Hey Jimmy! 5,000 coming! Those Tailings are looking $$$$

2 Likes

I had some Cerro Dorado shares that became Auryn after the reverse split. If you have some as well and need documentation regarding the reverse split, it is in the quarterly report disclosure dated June 30, 2018. you can find it here:

5 Likes

Brecciaboy,

What ratio are you expecting for the MDMN:AUMC share distribution?

200:1? 150:1?

BB. Where did I suggest that I know more? I was simply stating that trying to predict AUMC’s AISC by any comparison to El Penon was laughable. Why, because they are both in Chile and Luis thought the two deposits were similar? That’s fun to post about and draw your conclusions and post those conclusions over and over and over again to an audience who doesn’t know any better, but that doesn’t have anything to do with the comparable costs b/w the two projects. Its analagous to stating that AUMC should be valued based on industry averages or magically plopped onto the most hyperbolic stage on the Lassonde Curve without them having accomplished ANY of the steps that lead to those rewards. Its analagous to inferring that the past 20 years in this investment is relatable to the normal mining cylce or that AUMC managed to be the 1 in a 1000 miners reaching production. Maurizio could have made a decision to build a little plant a decade ago, JJ three decades ago. It’s been a static asset with the exception of the recent efforts to find one (of many veins). Why would there have been any dilution??? (following the first massive dilution). Spend a few million dollars based on a bet that historical results and chasing a vein will turn a profit. It just might! But AUMC will operate and be valued as the anomaly it is. A public co that should clearly be private. There are 100’s of family owned “Gold Rush esqe” projects that have been built on the same foundation. For holders of MDMN, where 90%+ of investors money is trapped, the hope needs to be that any value that is created and/or appreciation in the stock is sustainable, beyond a couple years, as there will not be an opportunity to sell. I think we all can agree that the POG won’t be an issue, as it makes its way to $10k.

It’s not a great sign that the one dissenting voice, which has been right a lot more than wrong, receives so much emotional backlash. I clearly disagree with the analysis but let it play out. This is exactly why I’m hoping to see some production where the “rubber meets the road” and all of these metrics (AISC, grades, production, profitability, valuation, dividends) come into the light of day.

If AUMC becomes the highest grade, lowest cost, dividend generating machine you will only hear congrats and praise from my end. I would only ask if/when some of these “optimistic” projections fall short, that there is productive debate vs another long phase of denial. Nobody (well almost nobody) believes that this crazy journey has been part of some grand plan nor anything but an investment of epic disaster BUT tomorrow is another day and even a broken clock is…..

J.P. Morgan projects gold averaging $5,400/oz by Q4 2027. By the end of 2026 there will be 1-2 Qtrly Reports showing financials. The thing that will light a fire on moving PPS up rapidly is Free Cash Flow (FCF). Having a high PPS will benefit all present shareholders when MDMN converted shares are distributed as AUMC shares. The distribution will likely take some more time to be acted on. A big if, when the distribution occurs, a PPS above $5 would certainly qualify putting AUMC on an upgrade path to a major exchange. At that time AUMC will be a trading stock and have news very worthy of promoting the path forward to mid-tier status and expansion. That is what my foresight is telling me management is moving towards. It has been signaled and is entirely possible. 2026 is a pivotal year for the success of AUMC.

EZ

8 Likes

Yes, I predict the “free cash flow” from the very high profit margin will pay the debts of this company expeditiously and cause a very precipitous re-rating. 2026 is our year. Govern yourself accordingly - why wait, feel free to buy/sell AUMC stock NOW as you wish (put your money where your mouth is).

![]()

5 Likes

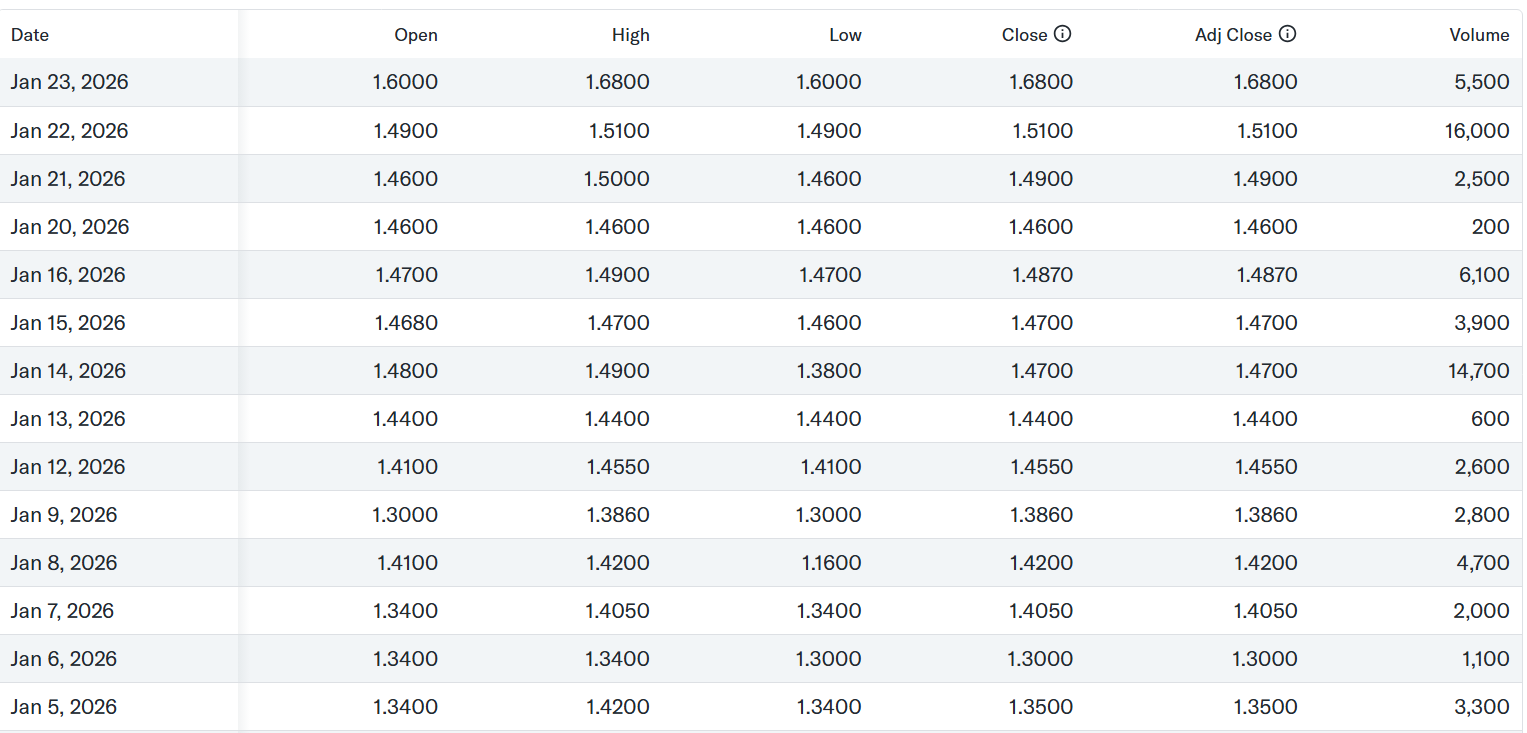

Hey! That’s what I’ve been saying for months. But nobody seems to follow through. How is anyone going to make any money when this sucker hits $5?? Anybody want to guess how many shares traded in all of 2025? And the total value?

The fortuna project is at 1,000 tons a month now but trying to get to 3,000 tons soon

The Caren project was at 1,000 tons a month then October 2025 asked for 1,950 tons a month now January 2026 trying for permit to 3,000 a month. On last update it seems to me on Caren might even go higher than 3,000 a month

my question on who knows about the flotation plant we constructed

How many tons a month can this plant handle? If it’s low can you expand on or have to rebuild a separate bigger plant

Also how much money would AURN be receiving at 6,000 tons a month? I know this would be at full production but it could be realistic very soon

2 Likes

Barring a crash in the price of gold, $5 a share is in the bag; sooner rather than later. At least $5 will look good on paper even if one can’t really trade volume at that price! (especially for the Medinah shareholders watching from the sidelines.)

6 Likes

Yeah, the froth flotation potential capacity is a question I’ve posed for quite awhile, to no avail. But, I’m about 100% confident MC would like to scale production as fast as possible, if for anything to get back ASAP that $10 Million he loaned to the company at ZERO interest (you can call him your Godfather if you wish). There’s also another loan of $4 Million to a third-party entity, all of which when considering the potential profit is relatively immaterial, as I will show immediately below.

At, 6,000 tons per month,15 gpt gold, 80% recovery, a gold price of 4,900.00 per ounce, and an AISC of 1,200.00 per ounce, the company would bring in $8,565,916.39 per month:

6,000 x 15/31.1 x .80 x (4,900.00 - 1,200.00) = $8,565,916.39

I’m not an expert in the mining industry, but that’s my computation - and it’s a nice sum for ONE month - and IF it materializes, it could pay off company debt in a jiffy, a good thing.

BTW, the 31.1 in the above equation is the number of grams in a troy ounce.

Many on this board believe those are conservative numbers, but the truth is they could end up being higher or lower - you can make a spreadsheet to play with it.

The other question we might have is What will happen with all this profit? Will MC opt to use some (or all) to expand? Will he use some (or all) for dividends? MC has stated he aspires to make AUMC a mid-tier mining company, so we probably should resign ourselves to the fact that some will be used to expand. But, companies with healthy share prices have better access to capital, right? Will some be used for dividends, which will attract interest/demand for the shares? Seems like it would be a great “business” decision. MC already got a loan once - which by definition means that he was able to convince the financier to loan the company (read they had the DATA to induce them, which at least one shareholder denies and thinks he knows more).

Whichever road MC chooses, I’ll be 100% in support - as it is only because of HIM that we even have a chance to recover and in fact make out well.

5 Likes

Yes, Les screwed all MDMN shareholders while other management were likely sleeping at the wheel. MDMN’s 2.8B outstanding shares had much to do with the NSS/market makers trying to take it down. I’m aware there are a few other factors involved, but the criminal activity against MDMN shareholders really beat us down. We were also lucky enough that wizard took the bull by the horns to gain some resolve for us.

![]()

![]() But that was THEN — this is NOW.

But that was THEN — this is NOW. ![]()

The good news is that the mountain still stands, and now all claims are consolidated under Auryn Mining. If not for one capable man with the means to pull us out of the quagmire, we would have faced inevitable doom. How long ago was that? Many current shareholders of AUMC bought in only after the resolve.

Now we see the results of MC’s actions. As of today & the likely projections, I’d say we are all much better off than it could have been. MC used his own personal millions (interest free) to get us here. A few of us wanted different paths than what MC ultimately chose. But MC had & still has the vantage point to have made those decisions, with opinions of credentialed mining experts who visited. Regardless of prior dilution some years ago, it’s still a new day in Medinahland/Auryn where most all of us will prosper … significantly. I’m good with that! ![]()

4 Likes

Baldy, there are 9 million shares of AUMC in the float. There is and has been minimal trading volume because the owners of those 9 million shares know the real value of their shares is substantially above the current price. If you are lucky, when the price hits $5, maybe some of those shares will become available, or not!

5 Likes

While its nice to reap the benefits of this ripping market in gold and, in particular silver, I much preferred the steady grind higher. Silver has become a meme and the new, hot, retail play. JPM’s shift from a long-term short to a massive long in silver has created a squeeze across the Euro banks. Its impossible to know how long that plays out but its going to end poorly. There will be a massive flush and volatility before gold and silver can begin their long grind higher again. Unfortunate.

This explosive move is undoubtedly creating bids in long lost assets. Some of which I forgot I even owned. Can AUMC reach higher and higher prices with its float? It doesn’t take much. AUMC traded a total of 700k shares in all of 2025! To your point, the trick is sustainability. If Maurizio is able to hit some of the numbers tossed around here (or even a fraction of) there will be sustainability. Back of the napkin, at today’s prices ($100M+) the market is discounting a company that is producting 7-10k ounces and clearing $3k an ounce in profit. If that number is exceeded there’s no reason why the share price can’t, sustainably, trade at this level or higher. At $5, AUMC would need to be closer to 20-25k ounces. The P/E metric (30x) has no applicability to a company at AUMC’s stage. None, and without a resource, any sort of multiple to cash flow will be highly discounted. If AUMC is going to be producing 20k ounces with a 100td plant the grades will need to be VERY high and capacity will need to be running at close to 100%.

Assuming, AUMC receives the permits and succesfully exits the commissioning phase I’m guestimating 3-5k ounces with an AISC of $2,000oz+. That’s what makes a market.

Despite the lack of volume, today, the share price will ultimately settle near true vaue and that price is all that really matters to holders of MDMN who will be forced to watch a lot of the action from the sidelines (until mid 2027?).

I’ve got my popcorn.

Hi Z. Yes, I’m aware of the float. Hard to sell, hard to buy. I guess my point is/was that there was a very, very long period where folks around here were calling for a $5-$50 price target when the stock was trading at well under a buck. Not a lot of people putting backing up their bullishness with actual $$. I can only assume, and appreciate, that most people are tapped out with their position in MDMN even though AUMC is cleary the pure play with any sort of liquidity.

I’ll throw something out that will not be well received but remember this post later in the year. It would NOT suprise me if AUMC ends up issuing shares if they are able to maintain prices anywhere near this level. This doesn’t have to be because they need money (or they might) but rather its a mechanism to bring liquidity into the stock and generate sponsorship across the different banks. Co’s do this all of the time, particularly when they are basically trading like a private co. Its a smart a smart move but only available when things are going well. The other source of liquidity is clearly the millions of shares issued to MDMN holders but that’s 18 months out. AUMC will want to get the trading volume way up before those shares become unrestricted.

First up; plant completion target is this coming Friday. Hard to imagine that will actually happen. If some real trading buy volume shows up this coming week; might be a good sign.

7 Likes

A couple of hours ago, Bank of America came out with guidance estimating that in a couple of months (“by spring”), aligning with when Auryn starts selling their “float concentrate”, the price of gold will be trading at $6,000 per ounce. Today (1/24/26), the POG is at about $5,000 per ounce. Assuming that Auryn’s froth flotation plant is all “dialed-in” to maximize recovery rates and hitting on all cylinders, what kind of profits and cash flow might Auryn be able to generate in Year 1 of operations?

In making an admittedly “back of the napkin” type of earnings/cash flow projection (written “in pencil” for now and subject to change when more accurate data is released), certain input variables need to be chosen. These include the price of gold, the AISC, the average head grade/mill grade, froth flotation recovery rates, recoverable ounces, daily and annual production rates, # of workdays per year, production rate ramp-up estimation, etc.

As far as the price of gold goes, I’ll calculate projections for both the current POG of $5,000 and for B of A’s projected $6,000 per ounce. I’ll set the projected AISC at $1,000 per ounce. The average “HEAD GRADE” I have set at 0.5 ounces per Tonne which equates to 15.5 gpt. I have the froth flotation recovery rate set at 80%. The number of “recoverable ounces” will be 0.8-times the number of “contained ounces”. The daily production rate will be set at the nominal throughput rate for the FF plant which is 100 Tonnes per day entering into the FF plant from the ball mill. I’m assuming that there will be about 330 working days per annum. I’m going to wait for guidance from management before estimating a production ramp up rate as a function of time. Management upwardly amended their order for the FF plant after placing the original order for a 100 TPD plant. We do not know if that materially changed the 100 TPD figure.

The annual production rate, going into the ball mill and then into the FF plant, would be about 33,000 Tonnes per annum (100TPD times 330 days). With an average head grade of 0.5 ounces per tonne, this means that the number of “contained ounces” of gold coming from the ball mill and into the FF plant will be 16,500 ounces per annum. With an 80% recovery rate, this means that 13,200 ounces of gold equivalent will be recovered/produced per year in “float concentrate” form.

Based on an AISC of $1,000 per ounce, and the POG set at $5,000 per ounce, the marginal profit would be $4,000 per recovered ounce. With the POG set at $6,000, the marginal profit would be $5,000 per ounce. If you multiply a marginal profit of $4,000 per ounce to the recoverable ounces figure of 13,200 ounces, you’d get an estimated annual pre-tax profit of $52.8 million or 75-cents per share based on 70 million shares outstanding.

This would represent a $66 million pre-tax profit figure in the case of the $6,000 per ounce POG scenario. This equates to about 94-cents per share in earnings per share (EPS). Based on the average “multiple” of EPS in the mining sector of 30.1, THEORETICALLY a miner making 75-cents per share would have an “appropriate share price” (ASP) of about $22.50. A miner earning 94-cents per share should THEORETICALLY trade at about $28.20. Note that this is not a prediction by any means. I’m just setting up the equation.

A question that might arise is whether or not a miner with only 7 million shares in its “float” of readily sellable shares should THEORETICALLY command a higher “multiple” of EPS than the average for the sector. I would suggest a resounding yes. A miniscule number of shares in the “float” might suggest that arriving at the “appropriate share price” might take less time and a lesser amount of buying. With only about 7 million shares in the “float” (before any allocation and distribution of Medinah’s “AUMC” shares), we are basically in uncharted waters from an historical point of view in this sector. I’ll review later how this enigma came about.

IS IT A GOOD THING OR A BAD THING TO HAVE A MINISCULE “FLOAT”?

The “float” represents the SUPPLY of readily sellable UNRESTRICTED shares that interacts with the DEMAND variable (buy orders) to determine the appropriate share price through the PRICE DISCOVERY process. With a miniscule “float”, less DEMAND (less buy orders) will be needed to attain the “appropriate share price”.

Auryn’s miniscule “float” is associated with management’s ownership of about 62% of Auryn’s shares but they are restricted, as RESTRICTED and/or CONTROL SECURITIES, from resale into the open market by RULE 144 of the securities laws. These shares are technically ISSUED AND OUTSTANDING, but are not part of the readily sellable “float”. They are not part of the SUPPLY variable. Smaller shareholders get the benefit of management’s financial incentives being co-aligned with theirs but they don’t need to worry about management dumping large amounts of shares on the open market.

Since RESTRICTED securities still earn CASH DIVIDENDS, smaller shareholders might anticipate management providing a certain percentage of SHAREHOLDER REWARDS via allocating the profits towards CASH DIVIDENDS. If “the market” were to misprice shares below the “appropriate share price” and if the company was able to grow the profits by ramping up production over time, then shareholders could simply take their cash dividends and buy inexpensive shares out of the open market and thereby over time, expose PROGRESSIVELY LARGER SHARE POSITIONS to PROGRESSIVELY LARGER CASH DIVIDENDS. This represents the essence of a “positive feedback loop”.

In a scenario like this the DEMAND for shares goes up and the desire to sell shares (the SUPPLY) goes down which drives the share price upwards to the “appropriate share price”. In essence, “The market” can be FORCED to “discover” the “appropriate share price”.

DISCUSSION

Note that this analysis is set up on an “If…then” basis. If the "input variables are “X,Y, and Z”…then the “appropriate share price” would be “Q”. Feel free to put in whatever input variables you feel appropriate. Some will end up being too high and some too low. I’ve always found it helpful to “run the numbers” as best you can. Seeing how the input variables inter-relate is helpful in learning the industry. For example, in this industry the incremental increases in the POG tend to drop straight to the bottom line.

The one item that is extremely important is “HEAD GRADE/MILL GRADE” coming out of the adit. This is because it is a key factor in BOTH the top line income line entry and the ALL IN SUSTAINING COST per ounce produced line item entry. The ALL IN SUSTAINING COSTS drop markedly with higher GRADES at the same time that the top line income figure goes up. This way the disparity between the two, “MARGINAL PROFIT PER OUNCE” increases a disproportionately.

Those “appropriate share prices” cited above sound way too high, don’t they? I agree, so, which “input variables” should we amend? At this point in time, I wouldn’t recommend amending any of them. Just write them down “in pencil” subject to change.

The point needs to be made that we are in somewhat “uncharted waters” here. I’ve never witnessed a junior explorer/developer making it all of the way into PRODUCTION with only 70 million shares issued and outstanding. I certainly have never seen a PRODUCER with a “float” of 7 million shares. Furthermore, I’ve never witnessed the CEO of a junior miner being willing to advance all of the cash needed to make it all of the way into production while charging zero interest. I don’t anticipate ever witnessing this again. The GRADES at level 3 of the DL2 Vein are pretty much off the chart. The Plenge Lab smelter test results of 128 gpt gold are way off the charts. I’ve never seen a junior miner rebuff an offer from Enami for 70 gpt gold net of Enami’s fees. I’ve never witnessed a junior miner timing its entry into PRODUCTION coincident with the prices of all 3 metals it will be selling trading at all-time highs. I’ve never witnessed a 7-year-long “campaign of deception” perpetrated against a corporation and its shareholders of the intensity we have been witnessing. It only makes sense to expect an “appropriate share price” that appears to be off the chart at first glance.

Any junior mineral explorer that successfully defied the distant odds and inordinately long timeframes for making it into production will anticipate a significant “MARKET RE-RATE” once production is confirmed by the investing public. All of these other enigmatic realities should only augment the anticipated “MARKET RE-RATE”.

8 Likes

Well I called 5.00 PT by end of April.

2 Likes

One of the many reasons the smart money believes silver hitting $100 a share is just the start of something much bigger is this:

Intel’s stock drop on January 23, 2026, was primarily driven by manufacturing and broader supply chain issues, a critical global silver shortage is a significant contributing factor to the industry-wide constraints mentioned by management.

The current silver supply crisis and its impact on Intel can be broken down into three key areas:

1. Direct Impact of the Silver Shortage

-

Essential Component: Silver is crucial for high-end AI chips and data centers due to its superior electrical and thermal conductivity.

-

Supply Crunch: In early 2026, silver inventories at major exchanges (LBMA and COMEX) fell to record lows, with lease rates spiking to 8%, indicating industrial users are desperate for physical bars.

-

China’s Export Curbs: On January 1, 2026, China reclassified silver as a “Strategic Material” and restricted exports to prioritize its own domestic semiconductor and solar industries, further tightening the global supply available to companies like Intel.

4 Likes

100%

And another contributing factor (in my opinion) is JPMorgan now having to COVER their shorts, which is an offshoot of your “Supply Crunch” above. There are conflicting versions as to just HOW much they have to cover, but I like what this guy has to say:

As for the permits Maurizio knows 110% that Auryn will be receiving them from SERNAGEOMIN. They have a very good relationship with them. The only reason he didn’t put in the update is because he wants to make its official in a PR. This will start an ascending short term SP to 5.00. After that watch out!

3 Likes