So anyone owed money by mdmn has until Feb 16th to be on the list. Since mdmn is worthless the only asset is AUMC ownership represented by AUMC shares, I would assume creditors are after money reimbursed meaning the settlement would require sale of the only asset which is AUMC shares at current value?

2 Likes

Thanks Mike. I didn’t think the 60k tons being referenced would be 95%-98% barren rock. Its certainly not 60gpt either, but nobody was suggesting that. Even if it collectively averages 3gpt, that’s a nice sum of money.

Also, nice to see you back posting.

1 Like

Yes, judge, that’s what I was trying to say.

1 Like

As far as the most recent update from Auryn dated 1/16/26, I think we need to focus in on the first 2 accomplishments cited under “HIGHLIGHTS” at the beginning of the update. They were:

“January 8, 2026 – FIRST OFFICIAL BLAST (my emphasis) completed in the Northwest drift at Fortuna, MARKING THE TRANSITION INTO ORE PRODUCTION (my emphasis) and

December 2, 2025 – Successful connection of the 1847 level to the 1913 level, improving ventilation, access, efficiency, and underground safety.”

You might recall a recent press release in which Auryn noted that they had retained a “SUB-LEVEL STOPING” contractor. The “SUB-LEVEL STOPING” approach to mining is used for LARGE projects in which the ore body/bodies (plural) are dipping steeply (fairly upright) and the borders of the deposit are fairly well-defined. This is an accurate description for the 7 Main Veins present at the ADL Mining District. You might also recall how the “headmaster” of the San Sebastian University’s School of Mining who has worked with Maurizio on the ADL projects and who was the former “HEAD OF UNDERGROUND OPERATIONS” for the very large El Penon Mine which was discovered by Meridian Gold and was later taken over by Yamada Mining which in turn was later taken out by Pan Am Silver, was quoted as stating that he thought that the ADL Mining District had many of the characteristics of the El Penon Mine, and might share a similar future.

The El Penon Mine is currently being mined at 38 different operational sites. The main differential between the 2 deposits is that Auryn’s is of vastly higher grade and the Auryn deposit has very high-grade copper in addition to gold and silver. The El Penon is mainly a gold-silver deposit. The El Penon Mine is also exploiting about 6 or 7 main veins that are now interconnected via horizontal drifts. This press release offers evidence that Auryn is now transitioning down that pathway. Management’s choice of words “FIRST OFFICIAL BLAST” as well as “MARKING THE TRANSITION INTO ORE PRODUCTION”, although they already have over 60,000 Tonnes already stockpiled, suggests that this is pretty much Day 1 of the new Auryn Mining.

The first phase of a large “SUB-LEVEL STOPING” project is to open up what is referred to as a vertical “ore pass” or “ore bypass”. This is what Auryn accomplished on December 2, 2025 when they successfully connected level 3 at the 1,847 meters above sea level elevation to the old workings known as “the 1,913 level” denoting its relative elevation. Now there is a 66-meter vertical “raise” (ore pass) linking the two. This represents a major accomplishment for Auryn. This project was recently permitted by SERNAGEOMIN. In the most recent update. Auryn cited: “This connection improves ventilation, access, and overall operational efficiency while enhancing safety conditions underground.”

So, the game is officially on as far as the “SUB-LEVEL STOPING” (SLS) project at the ADL Mining District. From here on out, you will notice new operational sites being added incrementally via horizontal “drifts” linking the 7 Main Veins. In SLS projects, the lowest level in a series of horizontal drifts, in this case level 3 or the Antonino Adit, serves a the haulage adit. Blasting is accomplished in the levels above the level 3 and the ore is pushed into the ore pass where it free falls down onto level 3. All of the haulage activities are concentrate here so that the miner does not need haulage equipment, like LHD (Load, Haul, Dump) trucks, at all of the horizontal levels/drifts. The crashing of the ore onto level 3 will also serve to break up the ore and start the “comminution” (crushing and grinding) process.

In observing the dialogue present on the “MININGPLAY” investment forum, I don’t think the average shareholder has an appreciation for the progress having been made to date and just how big of a project that has been undertaken. The progress in the construction of the processing facilities is easy to follow because of the photos on “X” but we need to remember that in parallel to this progress we have seen significant progress in the mining of the ore that is going to be processed in those facilities. The drifting of these horizontal “drifts” also represents “EXPLORATION” and the ability to block out ounces of “Mineral Reserves/Mineral Resources” similar to how diamond drilling does. In this case, the drill holes are gigantic and oriented horizontally.

Another party that has been collaborating with Auryn over the years, Dr. Helmut Mischo of the Freiberg University in Germany, has commented that once Auryn “dials-in” their froth flotation process flow sheet, ramping up the production levels will be very predictable and straightforward. Dr. Mischo has authored, I believe it is 184 scientific articles in the various mining and engineering journals.

With SERNAGEOMIN having already approved the construction of the 66-meter ore bypass, and its successful completion, I don’t think that shareholders should be too concerned about SERNAGEOMIN continuing to approve the various other permits involved in the seemingly never-ending permitting process. Recall that SERNAGEOMIN has partnered with Auryn in delivering educational “workshops” to other members of the mining community including major mining firms. The most recent update also confirms that the “target completion date” for the ore processing facility is just 14-days from the release of the update or 1/30/26.

Below is a link to a short video on “SUB-LEVEL STOPING”. At the 1:25 mark you can see where they refer to the completion of the “opening raises”. This is the 66-meter tall “ore pass” or “ore bypass” I cited that Auryn just successfully completed.

3 Likes

Dear brecciaboy,

Can you please put these sweet lyrics to some gentle music that I and others (not everyone, of course) might use as, you know, a lullaby to get to sleep at night?

Thanks in advance!

– madmen

3 Likes

Hey Done Deal, did you run the numbers again today? $4,845oz ![]()

1 Like

Stracon’s name has to be on a publicized mine plan to start building credibility with the investment community.

You telling us on a message board won’t cut it. You tagged MC as an underpromoter as if its a term of endearment. Medinah needs to liquidate AUMC shares pretty soon. So perhaps he should step on the promotion gas pedal!

1 Like

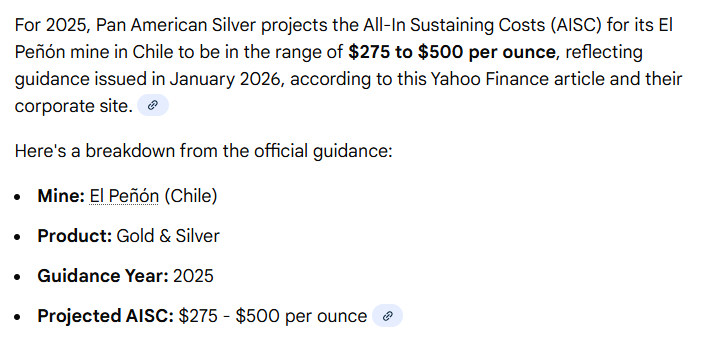

SPEAKING OF THE EL PENON MINE ……

Brecciaboy, it’s not lost on me that in one of your recent posts you suggested the AISC for AUMC should be estimated at 800.00/ounce (down from 1,200.00/ounce). So, I went back to take a look at recent guidance from Pan American Silver (the owner):

So, Brecciaboy, your estimate of 800.00 seems a bit conservative to me - probably taking into account the fact that we’re experiencing a dialing-in process and we’re just getting warmed up.

But, there was ……. someone …… around here who as recently as November, 2025 estimated AISC would be between $1,500-$2,000 per ounce. Be careful who you listen to, that’s all I’m gonna say.

2 Likes

Hey Madmen, I don’t want to put words in the Professor’s mouth, but it seems to me that the more they dig around down there, the more they know where these veins are going and don’t have to GUESS at it. They get further confirmation of the 3D model they no doubt already have.

It’s kinda like how the 30 years’ work of the artisanal miners gave us a nice road map - obtained initially from the data/statistics maintained by ENAMI, but then expounded upon by further exploration work of our own.

But, I’d rather hear the Professor on this.

2 Likes

Quote :

https://finance.yahoo.com/quote/AMNP/?guccounter=1

Website :

While I have my doubts that you will receive any guidance on an accurate ASIC (you don’t even have a precursory mine plan to refer to) for a very long time, that fact that you are looking at El Penon as some sort of benchmark is, to be kind, “amuzing.” You are literaly comparing a wheelbarrow with a Ferrari. FWIW, the ASIC was able to be reduced to this level b/c they dramatically increased their price of silver projections. The silver by-product credits are the main contribuing factor. Per my earlier post, I really can’t wait for these guys to start processing some rock. It will make for some very interesting conversations, revisions, and “clarifications”. But hey, the indistry average is around $1600oz, why can’t AUMC do better then cutting that in half? Maybe they could save additioanal costs buy replacing trucks with donkeys?

The word is AISC, not ASIC - we’re not talking about computer chips here.

I do believe AISC is a function of your geological LOCATION - and that it varies around the world. Nearby mines with the SAME type of mineralization and processing are not just a little bit relevant - in fact, they’re very instructive, although not dispositive. But …… I would think you would KNOW that, right? Maybe not. Didn’t you admit that you’re on the Board of Directors of some exploration/mining firm? (*** mod edit)

Are you the one driving the price of AUMC up to 1.40’ish? Wouldn’t surprise me - but why would a man of your stature invest in something like this. They haven’t drilled enough holes yet, right? So, it’s not fair to say they’ll ever produce ounce number one, right? Hey come to think of it, if that’s the case then the AISC will be ZERO, even cheaper!

Could it be that the very fact that you are here is tacit admission that MC and BB actually have something here? That’s what I’m thinking.

Sure am glad AUMC has 70M shares outstanding, as opposed to approaching a Million. Enjoy - we’ll see who gets the best dividends. You said NONE, EVER - remember?

1 Like

I wouldn’t.

…….but I believe you are trying to infer that geography plays a significant role in determining AISC/costs. Geography can play a role but you may want to double check with the old professor before you go too far down that road. In Chili power costs are high, water is scarce, labor in expensive and unionized, The higher the altitude the higher the AISC. Combined with the lack of mechanization, infrastructure, seasonality and the extremelly small scale of the project any competent analyst would point out that the AISC will likely exceed the industry average ($1600oz) by a large margin. Yes, the high grade nature of the deposit is a big (but only) factor in driving down the AISC but that ain’t going to move the needle anywhere near where you’d like it to.

Same type of processing and mineralization???

To make the analogy eaiser on you, just assume that the wheelbarow is Italian. Same geography but keep in mind that El Penon (the Ferrari) processes 40-50x the daily tonnage of the neat little plant that AUMC is currently building. Think about a highly mechanized operation that has been optimized over decades vs. blowing up some rocks, waiting for the dust to settle while hoping not to lose sight of an extremely narrow vein. I’ll just have to assume (always dangerous) that you understand how the scale of a project bring down costs, significantly. They don’t come any smaller than what we are discussing but put that aside. I’m sure it won’t matter. Did transportation costs disappear as well? They can concentrate the ore and save a few trips but the sliver of a road hasn’t magically become a highway. Killed imminent production at Caren and now we’re debating if AUMC’s AISC should be comparable to the lowest decile producers (let alone if they are able to generate any profit at all).

One might suggest waiting to see if these guys can reach profitable production on a steady state basis before claiming that AUMC is going to be spitting out dividends at industy low costs and historically high grades but that would be so un-Medinah like.

(**Mod note, edits made to remove personal slurs)

I agree! Thanks for continuing your informative posts BB. I have some thoughts I’d like to add to the discussions. Looking at the Oct 2025 up date, it notes that contractor continued upgrades to the Antonino Tunnel and advanced mining work to connect it with the upper-level Fortuna access known as “Fortuna 1913.” This connection is expected to enhance safety, ventilation, and overall mining efficiency while reducing dilution.

My read on the information provided says there is approximately 60,000 tons of lower quality ore available to supplement plant feed over time. Additionally, there is mention of 28,000 tons prepared for processing and ready for the plant at start-up which I take may mean the higher grade ore that will be used after the plant has been commissioned with some of the lower grade ore from the 60,000 ton stockpile. This is somewhat clarified in the next update from earlier this month.

From the latest January 2026 notification; “Approximately 13,000 tonnes of ore are prepared and currently being transported to the plant’s ore stockpile area for use during initial start-up.” I interpret this to mean this is lower grade ore from the 60,000 tonne stockpile to use for commissioning, not the 28,000 tonne higher grade ore to be processed after commissioning. Furthermore, the PR says,

The commissioning strategy remains unchanged. Lower-grade material will be processed during the initial commissioning period (approximately 30 to 45 days) to fine-tune plant performance and recovery parameters before transitioning to higher- grade feed from active mining operations.

If I am correct, it is possible some of the 28,000 tonnes of ore came from the Caren or Merlin IV vein and is higher grade.

Initial Feed Plan: Start-up will utilize lower-grade stockpiles to establish steady-state performance without risking recovery losses. Thereafter, plant feed will transition to production from the Fortuna and Caren projects.

Getting to the production plan, the upper level drift of this single stope is the “Fortuna 1913,” situated at an elevation of 1,913 meters above sea level. The lower level drift is situated 66 meters below at 1,847 meters above sea level. The vertical distance between these two points (approximately 66 meters) defines the block of ore being prepared for extraction via the sub-level stoping method. This orebody (an unspecified horizontal length of the vein) is divided into large vertical sections (stopes). In this instance, it is a single stope, however with expansion to greater depths there will be multiple intermediate levels (sublevels).

Visualize an ore vein (“Fortuna 1913”) that runs some distance horizontally, but also has a great vertical depth that may be hundreds of meters in depth. Think of this single ore vein that has one drift stacked on top of another (the lower 1847 level) with some distance in between. In this instance, there is 66 meters separating the two, but it is a single ore vein running at different depths. BB describes the connection of these two ore drifts as a vertical “ore pass” or “ore bypass”. “The successful connection of these two levels on December 2, 2025, was a critical milestone for establishing the ventilation and safety infrastructure required for active production.” The “ore bypass” isn’t actually pictured, but I think of it more as a spiral decline that is offset from the actual vein being mined. It does not provide high grade ore to be processed.

While 66 meters is on the higher end of the standard range for a single open stope, Auryn’s engineering team and specialized contractor managed the integration under a project plan approved by SERNAGEOMIN.

( January 2026 – Shareholder Update | AURYN Mining Corporation ).

The connection of these levels was specifically cited as a milestone that enhanced safety and reduced dilution, indicating that the 66-meter block is considered manageable with their current design. That’s a lot of ore!

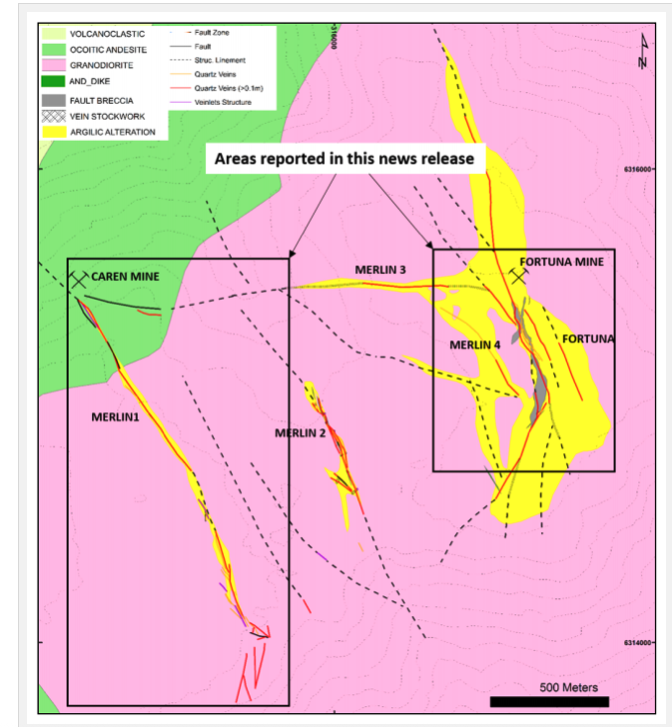

Recall, as disclosed earlier, Ameco Chile SpA (an affiliate of Strategic Investments S.A.C.) is the specialized contractor for the La Fortuna Sub-Level Stoping Project. The “La Fortuna Sub-Level Stoping Project” involves high-grade extraction from vein systems (such as Merlin IV and Don Luis) accessed through the Antonino Tunnel.

During this quarter, we significantly advanced activities at our Fortuna site:

Antonino Tunnel Operations: We retained a specialized contractor who is managing Antonino Tunnel operations as part of the La Fortuna Sub-Level Stoping Project. Current efforts include enhancing tunnel access, improving grade, and ensuring continuous, efficient operations with minimal disruptions.

We are advancing two additional exploitation projects targeting the Merlin IV vein, both in its northern and southern extensions. Each project targets an extraction rate of 1,000 tons of ore monthly, bringing our total authorized production capacity to 3,000 tons per month by the third quarter of 2025.

https://aurynminingcorp.com/april-2025-shareholder-update/

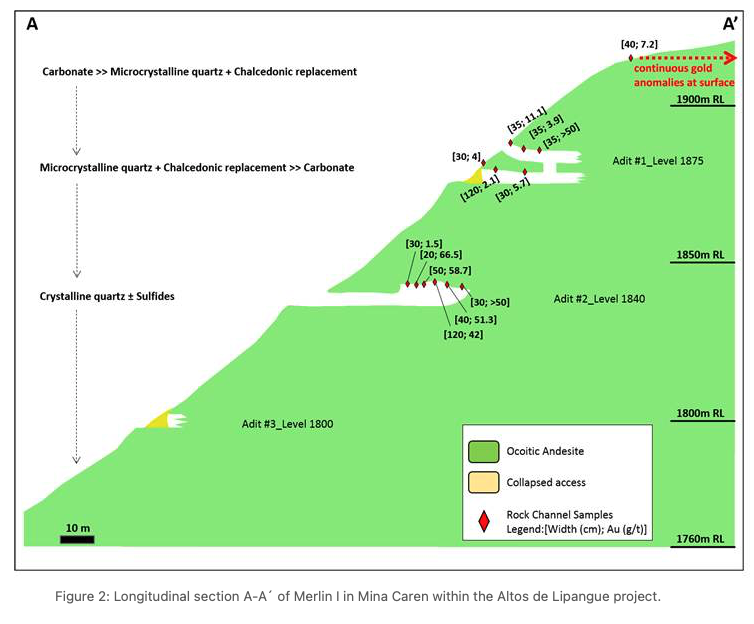

It is worth mentioning that both the Merlin 1 Vein (Larrissa Adit) and the DL2 Vein show “bonanza” grades at the 1,840 meters above sea level elevation. This is an interesting level across the entire ADL. At this favorable sub-level management will likely choose to mine out these areas first. Major veins were first mapped out in a release December 2015:

It is interesting to note the changing composition of the deposit as the depth increases.

Perhaps the Merlin IV is actively being exploited at this same level to see if high grade ore continuity across the ADL is consistent. I think Maurizio has a very well thought out plan to exploit the ADL and is now putting it in action with POG at an ATH, a very opportune time. I think shareholders will not have to be looking back.

EZ

8 Likes

This is what I SAID - look it up.

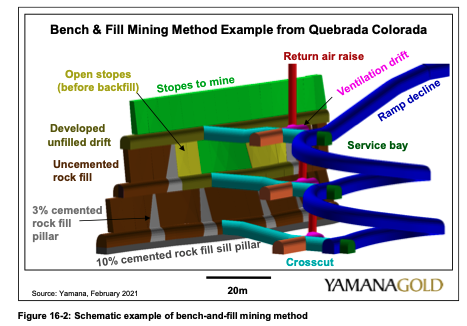

I see what you are talking about here brecciaboy! Look at this layout of interconnected “ore bypass” spiral declines when the El Peñón mine was operated by Pan American:

You can see the stopes mined out next to each “ore bypass” spiral decline. The good high grade ore is “bypassed” and not mined from the spiral decline that grants access to the active multiple stopes being exploited. Here is a schematic that demonstrates this more clearly in a close up from El Peñón when run by Yamana:

Sure looks to me like MC has a clear vision for the mine plan he is implementing. I’m one highly appreciative shareholder of your well researched and instructive posts BB, but I also get a lot out of the contributions made by other shareholders here. I’m looking forward to seeing figures of actual free cash flow (FCF) that will be forth coming in the next year or two as this exploitation continues to expand to greater tonnage of high grade ore being accessed.

EZ

6 Likes

I just put up another post. I should have read your PM Bubba before I posted and included “Nearby mines with the SAME type of mineralization and processing are not just a little bit relevant - in fact, they’re very instructive, although not dispositive.” This should not have been edited out by a moderator!

(**This was not edited out- just a personal comment)

2 Likes

Some buying coming in! Gold ripping again! Plant almost complete! Hopefully we get our shares of Aumc shortly! Stars are aligning perfectly!

5 Likes

Hi MrB,

The analogy between the characteristics of the ADL Mining District and those of the El Penon Mine was made, not by me, but by the FORMER HEAD OF UNDERGROUND OPERATIONS at the El Penon Mine who is intimately familiar with BOTH projects. From a past press release of Auryn:

"On August 12, 2021, a group of professors and students from Universidad de San Sebastian spent the day with our mining team at La Fortuna de Lampa. The visit was multidisciplinary in scope and covered all aspects involved in our project transitioning to a producing mine including infrastructure, continuous mining operations, health and safety, and environmental and sustainability issues. AURYN anticipates several reports to come from this once all the analysis is complete. In the meantime, Luis de la Torre, one of the professors who visited, offered the following comments:

“The ore extracted and stockpiled from the OLD AND NEW WORKS [NOTE WHERE SOME OF THE 60,000 TONNES OF STOCKPILED ORE CAME FROM, KEEP IN MIND AT THIS TIME (2021) Auryn HAD YET TO INTERSECT THE MUCH HIGHER GRADE LEVEL 3] on AURYN’s La Fortuna de Lampa mining project strongly reminds me of the ore from El Peñon Project, owned by Yamana Gold Corp. They are very similar to the color and rock quality of the ore I personally observed during my time working on the development of El Peñon. I have the firm belief that once La Fortuna de Lampa project goes into production, and a correct evaluation of the entire project is achieved, it will be a mining operation with very similar characteristics of El Peñon.”

Luis de la Torre

HeadMaster

Civil Mining Engineering

Universidad de San Sebastian"

Imagine that, the ADL is likely to be: "a mining operation with very similar characteristics of El Peñon.” Note that Baldy suggests that he knows more about the ADL Mining District and the El Penon Mine than this head of the Civil Mining Engineering Department at the University of San Sebastian, who served as the HEAD OF UNDERGROUND OPERATIONS. Why doesn’t that surprise me?

SOME CONTEXT: From 1940 to 1970, the artisanal miners averaged 64 gpt gold mining the “old works” at levels 0,1,2, level “N”, and level “S-1” with no technology. Their discards from pre-sorting, held TODAY in “tailings piles and dumps” are running at 14 gpt gold in many places. The discards are running at 3.5-times the average head grade being mined today worldwide in similar underground vein deposits, like El PENON,for example. Let’s look at that again. The discards in place at the DL 2 Vein from areas mined with a much lower grade than where Auryn is currently mining (level 3) have a much higher grade than the worldwide average being mined today. These discards are stored at the entrance to the adits accessing levels 1 and 2.

The DL2 Vein has a surface strike length of 1,000-meters. It has been successfully traced to a depth 0f 700-meters. Assuming an average vein width of 1-meter and “granodiorite’s” SPECIFIC GRAVITY of 2.7 Tonnes per cubic meter, this represents 1.89 million Tonnes of ore. Based on Auryn’s FF plant’s INITIAL nominal throughput of 100 Tonnes per day or about 33,000 Tonnes per year based on a 330-day “work year”, this represents about 58 year’s worth of mine life for just this one of the 7 Main Veins present.

Both Rob Cinits (ACA Howe) and Dick Sillitoe have commented that BOTH the GRADES and VEIN WIDTHS are increasing with depth at the ADL. De la Torre’s comments were made BEFORE they hit the huge grades at the new level 3, i.e. that of the Antonino Adit. Auryn’s exhaustive surface trenching program (over 1,600 samples) revealed over 5,000-lineal-meters of mineralized veins that made it all of the way to surface, many did not as we witnessed during the drifting of the Antonino Adit. All of these veins are related "SPATIALLY and TEMPORALLY. They comprise a homogenous and somewhat predictable “VEIN SET”. There are “bonanza” grades at similar depths from vein to vein (about 1,850 masl). The Merlin 1 Vein (Caren Mine) assayed out at an insanely high average grade of 26.9 gpt gold AT SURFACE (volume weighted average=super accurate).

Auryn did NOT find the need to sell hundreds of millions of shares in order to fund a diamond drilling campaign and a series of feasibility studes over the course of perhaps 4 years, in order to establish estimations of MR/MR, AVERAGE HEAD GRADES, an estimated mine life, and the ECONOMIC FEASIBILITY of the project at a time in which all 3 of the metals being mined are trading at all-time high levels. The “ECONOMIC FEASIBILITY” of the project was a no-brainer. If you can’t recognize the good fortune that Auryn has realized by taking this approach, involving Maurizio advancing all of the cash needed to put the project into production, and thereby avoiding all of that SHARE STRUCTURE DILUTION while maintaining 100% ownership of the project, then there’s nothing I can do for you.

FACT: The two main parameters used for estimating AISCs are AVERAGE HEAD GRADE and whether or not the miner has its own ore processing facility on-site and can avoid expensive “tolling” arrangements. GRADES vary inversely with AISC. A miner, LIKE AURYN, mining ore with an AVERAGE HEAD GRADE in the top decile (10%) or quartile (25%) of all producing mineral deposits, will likely have an AISC in the lowest decile or quartile of all producers. The average AISC, worldwide, for 2025 was $1,510 per ounce produced. Auryn’s grades totally blow away those of the El Penon whose AISC is about $450.

7 Likes

Well, well, well - that’s pretty clear …… at least to me.

Thanks BB!

And 58 years on that ONE vein?

Probably nothing.

2 Likes