Why would AURYN issue shares for various option agreements? Isn’t equity percentage interest quite different from dilutable shares? MDMN (and shareholders) should be quite happy with the 15% equity interest presently held in AURYN with the eventual exercise of the terms of the option agreements or a TO. With any new early production agreements I would think hard cash would result. These agreements would likely be totally separate depending on the make-up of the ownership, and in addition to the existing option agreement contracts for 100% claim ownership. I would expect AURYN to be the main beneficiary early on, especially on their newly acquired properties, of any early exploitation. Phase 2 drilling on the Merlin-Fortuna is scheduled to begin this quarter according to the timeline in AURYN’s project stack. Will there also be some early production (bulk sampling) pursued? AURYN states one of it’s goals is to prioritize the best exploitation targets. Despite this goal, AURYN is a private Company and reserves the right to disseminate information to the public at its own discretion. If the veins are on MDMN property there may be some benefit to MDMN shareholders much earlier than on the Fortuna, even though the Fortuna appears more favorable for early production. Unfortunately for Cerro shareholders, the early production equation does not work out until there is a resolution to the Quijano’s ownership problem. Not resolving the Quijano ownership interests is prolonging the PPS distress in both stocks. AURYN will work around this roadblock if it is not resolved up until the July 31, 2017 termination date, or just exercise an early option and TO for the 15% if there is no other resolution possible.

@mdmnholder or @cornhuskergold – give me a wag for the production cost per tonne given what you see so far.

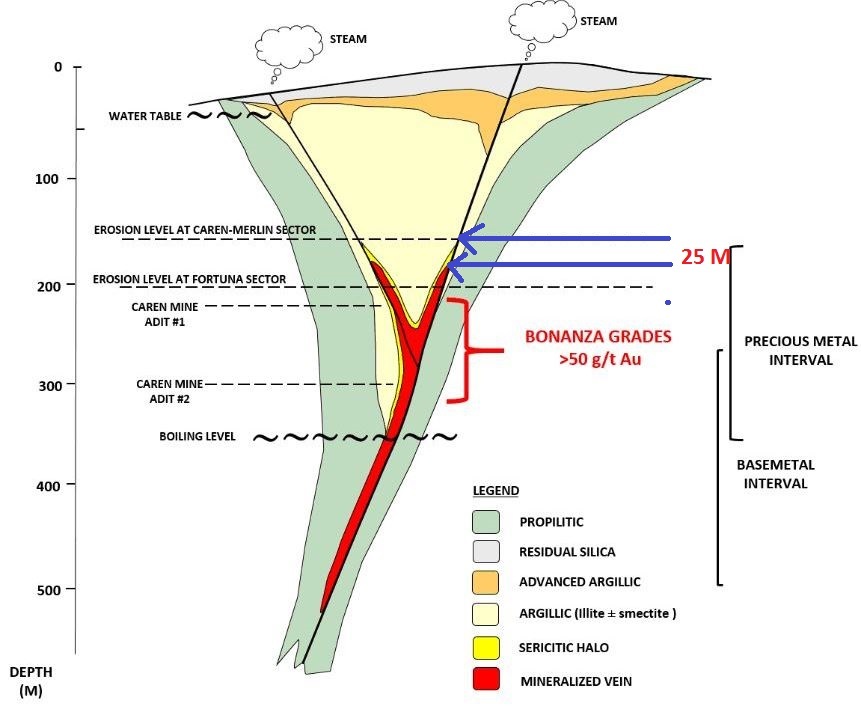

The high grade veins appear very shallow. Note per Auryn the deepest Cerro ever went was 100 meters and they mined on 3 levels above that.

“The Fortuna de Lampa mine was developed on a system of relatively narrow, high grade gold-bearing quartz veins hosted in granodiorite. The veins trend approximately north-south and dip moderately to the east. The system can be traced over a length of approximately 800 meters and there is evidence of an associated breccia to the south. There are about 1,100 meters of underground workings that have been developed on four levels concentrate on the main Fortuna vein and reaching a depth of 100 meters. Records for small scale production in the 1940´s and 1950´s gave an average grade of 59 g/t gold and 104.1 g/t silver.” Fortuna de Lampa Mine - Agreement Signed with S.C.M. Cerro Dorado Chile - AURYN Mining Chile

On the other hand: you can see from the Auryn diagram that the “erosion level” is about 40m to 50m lower at Fortuna than it is at Merlin1, meaning approx. 50m more overburden. Their diagram matches pretty closely the spacing on the north side of the mountain. Adit #2 looks to be a little more than 100m below the plateau top on the north side. Adit #1, maybe 70m. The grades change in between there somewhere. And this matches up with Auryn’s diagram and the “erosion level” differences

There are so many unknowns … I also agree with the idea that there will be a series of approaches. They are not going to just treat 2 g/t to 7 g/t rock as “overburden” and throw it over the cliff. Do they process that now and that is the first production? Or do they pile it up and process it several years from now when they could do that locally? Do they go after the highest grade stuff first via the north side of the mountain or do they really construct a 100m deep pit? All unknowns.

You have to consider that anything that takes time to construct, say 12 months, starts to take it out of the timeframe of the Option. So only what they can do in the next 17 months matters to the pre-Option period (and any other TO / reverse merger options etc. just make it more complicated)

I will say that I know of a fairly shallow open pit about to be constructed in Canada that claims $600 / oz production cost. Deeper more complicated mines are finally getting under $1000 for all-in costs. I think the safest approach is to use a range - calculate with $600 and then with $850 and that will give you bookends, IMO.

Is over burden removal cost still in a very low per ton range? http://costs.infomine.com/costdatacenter/miningcostmodel.aspx

What is the normal comparison of open pit to underground costs. Some geologist types here may have models that would help. https://www.coursehero.com/file/p1a122i/23-Underground-vs-Open-Pit-Compare-total-mining-cost-per-ton-of-ore-for-each/

What is the g/t for the open pit you reference in Canada?

I misremembered. It is $730 AISC.

It’s a decent sized open pit, not particularly shallow.

About 0.80 gpt.

But they can run 29,000 tpd. Pretty decent production.

not a particularly great model for the ADL

SHAREHOLDER UPDATE January 27, 2016

Dear Medinah Minerals, Inc. Shareholders:

We are pleased to publish the attached News Item Update on bonanza gold grades in Caren mine, have returned over 100 g/t Au at Fortuna – Merlin system in the Altos de Lipangue project, Chile.“ prepared and released by AURYN Mining Chile SpA. on January 27, 2016.

Vittal Karra

Chairman and President

Medinah Minerals Inc.,

Lets hope it hits the news wires before the markets open. If they even bother.

Looking closer at the diagram provided by Auryn; it depicts the gold vein as being 25 meters below the surface of the Plateau and at surface at the Fortuna.

WAG is around $1,000/tonne which seems inline with other underground mines, regardless the grades will make it economic. I don’t have much experience with underground gold mines, but things to consider right off is rock stability. You have to bolt the ceilings and shotcrete, run air lines, build safety/escape rooms. I am also not sure how they mine, do they blast and haul rocks with scoops or do they blast and/or rip the face with a continuos miner. Then you need a conveyor belt system to run the rock to the portal.

The vein(s) may not be continuous and may have a dip causing adjustments. And then Chile has had some seismic activity and that is always good for a couple days of shut down while the mine is inspected for safety.

50 gr. per tonne is a lot of gold.

The stock should go at least at 3 cents only with this news.

Why is not working?

The news hasn’t even been out for 24 hours, plus I’m not sure it’s on the news wires yet is it? So no one knows about it except us.

As has been discussed previously, the stock is currently dependent on technical vs. fundamental developments.

That and who, what, when, where, and how much are still unclear.

Yes. A clear delineation of who owns how much of what is also paramount. We can assume that our insiders have secured themselves a lucrative exit (fiduciary responsibility is a four letter word in Medinahland) on any of the private/side deals. Now we need to learn what the peons (common shareholders) are getting served . Thankfully, in both MDMN and CDCH both insiders and peons are in the same boat. However, I’m hoping that insiders didn’t receive larger concessions in the private deals in exchange for less on the ADL. This has been a pattern in the past that we can all hope has been broken.

Given the importance of the CDCH /Fortuna claims , and Juan’s 50% ownership of same, hopefully there was also some progress on this matter at the recent meetings to report on soon.