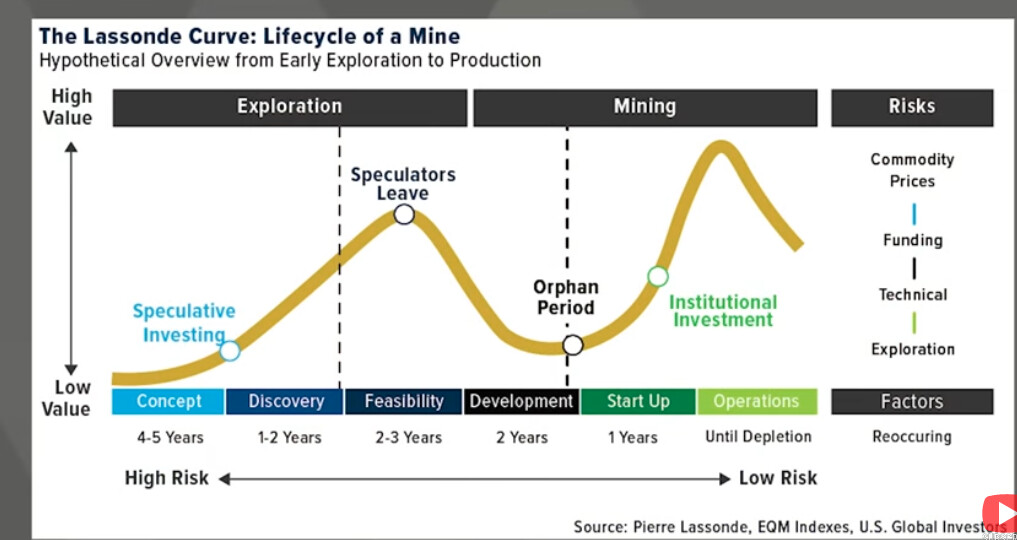

When attempting to predict the future of an investment in a junior mineral explorer/developer/soon to become “PRODUCER”, Pierre Lassonde did a lot of the heavy lifting for us. What he did was study the share price performance of perhaps thousands of junior miners as they migrated through their various stages of development. Many believe that his work, summarized in “THE LASSONDE CURVE”, has made (or saved) perhaps hundreds of millions of dollars for those investors willing to study his work.

His work suggested that the “sweet spot” for investing in the junior miners is to patiently wait until a junior miner irrefutably proves that it has entered into the “CONSTRUCTION PHASE” of a mining project immediately prior to its transitioning into PRODUCTION. Advancing into the CONSTRUCTION PHASE typically involves passing the intense scrutiny of a willing financier capable of performing a much more thorough level of due diligence than most junior mineral investors can perform. The idea is to delegate out some of your due diligence activities to others that are more qualified, besides it’s free.

“THE LASSONDE CURVE” takes into account the fact that once into PRODUCTION it is very predictable that the young “JUNIOR PRODUCER” can successfully ramp up its initial production levels as inevitable operational “bottlenecks” are successfully diagnosed and addressed. A junior miner’s transitioning from doing nothing but spending money raised from the sale of shares, often at steep discounts to already low share price levels, to actually making money represents a tremendous accomplishment especially when the subsequent ramping up of production levels is extremely predictable.

Recall how Auryn’s collaborator Dr. Helmut Mischo predicted how “straightforward” Auryn’s production ramp-up would be after dialing-in the FF plant’s flow sheet. If a junior miner can accomplish transitioning into production at the same time that the metals being mined and sold are trading at or near their all-time high prices, then that’s all the better. “THE LASSONDE CURVE” reminds us that historical share price performance within any given industry tends to repeat itself.

THERE’S ANOTHER “BONUS” INVOLVED AS PRODUCTION RATES RAMP UP

Since the infrastructure has already been established, the incremental additions to production come at a lower ALL IN SUSTAINING COST (AISC) per ounce produced. These “new” ounces of gold being produced during the ramp up are more profitable than the original ounces produced. If the PRODUCTION RATE increases at a rate of “X%” over time, the NET PROFITS might rise at a considerably higher percentage rate. This “BONUS” phenomenon might help explain exactly WHY the share prices of the young “JUNIOR PRODUCERS” tend to outperform by so much. This sector is famous for its share of “10-baggers” amongst new producers.

When you model Auryn’s future earnings using even the most conservative of input variables, you can see how even while operating an admittedly minuscule 100 TPD froth flotation plant, Auryn is still going to make a fortune every year. With the price of gold trading somewhere around $5,000 per ounce, we’ve seen how Auryn could easily make somewhere around $60 million per year once they’ve dialed-in their froth flotation plant in order to maximize recovery rates.

So, once they “cut the ribbon”, as it were, in the next couple of days, what happens next? I’m going to guess that management, perhaps with the aid of their new financiers, are going to move heaven and earth in order to significantly ramp up production in order to maximize this “BONUS”.

With the operational infrastructure already in place, if management were to double their PRODUCTION RATE, they should be able to more than double their profits. If the profits from a 100 TPD plant were, let’s say, $60 million per annum, shouldn’t a 200 TPD plant capacity be able to generate perhaps $130 or $140 million in profits?

Now the question becomes, just how difficult and how long might it take to double the production rate from 100 TPD to 200 TPD and perhaps even upwards from there. With Auryn starting out with over 60,000 Tonnes of ore having been mined, stockpiled and “segregated by grade”, and freshly mined ore constantly being added to the stockpiles, there doesn’t appear to be much of an issue with keeping the froth flotation plant “well fed”.

There is yet another “BONUS” phenomenon that comes into play. With over 60,000 Tonnes of ore already having been mined, stockpiled, and segregated by grade and the number of new operational sites constantly expanding, Auryn will be OPTING to process the highest grade ore first. This is referred to as OPTIONALITY. They get to choose the best of the best from a combination of the pre-existing stockpiled ore and the freshly mined ore. Thus, not only will the PRODUCTION RATE be increasing, while the average cost decreases, but the AVERAGE GRADE will also be increasing at the same time. Recall also that both Rob Cinits of ACA Howe and Richard Sillitoe have opined that BOTH the vein widths and the GRADES at the DL2 Vein are improving with depth. This is a very powerful phenomenon from an ECONOMICS point of view. What we want to gain an appreciation for is the graph of increased earnings as a function of time because of all of these overlapping “BONUSES”.

REVIEWING 3 OF THE “BONUSES” ASSOCIATED WITH TRANSITIONING INTO PRODUCTION

- PRODUCTION RATES, in terms of ounces produced per unit of time, goes up.

- The AISC per ounce produced goes down over time. This is because the infrastructure is already in place to support the incremental increases in PRODUCTION RATES. This increases the “MARGINAL PROFITABILITY” per ounce produced.

- The AVERAGE GRADE being sent to the FF plant goes up with time as more and more operational sites open up throughout time. This also drives down the AISC which is heavily dependent upon “AVERAGE HEAD/MILL GRADE”.

What is important to appreciate are the synergies associated with all 3 of these occurring SIMULTANEOUSLY. This is what Pierre Lassonde noticed.

In mining operations, there is usually one stage of a multi-stage process where “bottlenecks” might appear. Once you diagnose them and successfully address them, then this opens up a runway to ramp up production until the next bottleneck appears and is addressed.

Auryn has listed out several of their new operational sites. Many of these will involve mining from the surface downwards. This suggests that they will be mining near surface “oxide ore” at least for awhile. This “free-milling” ore is typically processed in a manner vastly different than, and easier than, how a sulphide ore is processed via froth flotation. I’m going to guess that the design engineers have already incorporated into the plan locations where oxide ore will be processed alongside the sulphide ore.

A BASECASE SCENARIO LAYERED OVER WITH VARIOUS “BONUSES”

My “basecase scenario” has input variables including an FF plant throughput rate of 100 TPD, an average head/mill grade of 0.5 ounces per tonne (15.5 gpt), a POG of $5,000 per ounce, an AISC of $1,000 per once, an FF plant “recovery rate” of 80%, and 330 workdays per year. When you do the math, Auryn should be able to generate about $56.7 million in pre-tax earnings once the commissioning phase of the FF plant has been completed.

If Auryn can ramp up their sulphide ore production rate to, let’s say, 125 TPD, then that $56.7 million becomes about $70.9 million. If they can increase that “AVERAGE GRADE” of 0.5% OPT by 25% to 0.625 OPT, then that $70.9 million figure becomes about $87.59 million. If they can get their AISC down 10% to $900 per ounce from $1,000 per ounce, then that $87.59 million figure becomes about $90 million in pre-tax profits per annum. Thus, a few small incremental gains, when layered upon each other, can make quite an improvement to the bottom line.

The ultimate goal of any junior miner is to get their mineral deposit into PRODUCTION. Many are aware of the statistic that only approximately 1-in-1,000 mineral deposits will ever get into production. A perhaps even more sobering statistic is that for that “lucky” 1-in-1,000 junior “producer”, it now takes an average of in between 17 and 24 years from the commencement of exploration activities to that first day of production. Now you can appreciate why entering into the CONSTRUCTION PHASE represents the “sweet spot” for an investment in this sector.

Due to the rarity of this accomplishment and the inordinate amount of time associated with accomplishing it, the market tends to give a significant “MARKET RE-RATE” to the share price of a new “junior producer”. While it’s true that the ultimate goal of a junior miner is to enter into PRODUCTION, there are some secondary goals also. One is to enter into production WITH AS FEW SHARES ISSUED AND OUTSTANDING AS POSSIBLE. This way the all-important financial metric of EARNINGS PER SHARE is maximized. Share prices in any sector tend to trade at certain industry-standard “multiples” of EARNINGS PER SHARE. In the mining sector the average “multiple” is 30.1.

Another secondary goal is to enter into production with as few readily sellable shares contained in the “float” as possible. Auryn managed to make it into production with a tiny number of shares outstanding, 70 million, and a microscopic number of shares contained in its “float” i.e. about 7 million. What these accomplishments do is to maximize the expected “MARKET RE-RATE” associated with making it into production.

AURYN’S MOST NOTEWORTHY ACCOMPLISHMENT MIGHT NOT BE RELATED TO GIGANTIC PRODUCTION RATES; THEIR CLAIM TO FAME WILL MORE LIKELY BE CENTERED ON THEIR ENTERING INTO PRODUCTION WITH ONLY 70 MILLION SHARES OUTSTANDING AND A “FLOAT” OF ABOUT 7 MILLION SHARES

This particular “BONUS” puts the other ones to shame when it comes to the provision of SHAREHOLDER REWARDS. The crux of “THE LASSONDE CURVE” is that the junior miners able to achieve all that is necessary to transition into production predictably receive a “MARKET RE-RATE” from the investment community willing to pay more per share for having made these accomplishments.

The magnitude of this “MARKET RE-RATE” can be increased if management was able to minimize share structure dilution during the journey towards production. The financial metric to focus on is EARNINGS PER SHARE. The lower the number of shares issued and outstanding, the higher will be the EARNINGS PER SHARE given a certain level of TOTAL PROFITS.

Ideally management will hold a large percentage of the number of issued and outstanding shares in a “RESTRICTED” format. These “RESTRICTED” and/or “CONTROL” securities bear resale restrictions due to a rule referred to as “RULE 144”. This protects smaller shareholders from management selling large blocks of shares that might depress share prices. With Auryn having only 70 million shares issued and outstanding and about 7 million shares in its “float”, one might expect that any upcoming “MARKET RE-RATE” might be significant. When management holds a significant percentage of the “issued and outstanding” shares, their financial incentives tend to co-align with those of the smaller shareholders. Auryn management holds approximately 62% of the number of shares “issued and outstanding”. The average industry-wide is probably around 2 to 3%.

IN A SENSE, WE’RE IN UNCHARTED WATERS IN REGARD TO AURYN

In 44 years of investing in the junior miners, I’ve never witnessed a CEO, like Maurizio, being willing to advance all of the cash needed to put the project into production while charging no interest. Auryn was thereby able to circumvent massive levels of share structure dilution by not needing to sell shares to the public in order to fund development activities. I’ve never seen a junior miner with a “float” of 7 million shares.

I’ve never seen VEIN GRADES that would rival what Auryn found at level 3 of their DL2 Vein. Auryn’s qualifying for a debt financing from an institutional investor charging only “SOFR plus 4%” is extremely atypical. I’ve never witnessed a young “junior producer” able to time going into production at a time in which the prices of the 3 metals being mine and sold are all trading at or near their all-time high prices. I’ve never seen a junior producer able to net nearly $4,000 per ounce produced. It’s going to be interesting to see just how much of a “MARKET RE-RATE” Auryn’s market will grant it.

12 Likes

Thanks for your response doc. How do you think the AMNP shares that Medinah owns will be handled?

1 Like

You can and should and have jumped up and down, celebrating the “tight share count” (post the massive reverse split diluting all investors by 95%). This tight share count is a result of NOT pursuing the steps that all of the other 1000’s of junior explorers/developers pursued while issuing shares. This distinction has been key to your thesis: why issues 100’s of millions of shares when they can just bootstrap an operation. Fair enough.

However, your attempt to create any relevancy or comparison to the Lassonde Curve or industry average P/Es are bizarre. The ONLY reason why the “construction phase” is so parabolic is because those companies actually explored and developed and paid for feasability studies to understand the grade/ounce and develope a mine plan. AUMC did NONE of those things. They just magically drop into the best part of Lassonde Curve while not doing any of the necessary work? That’s not how it works for very obvious reasons.

Despite your hunch of the highest historical grade WCD (based on a single sample taken directly from a vein), the market will NOT be so gracious. The market isn’t going to assign a PE of 30 (which is way too higher either way) unless they believe there is more than 30 years of mine life, also for obvious reasons.

Talking about doubling production before the first phase is even completed is a very consistent trend/habit of your over the past several decades. It has not worked well in the past but its your perrogative to to repeat the pattern. As Mike Gold pointed out, there is a high likelihood that the 60k tonnes is from previous mining at indeterminable grade. Given that neither you nor anyone else could calculate how 60k tonnes of recently mined ore could be stockpiled (because the math doesn’t work), this is a pretty solid presumption.

None of the above means that AUMC can’t over time grow into at $350M market cap ($5) with a lot of luck and solid execution, but even mentioning that as a reasonable short term probability means that you aren’t familiar with the profile of other junior miners trading at the valuation or your following your previous optimistic “trend.” With no resource, a junior producing 5-10k ounces trading at over $250M doesn’t exist. Prove me wrong. Soma Gold, which I’ve mentioned before is probably the best comp as it relates to the capital structure (insiders own most), potential size/scale. Soma trades at at $250M market cap now but they are forecasting 40k ounces and have a resource (not a huge one).

AUMC has never mined anywhere near 100tpd. The stockpile can definitely fill some gaps but the economically feasible grades aren’t anywhere near 30k let alone 60k tonnes. But there is already talk of ramping production!

This is a bootstrap, chase a vein, very small scale producer with no defined resource. With the price of gold at these levels, they might be able to generate up to $25M in cash flow over a long period of time if they are running at nameplate capacity. There’s nothing wrong with that outcome. Maybe consider breaking the trend by settling projections that are actually attainable? If I turn out to be wrong in my “cautious guidance” I’ll be more than happy to own it. I can only ask that you are willing to do the same, this time.

Still feels like early march to kick off commissioning (assuming they get their permit) but they are moving at a quick pace. Easier to do for a plant of this size but still good work on their end.

1 Like

Don’t be a hypocrite. You can’t scold others for making bold presumptions without enough evidence to support it, while you do the exact same above. How can you make this statement with any degree of confidence?

More than half the stockpile is not economically feasible despite having an onsite plant combined with the company openly publicizing having a 60k stockpile…smh

5 Likes

There’s a big difference from claiming there’s 60k tonnes of high grade stockpiles, which AUMC had publicly refuted, and my assertion that more than half are very likely unlikely. The positive spin is based on hope and a long standing, hyperbolic optimism which has been proven incorrect for 30 years: I’m simply saying that it would be highly unusual versus past and present mining if there was a lot of high grade tonnage. They’ve never had a lab making it extremely difficult to effectively sort and, they’ve spent A LOT of time chasing very elusive veins (read: lots of barren rock before ever finding anything).

My main point: it seems very “inconsistent” to praise a lack of , recent dilution for AUMC (not MDMN) which was only possible b/c they didn’t develop the assets. Claiming that AUMC should be comped to the miners who put in the time, effort, and money is, pretty insane although not at all surprising.

I appreciate that many of the long term investors are looking for a quick home run. Nobody is in their 20’s, let alone 40’s anymore. Unfortunately “hope” is not a great catalyst.

1 Like

If I didn’t own a stock, would I even waste my time? I’m a busy man.

How else are sane people supposed to approach a poster who habitually attacks another well-informed and well-intentioned poster, does not own any shares of the stock, and has posted many times before that it is not possible for this company to succeed because it has not drilled a thousand holes? You’ve recently softened, but that don’t count - we remember.

7 Likes

If you go back to a 2024 Auryn Shareholder Update, it reads as follows:

“To further understand the potential of our site, our team is planning a comprehensive exploration effort. This will involve correlating data with nearby mining districts such as BRONCE PETORCA (to the north) and LA FLORIDA (to the south), specifically targeting regions at 1,550 meters below the Antonino level.”

In other words, Auryn is suggesting that these 2 mine sites are the most representative of what to expect in and around the Fortune vein.

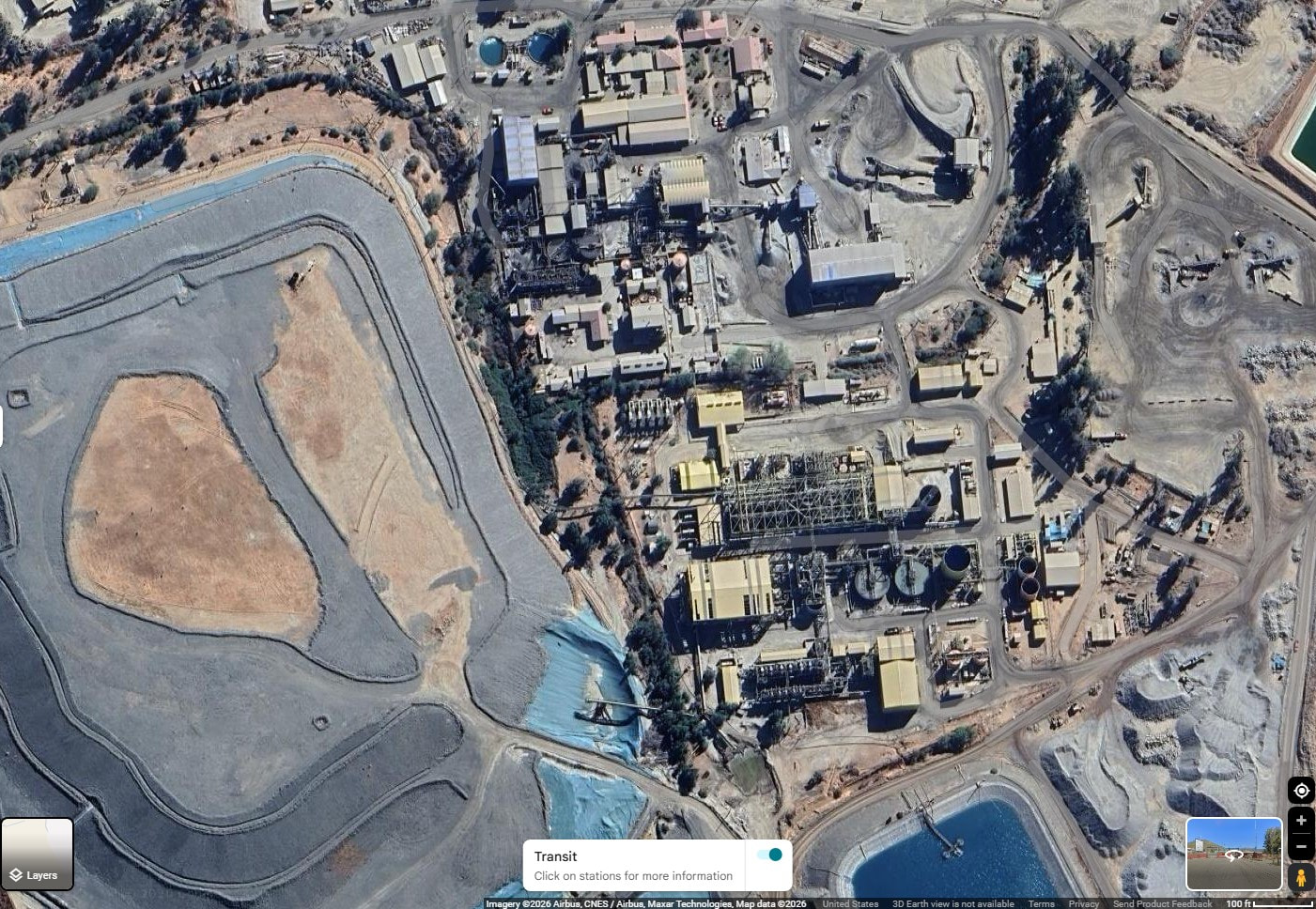

I have attached a couple of photos of the mining processing facilities at those 2 mines which gives you an idea on just how big they are and how far Auryn still has to go to reach some big numbers.

5 Likes

Brecciaboy has made the following points in multiple posts that have continually been met with derisive comments and attempts to dissuade new investors. Based on rigid standard mining practices this viewpoint by BE is quite valid and reasonable. However, bootstrapping a mining project is an Anomaly from this rigid viewpoint and takes a considerable investment in time.

In simple terms, the Lassonde Curve explains why a company can be physically successful while it’s stock price is struggling. As a company moves from finding gold to actually building a mill, the stock often hits a bottom for two main reasons, dilution, and boredom. Building a mine is incredibly expensive and during construction there are few flashy new discoveries to keep speculators interested. Once the mill is finished and the company starts producing gold, the stock often returns to its previous high valuation because the project is largely de-risked, new investors arrive and cash flow produces a rerating.

The Orphan Period represents the point of maximum financial strain and investor boredom, while the Production Phase represents the reward for those who survived the dilution.

Auryn Mining’s approach at the Altos de Lipangue district demonstrates how a company can bypass the deepest part of the Lassonde Curve’s reward “bottom”. Instead of issuing millions of shares to build a massive complex, Auryn secured a targeted $4 million financing agreement with Strategic Investments S.A.C. to build it’s flotation plant. Rather than a decade of studies, Auryn advanced the Fortuna Project toward ore production, completing its first official blast in the Northwest drift in January 2026. Because the share count remains low, any increase in the company’s value translates directly into a higher Price Per Share (PPS). There is likely a Free Cash Flow (FCF) re-rating resulting in the market seeing a clear, short path to revenue. With successful bootstrapping there is a potential for cash distributions or dividends much earlier in the mine’s life cycle because there isn’t a massive mountain of construction debt to pay off first. Shareholders are anxiously staying tuned and pleased to finally see the rapid progress being made.

EM

7 Likes

“ ….. 1,550 meters BELOW the Antonino level.”

Just connecting the dots, I’m just guessing MC saw some GOOD things 1,550 below the Antonino level? If so, then him subsequently getting excited about building a mine to “chase veins” should bode well.

Probably nothing.

1 Like

Anyone know anything about this site? Valid? I sent an email to the contact email address two weeks ago with no response yet.

3 Likes

Yes, MedinahReceiver.com is the website set up to inform us about the Nevada receivership instituted to pay off MDMN’s debts and then distribute our AUMC shares to us.

3 Likes

Yes, and some here can actually make conclusions between two polar opposite extremes, offering a very wide landing zone. Your assertion is just as baseless as one claiming the entire 60k pile is high grade. You are claiming more than half not only is not high grade, but that it is not even economically feasible. As in, more than half that pile is worthless. So MC is publicizing that we have 60k stockpile knowing full well that less than half of it can actually be run through the plant.

Got it. Thanks again for confirming.

Once again. Personal attack vs. being able to articulate where I’m wrong in my analysis. Scary stuff. I didn’t realize that owning shares in AUMC was a prerequisite for participating. Im sure you are a busy guy! My spending 5 minutes here a couple time a week is not too taxing and I’ve been involved in one way or another long enough, that it remains interesting to follow (but cleary not invest). I’m counting on you to remember.

FWIW, I’ve NEVER claimed that a lack of holes guaranteed failure. What I have said is that a lack of resources makes the journey infinitely more difficult. Based on the progress made over the past TEN YEARS, this point is irrefutalbe. I also never claimed that AUMC can’t make money without a resource BUT the risk profile is massive vs a miner who knows “where to mine.” This risk will be discounted in any future valutation as will the lack of a resource. We can revisit these last two points down the road.

1 Like

Good to see you back MG,

Speaking of a little blast from the past, here’s another eyeopener to have with your morning coffee from BB. I wonder how many remember it … I sure do!:

…. I think we tend to forget how tiny this investment forum is in real terms. Could you imagine if a couple of whales came in and started feeding? I do sense some empathy coming out of Raul. He knows how frustrated we are. He openly admitted that management HAS HAD the ability to distribute our AUMC shares since last Dec. 15 but it wasn’t “the appropriate time”. His earlier reply to a shareholder stated that we’d know more “at the appropriate time”. His most recent communique to a shareholder contained this:

“We have spoken to legal counsel and we can proceed with allocation of AUMC shares since December 15,2019, however, we have not done so given we are waiting for work to be completed. As soon as it is possible, I will be updating everybody through our website, please check the news update section. I can only say that any delays on updates with respect to AUMC shares owned by Medinah is with the intention of benefiting the shareholder.”

We didn’t learn much more in the second communique other than “the appropriate time is when certain work is completed”. But he also stated that any perceived delays are with the intent of benefitting the shareholder. My inference is that when he rolls out whatever he is going to roll out, he wants to get the biggest bang for the buck he can for all of us. I think this might tie back in with the incentive to move the share price up prior to any need to raise funds out of the market for these lofty goals of Maurizio. A much higher share price would also give management more strength at the bargaining table when cutting JV deals with any majors. My recommendation would be not to entertain any deals for the early gold production opportunities at least until the production rates have increased and then plateau’d out.

It looks like the appropriate time is when certain work is completed. Management is strategically aligned with shareholders. (hi-lighted text is mine)

EM

2 Likes

Yeah, there’s literally NO marketing of this company going on - just wait until it hits the fan!

2 Likes

If anyone knows, what can the flotation plant be expanded to beyond the 100 tons per day?

Hi EZ,

Thanks for the re-post of that version of “THE LASSONDE CURVE”. The figure can be accessed on post #253 made on Feb. 4. The graphics are well done. The concept is extremely simple, junior explorers/developers tend to go through common stages of development and the ultra-lucky ones may even get their mineral prospect into production.

The “curve” is basically a forward-leaning “CAPITAL N”. The left vertical component describes how a junior with a decent drill intercept will witness its share price go up a measured amount. The excitement dies off soon thereafter and investors realize that they’re still a minimum of 5 or 6 years away from production and during that time period a massive amount of SHARE STRUCTURE DILUTION is going to occur. The price gains from the initial reaction to decent drill results gets erased and the share price returns back to where it started out before the drill program commenced. The main difference between pre- and post-drilling is that the share structure has been significantly diluted because a bunch of shares needed to be sold in order to fund the initial drill program. Phase 2 of drilling is going to involve the sale of yet more shares at these low share price levels.

What the “LASSONDE CURVE” is telling us is to not even look at investment opportunities related to the left-hand vertical portion of the “N” or the downward line in between the left- and right-hand vertical portions of the “N”. The downward slanting line coincides with “the orphan period” after some investors took their profits and naive investors held tightly to their shares as their ownership position was getting diluted out from underneath them.

The “LASSONDE CURVE” asks us “What’s the hurry”. Just wait until the miner under study irrefutably proves that it has entered into the “CONSTRUCTION PHASE” immediately prior to PRODUCTION. This way you can evaluate the SHARE STRUCTURE DILUTION that the miner under study has endured during the “orphan period” after it occurred WITHOUT RISK. What you want to do is to list out the junior miners that you have identified as having already entered the “CONSTRUCTION PHASE” and got it successfully financed, and then rank them against each other as investment opportunities.

The ranking data includes: the number of shares issued and outstanding at the time of entering into production, outstanding debt, the “float” of readily sellable securities, the average grade being mined, and the ALL IN SUSTAINING COST to produce each ounce of gold being sold. The RISK has already been all but removed as production is entered into. You don’t need to cross fingers and hope that management didn’t dilute the heck out of the share structure during the various phases of drilling and during the execution of a series of expensive and time-consuming feasibility studies.

The right-hand vertical component of the CAPITAL “N” is what it is. The share prices tend to take off like a rocket upon entering into PRODUCTION. The big RISKS are now in the rear view mirror except for “operational risk”. If the company under study has an incredibly low number of shares outstanding, an incredibly low “float”, ownership of 100% of the assets, extremely high GRADES, a low amount of debt, and a low AISC, then that particular “rocket” is likely to have a lot more fuel in it then the others and the share price will likely ascend to very high levels. If, by chance, the price of the metals being mined and sold just so happens to be trading at or near all-time highs, then the share price advance will be augmented that much more.

Somebody on THEMININGPLAY recently introduced a junior mineral explorer/developer that is about 60-days ahead of Auryn’s schedule within the CONSTRUCTION PHASE. This affords us a wonderful opportunity to test out “THE LASSONDE CURVE”. Auryn has entered into the CONSTRUCTION PHASE with only 70 million shares outstanding, fully-diluted, and 7 million shares within the “float”. They own 100% of the mineral assets. This other company has 921 million shares outstanding, fully-diluted, about 700 million shares within the “float”, and they have had to take money from a royalty streamer and they no longer own 100% of the production from the mineral assets.

Interestingly, upon entering their CONSTRUCTION PHASE, this other company’s share price ascended 10-fold while within this “sweet spot” of “THE LASSONDE CURVE”. This is despite the enormous number of shares outstanding and the enormous “float”. This company has done a lot of promotion in the past and Auryn has done NONE. The question becomes, once Auryn gets into PRODUCTION and tells their story, what kind of a share price reaction (“MARKET RE-RATE”) might they expect with so few shares outstanding and such a tight “float”.

When the price of gold is near $5,000 per ounce and the ALL IN SUSTAINING COST to produce each ounce is about $1,000, THERE IS NO QUESTION WHATSOEVER ABOUT THE “ECONOMIC FEASIBILITY” OF THE PROJECT. In a situation like this, there are a lot of junior miners that wish they’d have done a lot less drilling in order to block out ounces of MINERAL RESERVES/MINERAL RESOURCES and sold a lot fewer shares to determine the “OFFICIAL” ECONOMIC FEASIBILITY NUMBERS.

At the end of the day, the ultimate goal of a junior miner is to do what is necessary to get into PRODUCTION WITH AS FEW SHARES ISSUE AND OUTSTANDING AS POSSIBLE. All of those statistical numbers like INTERNAL RATE OF RETURN and NET PRESENT VALUE will be readily available once PRODUCTION commences. These will be 100% accurate and not “projections”. When the ECONOMIC FEASIBILITY of a mining project is a total “no-brainer”, I’d rather have a lot fewer shares outstanding, as an investor, than a 250-page book with a bunch of statistics.

Now, if the price of gold is $1,050 and the AISC is estimated to be $1,000, then that junior needs to fully drill out the deposit just to prove ECONOMIC FEASIBILITY. It’s share structure is going to be decimated, but that’s life. That’s better than spending $30 million on a mine only to learn that it’s a money-losing proposition. There is a trade off between “geologic certainty” obtained in determining “economic feasibility” by drilling and SHARE STRUCTURE damage. Drilling a hole 300-meters below the surface in an area which won’t be mined for 25-years doesn’t make a lot of sense when “economic feasibility” is a no-brainer. You can always drill later and pay for it with CASH FLOW instead of the sale of dirt cheap shares TODAY.

3 Likes