According to my charts gold has finally (this morning) broken out of a 11 day downward channel. Most of us have gold & silver stocks that have reached rock bottom support levels. Let’s hope now we’ll start to see them start to head up again.

I know life can be busy for most of us, but I thought I’d mention that Karora has a webinar starting in just a few minutes. If you are interested and have time here is the link:

The webinar was skillfully presented and mostly covered the company’s slide presentation dated from March 1 of this year on the company’s website (see link at end of post).

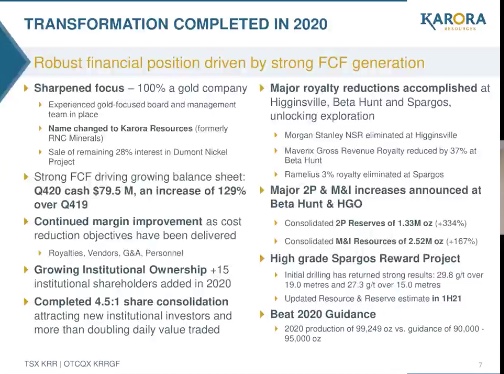

The webinar began with a slide looking back to accomplishments completed in 2020.

A couple of points that were made during the presentation that shareholders who don’t follow this one closely might not realize is that each quarter since mid 2019 KRR has shown a decrease in the cost of producing an oz of AU. 3rd qtr 2020 came in at $1,044/oz and Q4 2020 will be released in the next few weeks. Cost per oz is still a little high but continuing to decrease with increasing organic growth of assets. I did not realize the severity of impact on labor due to covid19 restrictions. I suppose many mining companies experienced the same type of labor shortages due to covid restrictions. At one point, the company had a 90% reduction of it’s labor force, but still managed to meet it’s production goals each quarter, and for the year. To fly in labor, contractors were restricted by a two-week quarantine, would work a two-week shift, and then have another two-week quarantine upon returning home! Covid19 constraints were not very conducive to expanding operations. Many of the labor force just chose to remain home rather than experience a dual quarantine period. Covid19 restrictions are anticipated to be eased during the upcoming year.

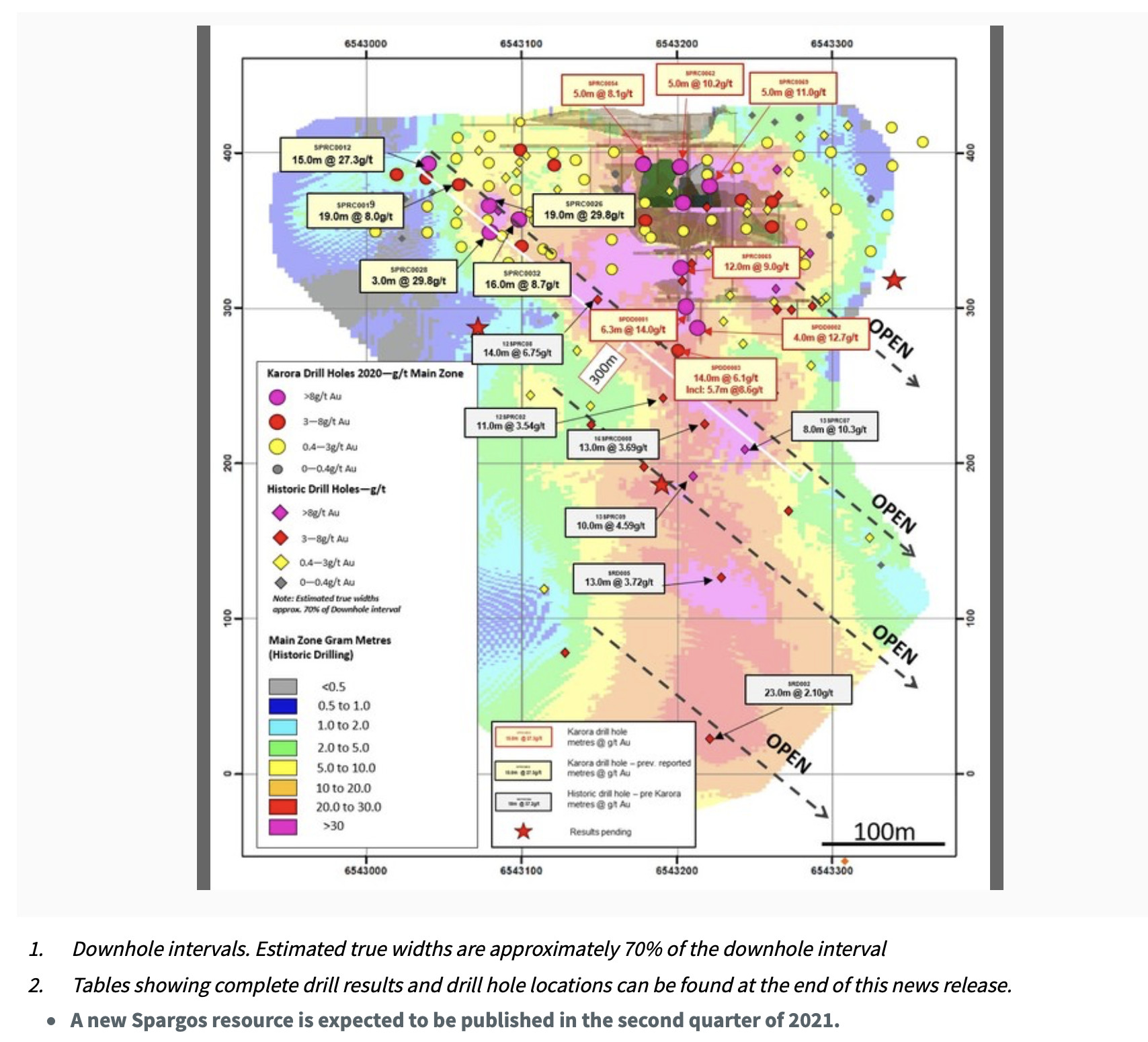

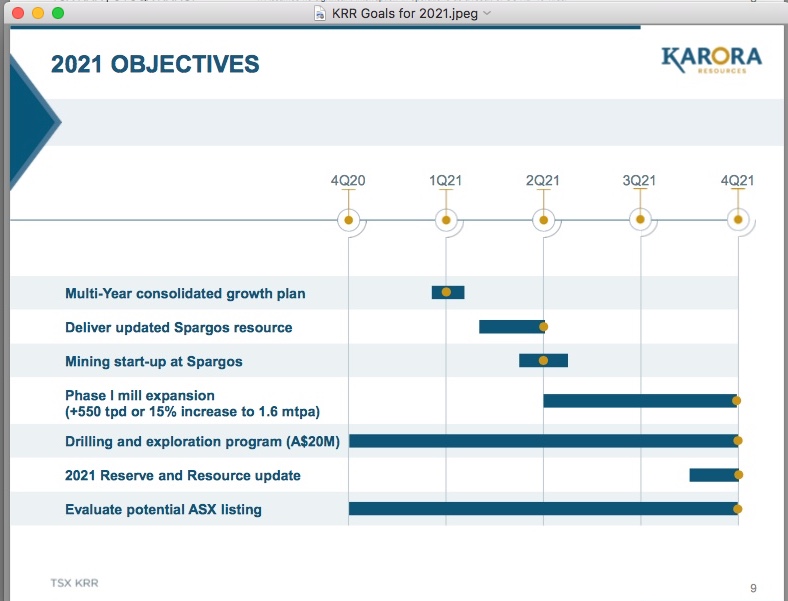

I consider this a growth oriented company worthy of long term investment. Paul Huet, the CEO, is relocating to Australia with family and flying out March 23. Annual production is expected to grow to 200-250Koz and the company will be pursuing an ASX listing. The Higginsville mill will be upgraded to handle an additional 550 tons per day. The High grade Spargos Reward Project has returned new high grade gold intercepts along 400 meters of strike length all within 100 meters of surface. This will be easily open-pittable with an updated resource expected by summer. 2021 has a $20M budget for the exploration and drilling program split between resource development and exploration in several key areas.

There was much more presented in this webinar, but for brevity I’ll stop here and encourage anyone interested to review the corporate presentation in the link below.

Future webinars to update shareholders will be announced, and this one was recorded and should be available sometime online. Overall the presentation assured me with great confidence that this company will continue to grow and add shareholder value over many years to come. Karora has the assets, location and team to move this forward.

ARTEMIS RESOURCES has drilled some significant assays -

Carlow Castle -

44m @ 2.00g/t Au, 0.71% Cu, 0.15% Co from 132m in ARC253

11m @ 4.24g/t Au, 1.58% Cu from 71m in ARC233

4m @ 11.1g/t Au, 2.0% Cu, 0.18% Co from 639m

53m @ 2.98g/t Au, 0.85% Cu, 0.25% Co from 120m in 20CCAD004

75m @ 1.15g/t Au, 0.36% Cu, 0.05% Co from 56m in 20CCAD002

Also - The Company has identified 7 initial targets/prospects for deep drill testing at Paterson Central, with 5 of them surrounding the Havieron gold-copper deposit to the north, east and south.

It may be a good time to get in, since as like a lot of PM stocks, the price has come down. Right now $0.064 , 52-week high $0.1271

**Silver Elephant’s Sunawayo Drills 3 Meters of 421g/t Silver, Multiple Intercepts over 100g/t AgEq 421g/t Silver,

Vancouver, British Columbia, March 18, 2021 – Silver Elephant Mining Corp. (“Silver Elephant” or “the Company”) (TSX:ELEF, OTCQX:SILEF, Frankfurt:1P2N) announces the highest silver and zinc grade intercepts to date from its 2,300 meter Sunawayo maiden drill program.

SWD010 intercepted 3 meters of mineralization grading 421 g/t silver, 0.92% lead, and 0.90% zinc (469 g/t AgEq) within 10 meters grading 144 g/t silver, 0.43% lead, and 0.97% zinc (183 g/t AgEq). SWD009 intercepted 2 meters of mineralization grading 50 g/t silver, 0.40% lead, and 7.67% zinc (290 g/t AgEq).

So far, 100% of drill holes at Sunawayo have encountered silver and lead-zinc mineralization. Significant drill results from all 10 of them. See their website for individual drill results.

I began a starter position in this one last summer, along with a few other prospective miners located in Nevada. It then qualified to move up from the pinks to the OTCQB last August. Blackrock Gold (BRC.V, BKRRF) Closed a C$10.35 Million Bought Deal Public Offering on Feb 19, 2021.

A few days ago a trading halt and name change was announced:

Vancouver, British Columbia–(Newsfile Corp. - March 15, 2021) - Blackrock Gold Corp. (TSXV: BRC) (the " Company ") is pleased to announce that effective Wednesday, March 17th, 2021 the Company will change its name to Blackrock Silver Corp., to better reflect the silver dominant nature of our flagship Tonopah West silver-gold project located in the Walker Lane trend of the “Silver State” of Nevada.

The trading symbol did not change with the name change. Yesterday, along with many other miners, the company had a very good day. I had thought the large gain was because of the name change, but may have “coincidentally” actually been front running this announcement:

BLACKROCK DRILLS 1,003 G/T SILVER EQUIVALENT OVER 3.1M IN NEW VEIN DISCOVERED DURING STEP-OUT DRILLING AT TONOPAH WEST

FOR IMMEDIATE RELEASE TSX-V Symbol: BRC

March 18, 2021, ‑ Vancouver, British Columbia. Blackrock Silver Corp. (the “Company”) is pleased to announce the first high-grade gold and silver drill intercepts from its 2021 program on its 100% controlled Tonopah West project located in the Walker Lane trend within the “Silver State” of Nevada.

HIGHLIGHTS:

TW21-057, -058 and -062 have intersected a new vein immediately south of the known vein swarm at our DPB target with TW21-062 intersecting 3.1 metres grading 6.15 grams per tonne (g/t) gold (Au) and 388 g/t silver (Ag) or 1,003 g/t silver equivalent (AgEq) (Ag:Au 100:1). A minimum strike length of 425 metres has now been established;

Drilling to the west of the main Victor vein has intersected significant alteration with 23 metres and 12.2 metres of veins and silicified breccia cut in TW21-033C and TW21-092C respectively on the footwall (west side) of the Pittsburgh-Monarch fault with assays pending;

A total of 13,000 metres of drilling has been completed since January 4, 2021, and a total of 41,300 metres of drilling has been completed since June 17, 2020; and

Three core drills and one RC drill are active on the project with two core drills infilling on the DPB target, where a maiden resource estimate is to be delivered by year end, one core drill exploring along the Victor vein system, and the RC drill continuing the step-out program.

(BLACKROCK DRILLS 1,003 G/T SILVER EQUIVALENT OVER 3.1M IN NEW VEIN DISCOVERED AT TONOPAH WEST)

Karora Announces 2020 Results Including Record Annual Net Earnings of $88 Million, 2020 AISC Cost Guidance Beat, Along With Record Low 4Q20 AISC of US$912 per ounce…gotta love that they beat their goals. Paul keeps delivering. One day the market will reward them.

Karora Announces 2020 Results Including Record Annual Net Earnings Of $88 Million, 2020 AISC Cost Guidance Beat, Along With Record Low 4Q20 AISC Of US$912 Per Ounce

Karora will host a call/webcast on March 19, 2021 at 10:00 a.m. (Eastern Time) to discuss the 2020 results. North American callers please dial: 1-888-231-8191, international callers please dial: (+1) 647-427-7450. For the webcast of this event click [here] (replay access information below).

TORONTO, March 19, 2021 /CNW/ - Karora Resources Inc. (TSX: KRR) (“Karora” or the “Corporation”) is pleased to announce its financial results and review of activities for the years ended December 31, 2020 and 2019. All amounts are expressed in Canadian dollars, unless otherwise noted. For additional information please refer to Karora’s Management’s Discussion & Analysis (“MD&A”) and audited consolidated financial statements for the years ended December 31, 2020 and 2019.

Highlights

Gold Production Exceeded Guidance: Consolidated gold production of 99,249 ounces for 2020 from the Beta Hunt and Higginsville mines in Western Australia, exceeded the top end of the 2020 production guidance of 90,000 to 95,000 ounces. Gold sales for 2020 totaled 98,656 ounces. For the fourth quarter of 2020, production was 25,637 ounces, the strongest quarter of production in 2020.

Ongoing Cost Reductions: Consolidated all-in-sustaining-cost (" AISC ")1 was US$912 per ounce for the fourth quarter of 2020, an improvement of 13% over the third quarter of 2020 and a record low since acquisition of the Higginsville mill in 2019. Consolidated AISC for 2020 was US$1,026 per ounce, which beat 2020 guidance of US$1,050 to US$1,200 per ounce, and was 11% lower than 2019.

2021 Production and Cost Guidance: Consolidated production and cost guidance for Karora’s Australian operations (Beta Hunt and HGO) of 105,000 to 115,000 ounces of gold at an average AISC1 of US$985 to US$1,085 per ounce. Consolidated HGO, Beta Hunt and Spargos drilling and exploration expenditures for the full year 2021 are targeted to be approximately A$20 million.

Record Earnings: Net earnings of $42.9 million for the fourth quarter of 2020 and $88.1 million for the full year 2020. Net earnings were $0.30 per share and $0.63 per share, for the fourth quarter and 2020, respectively. Net earnings for full year 2020 was positively impacted by an after-tax impairment reversal of property, plant and equipment of $25.3 million.

Record Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (“EBITDA”)1: Adjusted EBITDA was $33.9 million for the fourth quarter and $89.8 million for the full year ($0.23 per share and $0.64 per share, respectively).

Strengthened Cash Position and Balance Sheet: Karora ended 2020 with a strong cash position of $79.7 million, net of $4.0 million in debt repayments and $8.9 million paid into legacy gold price hedges in the first half of 2020. Working capital was $56.8 million as of December 31, 2020, an improvement of $30.3 million compared to December 31, 2019.

Consolidated Gold Mineral Reserve and Gold Mineral Resource: On December 16, 2020, Karora announced a 334% increase in consolidated gold Proven and Probable (“2P”) Mineral Reserves to 1.33 million ounces (23,531 kt @ 1.8 g/t) and a 167% increase in consolidated Measured and Indicated (“M&I”) gold Mineral Resources to 2.52 million ounces (41,994 kt @ 1.9 g/t) for its Beta Hunt and Higginsville operations in Western Australia.

Significant Royalty Reductions Leading to Increased Production Potential and Lower Costs: During 2020, Karora successfully negotiated the reduction or elimination of a number of royalties on its Western Australian properties including the Morgan Stanley NSR at Higginsville, Maverix royalty at Beta Hunt and Ramelius royalty at Spargos Reward.

Spargos Reward Acquisition: On August 7, 2020, Karora completed the acquisition of the Spargos Reward Gold Project. Spargos is a high-grade open pit gold project in Western Australia that is expected to begin generating positive cash flow for Karora in the second half of 2021. An updated resource estimate is planned for release in the second quarter of 2021.

Divestiture of Remaining Interest in Dumont Nickel Project While Retaining Exposure to Eventual Project Sale: During 2020, Karora sold its remaining 28% interest in Dumont to sharpen the corporate focus on gold and materially reduce corporate overhead associated with carrying the project. Karora immediately received $10.7 million in cash and maintains upside to receive up to an additional US$30 million upon a future sale or monetization of the asset by its owner.

Share Consolidation: Effective July 31, 2020, Karora completed a consolidation of its outstanding common shares on the basis of one (1) post-consolidation common share for every four and a half (4.5) pre-consolidation common shares. Since consolidation, the average daily traded dollar value of Karora’s shares has more than doubled to $4.6 million per day from $2.2 million per day previously.

Paul Andre Huet, Chairman & CEO, commented: "Karora delivered an exceptionally strong financial and operating performance in 2020 with net earnings of $88.1 million and consolidated AISC1 of US$1,026 per ounce sold. The fourth quarter was also exceptional with net earnings of $42.9 million and consolidated AISC1 of US$912 per ounce sold, an improvement of US$132 per ounce over the prior quarter and a record since the acquisition of the Higginsville mill in mid-2019. Since the acquisition, we have demonstrated a strong commitment to achieving cost reduction targets and have now delivered six consecutive quarters of AISC cost reductions, including by beating our target of achieving AISC US$1,000 per ounce by the end of 2020.

On a side note, Paul is hauling his large family(6-7 kids I believe) from Canada to Australia which will include a 2 week quarantine period. You don’t do this for no reason, I’m expecting some interesting developments going forward

Hmm, it seems Jaguar Mining is right about the price you picked it up at last August. Just curious, so did you sell it when it hit $9.20 USD ($11.30 CAD) just a month ago, or did you hold on for a long term hold and better tax rate on gains? I’ve recently exited a few non-core positions and picked up a starter position in Jaguar near last Friday’s lows. Before it jointed the OTCQX March 1, it cost me $50 a trade on Fidelity. Fidelity discourages trading pink sheet foreign equities, which I learned the hard way over the years. Jaguar currently has a P/E of 8.6, had good 4thQtr and full 2020 results and appears undervalued to me. It may still go lower, but may also be worth accumulating on dips. Looks to be at a good spot to pick up a few more shares and keep an eye on.

Metalla Royalty Acquiring Royalty on OZ Minerals’ Centrogold Project for Up To US$18 Million

Metalla Royalty Acquiring Royalty on OZ Minerals’ Centrogold Project for Up To US$18 Million

BY MT Newswires

— 7:52 AM ET 03/16/2021

07:52 AM EDT, 03/16/2021 (MT Newswires) – Metalla Royalty & Streaming Ltd. ( MTA) said Tuesday that it agreed to acquire an existing net smelter royalty on OZ Minerals’ CentroGold project from Jaguar Mining Inc. ( JAGGF) for up to US$18 million.

Consideration comprises an upfront payment of US$7 million on closing, which is expected in the first quarter, and up to US$11 million in contingent payments.

The NSR starts at 1% on the first 500,000 ounces of gold production before increasing to 2% on the next 1 million ounces of gold production. The NSR reverts to 1% on gold production thereafter.

There are so many companies out there doing well, even with pull backs. While Karora and NOVO are core favorites garnering the lion’s share of attention on the thread, a portfolio has many stocks to continuously add value. I’m sure posters here have other interesting picks that could be shared on the thread … just sayin’

Maybe Mike will remember this one from his trip to Morocco a few years ago.

I only have a small position here, having sold off most of it quite some time ago. Time to keep an eye on it as silver is in the spotlight?

Aya Gold & Silver Increases Measured and Indicated Mineral Resources by 340% at Zgounder

Montreal, Quebec, March 16, 2021 - Aya Gold & Silver Inc. (TSX: AYA) (“Aya” or the “Corporation”) is pleased to announce an updated Mineral Resource Estimate for its Zgounder Silver Mine in the Kingdom of Morocco.

Resources - Overview as of March 1, 2021 (Drilling till end of 2020)

· Measured and Indicated (“M&I”) Mineral Resources increased to 44.4 million ounces of Silver (“Ag”), a 340% increase compared to February 2018

· Measured Mineral Resources increased from 2.6 to 34.9 million ounces Ag, a 1,242% increase compared to February 2018

· The deposit remains open along strike and at depth

· Resource model will be further updated at year-end with subsequent drilling data

This is one of my favorite long-term speculative plays. I first posted last November about it (see post 1831 ?) hoping it would garner some attention on this thread. It is next to Summa’s high grade silver projects, also in the Tonapah District of Nevada (https://summasilver.com). I have starter positions in both companies. It is very early in development and drilling, but appears it will progress rapidly. I expect both will likely prove to be spectacular from early results just starting to come in. Another write-up on Blackrock Mining that expresses why I think it will be one of the better speculative plays available under $1:

A couple of weeks ago I opened a small position in Surge Copper. OTC symbol is grjvf

News Release

Surge Copper Significantly Expands West Seel with Step Out Hole Intersecting 585 Metres Grading 0.57% Copper EquivalentIncluding 164 Metres Grading 0.68% Copper Equivalent

March 24, 2021, Vancouver, British Columbia – Surge Copper Corp. (TSXV: SURG) (“Surge” or the “Company”) is pleased to announce assay results for multiple resource definition and exploration holes from the Company’s 100% owned Ootsa Property in British Columbia.

Highlights

Hole S21-228 intersected 585 metres grading 0.57% copper equivalent1 with the zone remaining open at depth

Hole S21-228 includes multiple higher-grade zones such as 0.99% copper equivalent over 16 metres and 0.76% copper equivalent over 44 metres

Hole S21-228 opens up significant expansion potential to the southeast with a 585 meter vertical zone of continuous mineralization, containing above deposit-average grades

Hole S21-228 ended in strong mineralization, leaving the deposit fully open at depth and to the southeast

On the weekly dollar chart covering the last 2 years it’s appears that the $ is overbought. If this turns out to be true I think we can finally look forward to rising gold prices in the weeks ahead… We’ll see said the blind. man. It turns out that several analysts disagree with me. They’re pro’s and I’m an amateur so they’re probably right.

******P.S. The POG is indeed headed for the lows of March 8th as the dollar continues to rise P.S.S. The POG is now where it was a year ago. When gold broke thru resistance on April 12 who would have thought we’d be here a year later. Silver is up 61% from a year ago

Silver is up 61% from a year ago

Silver is up 61% from a year ago